Introduction

Coach Incorporation, a fashion company that is based in New York, deals in high-end apparel and luxury products. It has 723 stores across the globe. For over a decade, Coach Incorporation asserted and expanded its position as a major global player in the upscale fashion market in fulfillment of its mission. Its brands encompass the main fashion areas like classical clothing, leisure and evening wear, sportswear and other complementary accessories. Coach Incorporation enhanced its collections through the licensed distribution of products such as footwear, watches, eyewear, cosmetics, and fragrances. The main competitors are Dooney & Bourke, Kate Spade LLC, and Michael Kors. The company successfully used flexible sourcing, retail distribution, and product-focused differentiation to survive the impact of these competitors. As a result, the annual sales increased by 20% from the year 2000 to the year 2011, that is, growth in annual sales from $555 million to $4.2 billion.

Coach utilized retail distribution in the recent past to further expand its presence in markets like Japan, China, and Europe. It applied a product differentiation strategy to expand and position itself as a fashion house. Coach’s scope of operations was characterized by retailing different fashion apparel to target men, women, and children market segments. For instance, Coach created renowned brands for a number of commodities like female handbags and cosmetics. Coach applied a series of grand strategies such as concentration, market development, product development, vertical integration, market penetration, and retail distribution strategies to expose its numerous products across the globe as the most competitive brand. For instance, Coach managed to expand its markets outside North America besides launching a series of new products such as sunglasses and fragrances.

Analysis of Coach Incorporation Strategic Capabilities

Coach Incorporation has a number of resources that have contributed to its success in the global market over the years. In order to ensure business sustainability, Coach has concentrated the focused strategy through clear definition and targeting of a specific market segment. Besides, Coach offers the most competitive prices for its quality products. Coach’s product differentiation through innovation and product reliability has been successful in ensuring that its brands remain unique and visible in the market. The strategies are achieved through provision of high-quality and stylistic designer products, effective supply chain network, middle-income customer segment, and attractive display in the stores. Coach premises are furnished in luxurious manner that attracts potential consumers from all categories in the market. Its value chain commences with the development of products through own factories, autonomous producers, and acquisition of licensed accessories from partners. Despite the success of these strategies, Coach is threatened by its competitors with more or less similar approach in doing business within the fashion industry. For instance, Dooney & Bourke, Kate Spade LLC, and Michael Kors threaten to reverse the gains that Coach has made in the fashion industry.

Strategic issue

As a prerequisite for sustainable organization performance, the strategic issues that Coach is currently facing pivot around the most appropriate market that the company should focus on or neglect in order to survive competition. Under this strategic issue, Coach currently faces the dilemmas of critical focus on the most reachable fashion market, potentials and threats of entering the stratified European market, potential of regrinding its current luxury brands, and the best strategies of increasing ambience without appearing as a copy cat of the main competitors. Therefore, what are the best strategies that Coach should focus on to survive competition in the dynamic fashion industry? In order to respond to this question, the following sub questions will be answered.

- Should Coach rebrand or introduce more brands to its current product line?

- What strategy will be necessary to properly differentiate the Coach’s brand?

External Environment Analysis

Industry competitiveness analysis using Porter’s 5 forces model

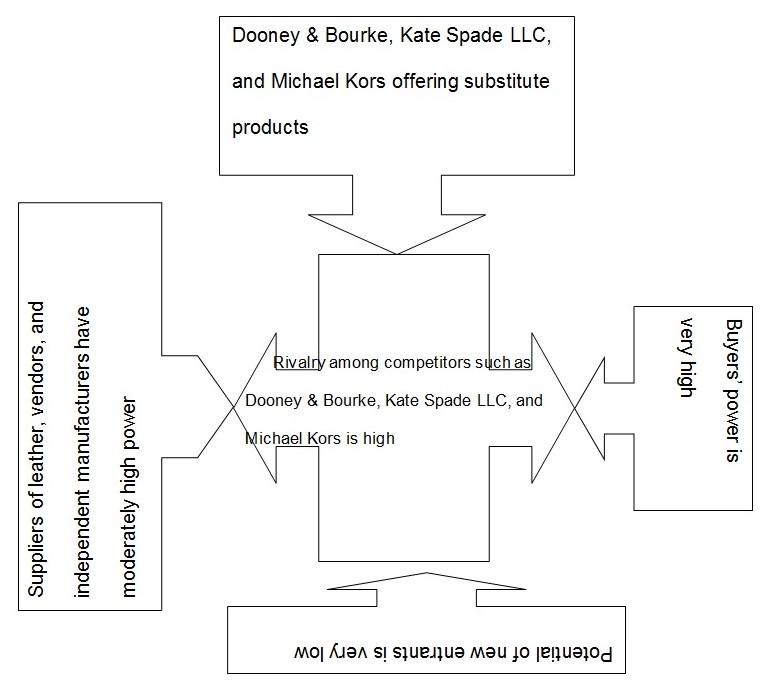

Porter’s five forces analysis is necessary for Coach Incorporation as it assists in comprehension of the market strengths and weaknesses. Although the Coach Incorporation has been a household name in the general fashion industry, the store has an expanded business portfolio which other fashion accessories. The expanded portfolio provides the Coach Incorporation with a competitive advantage in the sense that it can still maintain profitable performance even in instances where the retail fashion business experiences poor performance. Through diversification and portfolio balance, the Coach Incorporation is in a position to survive turbulence in the harsh economic environment characterised by stiff competition and sensitivity to market dynamics.

Threat of entry

It is very difficult for a new entrant in the fashion industry to successfully create a strong brand that can challenge dominance of Coach and Louis Vuitton among others. It would require massive capital for an aspiring investor to out perform their business prowess. Therefore, a new entrant may face difficulty in increasing brand visibility and cutting a piece of the market share. Since the fashion industry is characterised by the ability to produce high quality brands, a new entrant will have to build a following from scratch. This requires a lot of resources.

Threat of substitutes

In the premium bags segment within the fashion industry, threat of possible substitutes is very strong since most of the luxury bags are customised, thus, rarely have substitutes. Dooney & Bourke, Kate Spade LLC, and Michael Kors have the ability to offer an alternative perfect substitute to customers who may be unsatisfied with fashion products offered at the Coach Incorporation. Unsatisfied customers, therefore have other alternatives from where they can get fashion apparel. However, imitations may threaten the market a new or current players. When the counterfeits flood the market, the revenues of genuine companies will decline. In order to remain relevant, the Coach Incorporation has established a unique market for its customer through tailored optometry fashion products that are customized.

Suppliers’ bargaining power

In the fashion industry, the influence of the suppliers is highest when large volumes of apparel are purchased by a fashion store. When the influence is high, profitability of fashion stores is low. Since suppliers within the fashion industry operates and local and international levels, their influence differs. For instance, China, India, and Italy suppliers the largest volume of leather that Coach uses to make premium bags. Gucci, Coach, and other industry players have more than 100 suppliers. The partnerships between independent manufacturers and vendors reduce the power of the suppliers in this industry. Coach Incorporation has endeavoured to use its deep reservoirs as a strategy for balancing the supply forces in the fragile fashion market of the US and across the globe.

Buyers’ bargaining power

There is strong power in the fragmented retail segments which are indirect and direct to customers. Despite the fact that these fashion stores have very strong brand names, the buyers in this sector have the power to influence the prices for the premium bags and other apparels. The power of the buyers is high since this industry is characterised by high competition. Therefore, each store considers the perception of their customers before setting prices in order to survive competition. Fortunately, Coach has been consistent in maintaining their prices at half of the average prices of other brands.

Rivalry

There are several fashion brands operating in the same industry with virtually all of them dealing with a variety of fashion products and services. Players in the industry must be careful to survive any aggressive move by a competitor through creating a flexible brand name and constant product diversification. For instance, Dooney & Bourke provides the biggest competition to Coach Incorporation due to its biggest market share and expanded network standing at 30%. With many customers looking for good value for their money, quality in service delivery has remained the main basis upon which customers are making their final decision to purchase fashion products in the volatile fashion industry of the US. All the players in the industry are putting measures in place to ensure they attract more customers and therefore expand their market share through creation of a smooth supply chain, diversification, and brand positioning. Therefore, the size, in terms of space occupied by business premises, defines the temperature of the competition. In line with this, the Coach Incorporation’s New York branch is the biggest and busiest fashion store.

Key Success Factors Within the External Environment

Strong brand

Coach Incorporation has established a brand image that enables it to attract customers with less effort as opposed to most of its less established rivals. The entrants have to invest heavily in promotion and advertising for them to attract new customers and maintain their customers. The established brand image has enabled the company to cut on its cost and get increased levels of profitability.

Steady commitment to quality

Strong commitment to quality and product innovation enables the company to get the right experience for their customers. This has been possible through the recruitment of employees with the right skills and knowledge. These employees are further trained to understand the company production strategies. Moreover, the company conducts more market research to ascertain customer thoughts and changing demands.

Expanded market

Coach Incorporation has an active presence in all over America with an expanding presence in emerging markets including China, Japan, and Europe. In the past five years, revenues from sales doubled annually and the company expanded steadily. Analysis of liquidity is necessary as it establishes the ability of an organization to maintain positive cash flow while satisfying immediate obligations.

Market experience

Having been in the fashion industry for over 40 years, Coach Incorporation has acquired enough experience to compete favourably in the industry. It has had sufficient time to learn from its weaknesses and develop long-term strategies that will anchor it through the future of the market. As a way of adopting the emergent technological changes, Coach Incorporation has invested in technological creativity to suit its consumer changing needs. Finally, the company has been able to win more customers with its strategically-placed and ambient stores with conspicuous features.

Industry Profile and Attractiveness

The global luxury goods industry has experienced steady growth as more customers embrace renowned brands such as Dooney & Bourke, Kate Spade LLC, and Michael Kors. The global fashion industry has an estimated market value of over $700 billion. The US and Europe represent 30% of the market share. Despite the economic swing of 2007-2008 financial years, the players in this industry managed to recover and are currently experiencing an average growth of 20% annually. At present, the fashion industry commands 6% of the total market value of the consumer purchases across the globe. The market share is anticipated to expand further to 15% by the year 2015. The fashion industry at present is controlled by Dooney & Bourke, Kate Spade LLC, and Michael Kors, who have managed to establish a household name for their fashion brands. Moreover, promotional services adopted by these companies have spurred the growth of fashion production in the United Kingdom market. In addition, adoption of efficient and reliable technology in the marketing of these products positively skewed the market to the advantage of these retail giants. Based on the annual growth and market share, the incumbents are positioned to benefit in the future because the industry is highly attractive, especially in the emerging markets in Asia and Africa.

Company Situation

Financial Standing

The financial standing of the Coach Inc. has fluctuated significantly between 2007 and 2014. From the balance sheet, it can be observed that the total assets grew from $2.467.12 million in 2010 to $3,663.10 million in 2014. Further, the liabilities rose from $961.82 million in 2010 to $1,242.50 million in 2014. Also, it can be noted that the value of equity followed a similar trend. It increased from $1,505,293 million in 2010 to $2,420.70 million in 2014. However, in the case of income statement, the company reported growth at an increasing and decreasing rate in some years and a decline in growth in other areas. The key issue that Coach is dealing with fluctuations that are caused by the changes in the business environment and competition. From the cash flow statement, it can be noted that the net change in cash deteriorated over the period. The sales revenue generated grew at different rates during the period. The highest growth rate was attained in 2008 where sales grew by 21.75%. The least growth rate was attained in 2014 where sales decreased by 5.30%. During the global financial crisis that is in 2009 sales grew by 1.56% only. The market in which Coach, Inc. operates is quite competitive. The main competitors of the company are Dooney & Bourke, Kate Spade LLC, and Michael Kors. Based on the combined sales revenue of these companies, the change in sales growth was at 13%. Therefore, it can be noted that the industry has reached maturity since there has been very dismal changes in sales over time.

Financial analysis

Profitability

Return on assets

The return on assets improved from 29.79% in 2010 to 33.43% in 2011. It declined to 21.33% in 2014. This implies that the amount of profit generated from a unit of asset decreased over the period. This shows that the profitability and the efficiency in the utilization of the assets of the company declined over the period. This could also be a signal that the property of the company have dilapidated, thus, they cannot engender a considerable amount of returns.

Return on equity

The values of return on equity were high and they improved from 48.82% in 2010 to 54.62% in 2011. However, in 2014, the value dropped to 32.28%. The high values promises the shareholders high returns for their investments. The declining amount of return on equity can also be caused by the increasing amount of long term debt. An increase in debt results in an increase in interest expense.

Liquidity

Current ratio

The current ratio was fairly stable during the period. The value of the ratio was 2.46 in 2010 and 2.44 in 2011. Thus, it can be observed that the company can adequately pay the short term obligations using current assets. This shows that the company has a sound financial standing.

Working capital

The working capital rose from $773,605million in 2010 to $859,371 million in 2011. The value rose further to $1,042million in 2014. It implies that the value of current assets exceeds the current liabilities. The two liquidity ratios were stable during the period. It shows that the company is effective in liquidity and working capital management. This gives confidence to the debt and capital providers.

Leverage

Debt to assets

The value of debt to total assets was stable during the period. The ratio was 0.3899 in 2010 and 0.3880 in 2011. The fractions imply that the percentage of assets that are funded using liability remained stable during the period. The ratios also show that the company maintained a low leverage level during the period.

Debt to equity

The debt to equity ratio was also stable during the period. The value of the ratio was 0.639 in 2010 and 0.6341 in 2011. It is a suggestion that about 63% of the assets of the company are proactively funded through the debt option. The two leverage ratios show that the Coach Company has a low debt proportion in the capital configuration. This gives the company room to take more debt that can be used or growth and expansion. Thus, the company has not fully exploited its potential. The growth prospects will translate to better performance in the future.

Activity ratios

Inventory turnover

The inventory turnover ratio decreased slightly from 10.2 in 2010 to 9.9 in 2011. The value decreased further to 9.1 in 2014. This shows that the number of times that the company replenishes stock did not improve. This could be an indication that the company is trading on slow moving commodities. It could also be an indication of a low level of efficiency.

Day’s inventory

The day’s inventory increased slightly from 35.7 days in 2010 to 37 days in 2011. The value dropped further to 40 days in 2014. This shows that the Coach Inc., take a slightly less number of days before it replenishes stock. This shows an improved efficiency in stock management.

Receivables turnover

The value of receivables turnover dropped from 33.08 in 2010 to 29.10 in 2011. The ratio dropped further to 24.20 in 2014. This shows that the level of efficiency in issuing credit and recollecting deteriorated. Lower values of the ratios indicate that the company is selling most of their commodities on credit.

Day’s receivables

The day’s receivables rose from 11.02 days in 2010 to 12.54 days in 2011. The number of days rose further to 15.08 in 2014. This implies that the number of days taken by the debtors to repay the amounts they owe the company increased slightly. This shows a deterioration of efficiency in efficiency.

Free cash flow

The value of the free cash flow dropped from $1,037.7 million in 2012 to $765.4million in 2014. This implies that the amount of cash available for investment opportunities declined over the period. This limits the ability of the company to grab investment opportunities.

SWOT Analysis

Strengths

The stable and management team comprising of directors and several managers is instrumental towards providing necessary support and guidance in provision of fashion products to customers and reviewing current operational strategies in line with the demands of their clients at the Coach Incorporation. For instance, the management team introduced the online service in response to the demands of the clients. This has enabled the Coach Incorporation to fund different business project initiatives at affordable loan repayment interest rates. The Coach Incorporation also enjoys a wide network with over 45 branches and subsidiaries in the US and several representative offices in different regions outside the US. This is important in attracting more customers in those regions where the company is yet to reach full potential. Besides, the numerous branches have improved its products visibility and accessibility.

Coach Incorporation has been able to increase its level of sales and profits through increased consumer proximities, clear differentiation and segmentation of its brands, through the internationalisation of its business models and expansion of own retail businesses. The strong brand image that has been enhanced by the recent redesign of the company logo and extensive image campaigns has worked for the company. Its urban influence targets consumers who value individual fashion styles that embody a relaxed and easy-going attitude.

Coach Incorporation has increased own retail business in the last few years, particularly in Western Europe and North America. Company owned retail stores have become growth drivers and important distribution points for the company. Coach Incorporation retail stores supplement their wholesale activities which boost the growth potential of the company by deepening relationships with the customers. With company retail stores distributed across the world, Coach Incorporation has control of its brand image globally. The vivid presentation of Coach Incorporation brands through store ambience and image supports differentiated perception by consumers beyond their shopping experiences, further strengthening the brand image. Moreover, the establishment of a strong and reliable online store by the company represents a major growth for the company. The addition of new online stores in markets in North America and Western Europe with customer service and user friendliness significantly improves shopping experience for the customers. The other strength of Coach is efficient customer relationship management strategy. For instance, Coach does free handbag repairs and have customised services for customer interested in specific product that is not currently available in the store.

Weaknesses

The Coach Incorporation has more presence in the US than other parts of the globe. Specifically, unlike its main competitors, the Coach Incorporation has few branches outside the US. Thus, the store does not enjoy the substantive demand in the global market as its customer catchment area is restricted to the boundaries of the US. Besides, the focus of the Coach Incorporation is more on customised fashion brands and products. This is counterproductive in terms of revenue generation since the majority of its customers are small businesses and private individuals who cannot operate in the customised fashion platform. Besides, Coach has high inventory cost since it has many stores across the US. Managing these stores may not be sustainable in the long run if the annual turn over reduces. As a result of these weaknesses, the Coach Incorporation has not been able to efficiently penetrate the small business segment in the US within its Business-to-Business model of operation. Coach Incorporation focus on quality products has compromised its ability to incorporate views of a section of its consumers. A section of the potential consumers feels that the company should produce reasonably priced and quality products for the low end market. However, Coach Incorporation has largely ignored the low-end market for the middle and high class.

Opportunities

The Coach Incorporation has an opportunity to expand its opportunity to cater for expanded fashion apparel since its asset base is strong enough to sustain this market. This opportunity will help in boosting the Coach Incorporation’s revenues and leadership position in the US fashion industry. Therefore, through increasing its online sales via the Coach website, it would be easy to offer customised services to customers. As a result, the Coach Incorporation will be in a position to double its current revenues and increase the customer base. The company’s global presence and strong performance in most regions demonstrate that it can be successful in nearly all countries of the world. It is on this ground that Coach Incorporation plans entry into the regions where its presence is not yet felt. Secondly, working in collaboration with subsidiary companies enables ease of entry into new markets.

Threats

The main threat to the survival of the Coach Incorporation is the competition from counterfeit products that may act as direct substitute to its brands. Thus, the expansion and market penetration strategies that the Coach Incorporation proposes are likely to face opposition if these fake products are expanding their market share. Coach Incorporation is faced with fierce competition from its rivals, which requires adoption of more vigilant strategies. The soaring demand for raw materials across the world may prompt suppliers and independent producers to increase the prices, resulting in high costs of production and lower levels of profitability. Political issues in different markets, such as corruption may threaten the company from achieving its profitability objectives in the market.

Generic and Grand Strategy Recommendations

Operational efficiency and market niche provide an indication of how well the company manages its resources, that is, how well it employs its assets to generate sales and income. It also shows the level of activity of the corporation as indicated by the turnover ratios. The level of activity for Coach Incorporation has remained relatively stable over the five year period, despite threat of counterfeiting, increased taxation, competition, and constant change of taste and preference. In order to stay afloat, their competitive price, which is half the price offered by competitors, has ensured that it remains the choice for middle class income earners yearning for quality and luxury at low cost. However, it is apparent that Dooney & Bourke is presenting a serious challenge on price competitiveness. Therefore, in order to remain competitive, the company should implement focused product differentiation strategy by applying concentration, market development, product development, vertical integration, market penetration, and retail distribution as grand strategies.

Product concentration

Approach

The Coach Incorporation should ponder concentration to its products in countries which do not have strict laws that protect the business, when expanding further to other foreign markets. Countries like China do not have strict rules which protect business entities from being copied by competitors. This will help in safeguarding its products’ brands and making sure that it targets specific market segments.

Objective

To ensure that Coach introduces measures in its operative process that would make it distinct in the market from any firm.

Implementation

The introduction of product concentration should be applied while ensuring that the targeted markets, especially in Europe, have customised apparel that is unique to that region. The key performance indicator will be increased revenue in European market by 6% in the first year of implementation and 10% there after. Therefore, product concentration will position the Coach Incorporation as a strong incumbent brand in the global fashion goods industry.

Vertical integration

Approach

The Coach Incorporation may partner which medium businesses retailing products similar to those of its competitors.

Objective

To expand Coach’s market and make it easy for customers to access the products.

Implementation

The above objective can be achieved through created on in-house production, supply chain, and marketing strategies. When properly implemented, the company is likely to counter the strategy of its competitors, such as Dooney & Bourke, Kate Spade LLC, and Michael Kors, of reaching the customers through proxy retailers. The choice of vertical integration is driven by the need to create that perception of reduced inventory costs. The key performance indicator will be reduced inventory cost by 10% in the first year of application since costs related to running the business are expected to drop. This strategy takes some initial costs to develop the integration concept but the advantages are ability to legally protect the product, creation of some barriers to competition, and general promotion of customer loyalty.

Innovation

Approach

Cost leadership strategy is vital in business management, especially in an industry with stiff competition, such as the Coach Incorporation. The company may penetrate the African and Asian markets further through introduction of customised apparel that target different market segments such as direct customers, retailers, and fashion agents through an innovative approach.

Objective

To adopt the market leadership strategy to improve Coach’s product quality and appearance

Implementation

The above objective is achievable through creation of different high quality products and distinctive brands. As a result, this venture will develop a cumulative experience, optimal performance, and product availability through application of alternative technology and human skills. The key performance indicator for this strategy is the ability to create a new product, thus increased number of customer ratings by 3% after the first year of implementation.

Product development

Approach

The transfer of brand knowledge is enhanced by other factors that include awareness and image. It is an area that continues to fascinate considering the interconnection between the recognition, recall, uniqueness, and positive attributes. Growth in brands is mainly subjective in nature meaning that the internal environment has the greatest influence. In the case of the Coach Company, retail store image facilitates easy identification of customer responses to external stimuli, branding of private store labels, and evaluation of the marketing strategies that is used to promote store’s brands. The store’s brands will benefit greatly from the improvement of overall production quality and marketing support as much as it is done from evolving purchasing habits based on the rapid changes in geo-demographic and psychographic behaviours of the customers influenced by what they see. Therefore, this recommendation will be instrumental in achieving focused product differentiation.

Objective

To bridge any quality concern and introduce more product brands in the market.

Implementation

Essentially, the bridging of quality concerns between store and name brands will reduce the reputation gap leading to increased propensity of store brands. Specifically, the brand logo will remain instrumental in the marketing strategy in the fashion industry. The possibility that consumers could consider switching brands is important in increasing brand awareness. In essence, a brand involves; name, packaging, advertising, consistency, and reliability. It involves the symbol(s) of identification of a product or service that seeks to establish a degree of differentiation between it and other similar products and/or services. It is vital part of establishing healthy brand equity. The performance indicator for this strategy will be successful introduction of a new product line within the first 36 months after implementation.

Market development

Approach

From the brand personality analysis, it is apparent that Coach Company does not have the ideal and strategic image branding. The store should be more welcoming, very dynamic and lively to shop in. Being in the competitive fashion industry, the store should have high score on sophistication since the target market segment consist of very choosy clients who would want the best in the market to fulfil their status quest and remain elegant. As a result, it will create an intrinsic motivation response that triggers the mind to activate affiliation, self acceptance, and feign community feeling of belonging to the Coach brands.

Objective

To expand the current market Coach into the Asian market

Implementation

In market development, planning is critical, especially in a dynamic market controlled solely by customer preference and perception. In sales forecasting, the stores should assort their merchandise according to the lifecycle of each category. For instance, the seasonal winter items such as heavy clothing for the companies are categorised as slow movables. Besides, the latest fashion design products are categorised in the exclusive purchase segment in the stores. Basically, the assortment adopted should be informed by past volumes of sales and customer responses to periodic surveys by the company. When the brand image is increased, the visibility of the Coach’s products will also increase. The performance indicator for this strategy would be the ability to successfully increase the current sales volume by 5%.

Concentric diversification

Approach

An improved approach to product management through diversification will improve the visibility of the Coach brands. The buyer will make an effort to learn the Coach’s values, vision, challenges, and operating environment. A spirit of collaboration established will offer positive contribution to the partnering businesses when different products are launched. Such cooperation will turn new brands into a competitive advantage instead of a cost.

Objective

To improve the current product brands into efficient product that is diversified.

Implementation

Towards implementing marketing function, the product diversification strategy should constantly employ elements of marketing mix to appropriate plans on how to achieve the popularity in the market place. These strategies are aimed at promoting positive consumer behaviour through introducing more brands. The key performance indicator for this strategy would be increased sales by 3% as a result of improved product brands.

Conclusion

Generally, Coach Incorporation has been largely successful in the market, and bears ability to competently survive in the market. Incorporation of the Porter’s market forces in the management of this successful New York based fashion store is directly linked to its consistency, profitability, and efficiency. Successful execution solely functions of inclusiveness, creation of quantifiable tracking devices for results, and recruiting an informed support team. The management only needs to utilise all its available strength and implement opportunities to emerge as the world number fashion house. It is thus evident that Coach Incorporation operations are on the right course and there is little need to make new recommendations for the company operations. Generally, these recommendations should be practiced flexibly since the Coach Incorporation’s operation environment is characterized by constant dynamics that may make previous designs irrelevant.

Appendices

Appendix 1 – Summary of the Five-Force Analysis

Appendix 2 –SWOT Summary

Appendix 3 – Performance of competitors