Company History

Billabong International Limited (BBG) was established in the year 1973 in Australia’s Queensland by its present director Merchant Gordon (InvestSMART 2011). According to the statistics availed on its website, its core operations include production, distribution and retailing of garments, accessories, collections and wetsuits (Billabong International Homepage 2011). As of 2011, the company had carried out aggressive marketing strategies and established an active presence across 60 countries (MSN Finance 2009). This diverse geographic expansion has greatly reduced the seasonality of their earnings thus in the process giving the company a competitive edge over its major rivals (Nike and Quicksilver).

Introduction

The negative effects associated with globalization have heavily affected the operations of multinational corporations, Billabong included. It should be noted that in its efforts to overcome the challenges associated with economic crunch or inflation, the Australian based firm had previously borrowed unsecured bilateral loans to refinance its activities and improve on its liquidity (Interactive Investor 2008).

It is from the need to carry out its expansion program that this paper proposed the following 3 suitable funding facilities (commercial loan, US bonds and factoring) for this multination corporation. In most sections, the study went into detail to identify and describe the proposed funding facilities key aspects.

It should be noted that while proposing the 3 funding facilities in this case study, Billabongs’ latest financial statements were regularly referred to especially when studies were carried out to determine the amount of funding which the surf wear firm was liable for from the various lenders/factors.

Billabong International Ltd: Identification of 3 suitable funding facilities and a description of their key aspects

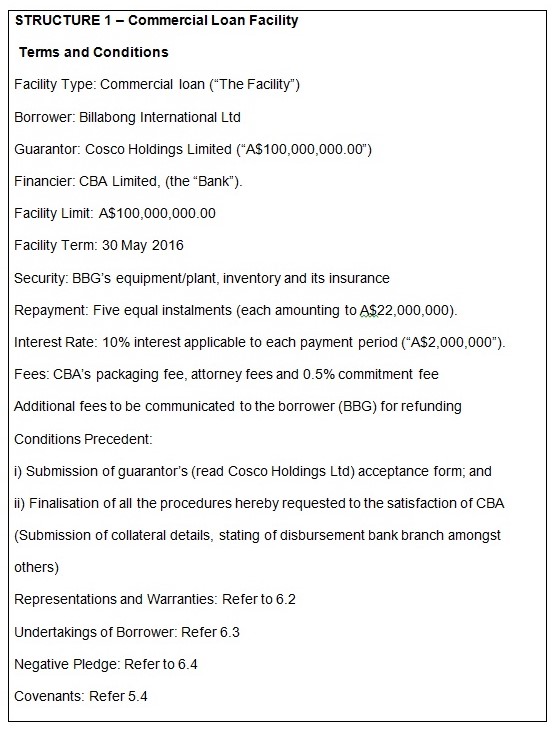

Commercial Loans

Billabong International Ltd can approach financial institutions and request for commercial loans for funding. The following are the guidelines adopted by most financial institutions in the process of reviewing or processing borrowers’ loan requests.

The proposed pricing pattern

In the case of commercial loans, financial institutions adopt varying patterns to loan pricing. Amongst factors affecting the pricing of commercial loans are the borrower’s stated request, pay-back timeframe, fees and individual lending institution choices.

Fees (Closing costs)

The following fees, which are associated with the application, processing and disbursement of any funding request, have been detailed by most lending institutions: packaging fees, attorney fees, commitment fee, taxes and other general expenses for instance document-search verification services.

Contract Clauses

The management team of Billabong international are reminded that their multinational firm will be required to achieve and sustain/maintain contract clauses relating to all funding aspects (lending commitment, disbursement, warranties and representations, and covenants amongst others). Some of these clauses have been detailed in the respective named aspects in this case study.

Covenants

The lender will use the covenants with the main purpose of requiring the borrower (in this case BBG) to accomplish the necessary things associated with repaying the loan. From the above perspective, most lenders’ propose to adopt and implement the use of the following restrictive covenants to any borrower:

Use of the loan proceeds

The lender will make a follow-up to ensure that the borrower uses the proceeds for the two stated reasons.

Government authorizations

The lender will require the borrower to make, obtain and store in the full force all authorizations pertaining to this agreement with the Australian government authorities. As such, these authorities will accent to the validity or monitor the repayment of the loan by the borrower.

Financial Statements

The borrower shall furnish the lender with all its financial statements on a regular basis. For instance, as previously stated, BBG’s end of financial period has always been on the 30th of June and for such. As such, a lender can decide to provide the management with a 30 day working period upon which the financial statements should have been furnished to it for analysis and review. As such, the lender will be fully informed on the financial status of the borrower.

Inspection Rights

The lender will also require the borrower to enable its representatives from the financial department to examine their records and property times considered reasonable or appropriate to them. For instance, if the lenders’ Chief Financial Officer considers that the information presented in the financial statements is or appears to have been tempered with; he may request his team to perform an audit analysis at the firm’s premises. The rights to do so are always determined by the borrower.

Default Notices

The lender will require any borrower (read BBG) to promptly give notices of any impending repayment default or any other events that may constitute adverse effects on their ability to undertake obligations to service the loan on a timely manner. This will help the two parties prepare on their next course of action which include amongst others the lender granting the surf wear firm a grace period.

Insurance

Having presented the company’s insurance amongst its collaterals, the lender will require that the borrower regularly services this insurance with a reputable and financially sound insurance company. The risks covered in the insurance clause should be related to risks affecting similar surf wear companies in the world. This may include the burning down of company premises.

In doing this, the lender believes that it will be in a position to claim parts of its resources in case of the borrower becoming bankrupt.

Maintaining of positive ratios

The lender proposes that the borrower shall maintain a positive ratio of current assets to current liabilities. Most lenders’ recommended ratio is that of less than 1.5:1.

In addition, the borrower, at all times, should maintain debt to equity ratio of not more than 1.5:1. This will ensure that it will always be in a position to comfortably service the impending loan.

Collateral

Based on MSN Finance (2011), BBG possesses property, equipment and a host of plants spread in the 60 countries. In addition, the company has an insurance that can be used as collateral. Since all these items fall with the stated standards for most lenders’ collaterals, the company can use can offer these assets as its collaterals to match its future loan requests. The values of these collaterals are determined based on the existing competitive market prices.

Assessment of Repayment Ability

Debt worthiness

From BBG’s last financial statement (2010), the company’s debt ratio for the financial years of 2008, 2009 and 2010 was 29.73%, 25.12% and 19.25% respectively. The last figure (19.25) if truncated in decimal point form will add up to 1:5. This figure is unfavourable to most lending institutions since most lending institutions stipulate that the lender should have a 3:1 or less debt ratio.

Cash flow analysis

Most research have evidenced that the ability of any borrower to service the proposed loan from the borrower’s resultant earnings and cash flows is a critical key factors that should always be considered in the loan structuring process (Marks 2005, p.290).

According to BBG’s latest results, the following table depicted its cash flow structure:

Table 1: depicting Billabong’s recent cash flow structure

Bar graph 1 depicting BBG’s cash flow structure (note that series 1 represents financial cash flow, series 2 represents operating cash flow while series 3 represents investments cash flow)

From the figure above, the author notes that BBG has established a successful model that can allow it to service commercial loans. Most lending institutions stipulate that the lender should have a positive operations’ cash flow to comfortably service loan and interest expense repayments. From the figures presented, BBG had a steady increase in the amount of operational cash flow.

Best Case/Worst case analysis

In further assessing the risks to be incurred by financial institutions in offering commercial loans to BBG, the following best case and worst case analysis was conducted on its financial statement. The table below shows the company’s last financial results

Table 4 showing BBG’s last financial results (Adopted from MSN Finace 2011).

In scenario 1 of a best case analysis, assuming that BBG’s revenues increase by 20% and that all its items are directly affected by these increase in sales, this will mean the company’s succeeding proforma income statement can be projected as follows:

Table 5 showing the projected best case analysis.

From the scenario displayed above, it should be noted that the company’s net income will not sufficiently service the proposed A$600million loan in the recommended five year period.

Likewise, if we were to perform a worst case analysis and reduce the revenues by the same margin of 20% for the succeeding year, the following Table 6 depicted the results of the findings:

Table 6 depicting the projected worst case analysis.

From the results shown above, it’s obvious that the company lacks the strength to service the proposed loan. The figures highlight that the company can only be able to comfortably forward an annual payment of say A$50 million. This means that if it is awarded a high figure as it loan request, then a very lengthy repayment period should be offered to it by a lending institution. This may worsen its creditworthiness.

Repayment

Based on the analysis done above, BBG had a reducing leverage ratio. The company’s debt to equity ratio reduced from 61% in 2008 to 35% in 2010 while its debt to total assets ratio reduced from 30% from 2008 to 18% in 2010.

This reducing trend might be welcomed by commercial loan lenders. However, its weak debt coverage service and unhealthy ‘best and worst’ scenarios reveal a lot of weaknesses in its financial capabilities. As such, the author hereby proposes that BBG’s financial team should engage any loan lender in comprehensive discussion to be awarded a competitive period for the repayment of any disbursed funding amount.

The excel sheet below (in section 5.8) show an example of how financial institutions calculate the total repayment amount for any disbursed funding request.

Interest charged

Billabong International should be notified that interests vary depending on the amount borrowed. The interest can also be fixed or on floating terms. For instance, the following can be noted of a fictional loan request. Taking BBG’s proposed repayment pattern as lacking the option of a down payment and the amount disbursed for funding as A$100 million, then BBG will be required to repay A$20 million plus 10% of 20 million in each instalment, five times to offset this disbursement.

The following figure depicted the truncation above:

An excel worksheet showing a proposed interest and repayment pattern.

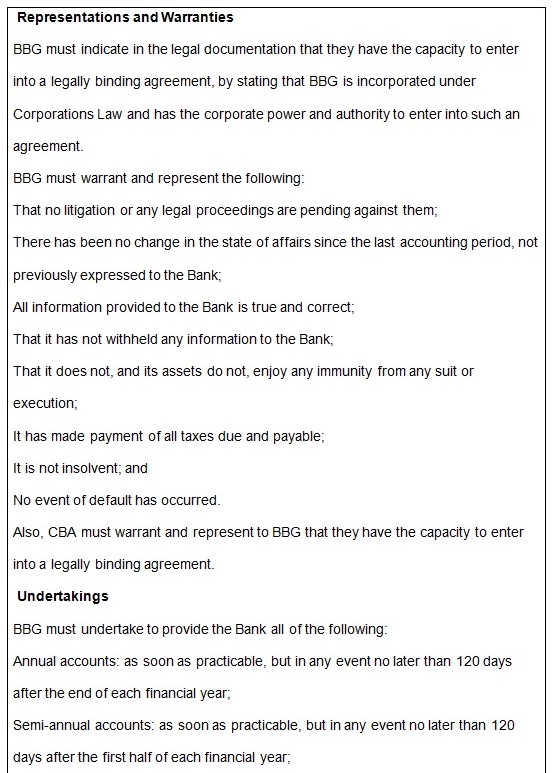

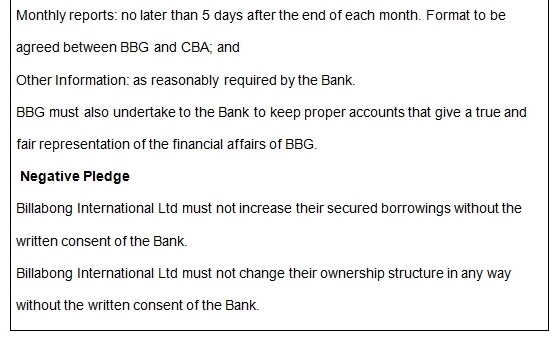

Sample Term Sheet

The following sample term sheet has been compiled with reference to Billabong international engaging in a commercial loan facility borrowing.

Events of default/risks and their mitigation

The following have been considered as events of default in commercial loan transactions;

The failure by the borrower to service the annual repayment amounts. In such a case, the lender, having been un-notified of the action will take any necessary action to reclaim its amount. For instance, CBA may decide to initiate and engage legal proceedings against the company. The costs of such proceedings will also be taken care of by the accused.

Moreover, if the borrower fails to implement or adhere to the above stated covenants, then this will be considered as events of default. In such cases, legal proceedings will also be initiated on the borrower for having violated the loan agreement.

Ideally, if a lender in its efforts to determine the correctness or the truthfulness of the warranties or representations presented by the borrower for securing the loan finds that incidences of lying were engaged by the borrower, then this will also constitute a default event. As such, the lender will carry out its own evaluation to determine who the correct warranties and representations were. Such incidences will lead to automatic cancellation of the engagement.

Tellingly, the dissolution of the borrower or its involvement in bankruptcy cases will constitute events of default. As such, the lender will engage its team of legal experts to oversee the sale of the collaterals provided to reclaim its value of capital.

Beside, the disposing off of collaterals by BBG will also be considered events of default. To mitigate such risks, a court injunction will be imposed on the availed collaterals to prevent their premature sale.

Conclusively, it should be highlighted that the proposed loaning structure constitutes a best tool for the lender evaluating their potential loan clients. Other than securing its funds, it should also be noted that this structure will also be of great benefit to the various borrowers since it provides for conditions that limit their credit unworthiness thus enforcing their stability.

US bond

Billabong’s Chief Financial Officer should be informed that US bonds can constitute suitable funding facilities for the expanding firm. In this case, BBG, through its expanded US branch can offer its bonds to trade on the domestic US market. In this case, the bonds will trade in the denominated US currency ($). At the time of the bonds maturing, the company can receive the hedged funds in the form US dollar currencies and distribute to its various branches for funding. The use of this proposed funding facility will be a welcome idea to the company’s management. This is so because the author established that the firm has been known to fund its operation by use of US bonds in recent times thus constituting some degree of experience in using this form of funding.

The following benefits are likely to accrue to BBG in using this form of funding:

- The company stands to attract many investors since research has shown that 84% of the bond market is USD (University of Michigan 2010).

- Beside, as Kyle (2010) noted, the multinational firm stands to ‘spice up’ its portfolio by adding foreign contents on its portfolio. As such, this can act as alternative strategy for investment. This is because the purchasers of its bonds will be mostly the foreign (US) residents.

- Moreover, evidence shows that US bonds form a natural hedge because of their denomination in the domestic US currency (Investopedia 2009). As such, BBG is likely to gain if the USD fell in comparison to the foreign currency (A$) to which the company is likely to convert its matured bond into.

- To end, the company is likely to fetch higher rates of return. This is the case because as Investopedia (2009) puts it, historical returns have evidenced the notion that global-fixed-income investments tend to possess higher rates of returns on the US market (returns of up-to 7%).

Pricing of US Bonds

Melnik and Nissim (2003) in their research established that US bonds are priced based on bond’s credit risks and maturity (p.278). For instance, if US treasury offered bonds valued at $500 million to BBG, the two parties can enter into an agreement that will allow the borrower (BBG) to repay the amount in a 10 year maturity period. In such cases, a positive 6% annual return can be forwarded to this investment.

Likewise, the prices of US bonds are also determined by the current market conditions and the borrower’s financial stability.

The author notes that financially sound companies can fetch high funding from offering international bonds. For instance, India’s largest private lender ICICI Bank had announced (on May 20, 2011) that it had raised a whooping $1 billion through issuing international bonds for a 5.5 year period (Moneycontrol Bureau 2011). These bonds had been offered from its Dubai branch to the US and UK markets had had a coupon of 4.75% and issue price of 99.665%. Due to reputation, the bonds had been interestingly oversubscribed by $2.7 billion (Moneycontrol Bureau 2011).

Fees

Since most US bonds are exempted from domestic taxing, BBG’s bonds are likely to attract transactional fees. According to Melvic and Nissim (2003), these transactional fees include those attained when the arranger (the lead bank) draws up an agreement thus leading to the claiming of a management fee (p.281). This management fee accounts for the services of compiling an ‘information memorandum’ (term sheet), negotiating the borrower (BBG’s) conditions and the preparing of necessary documentation for bond issue. BBG should note the discussed management fee burden is usually shared amongst all syndicate members.

Covenants

From their research, Dailami and Hauswald (2003) noted that debt covenants have evolved in recent times to mitigate adverse consequences associated with firms with bond-holders engaging in additional risky debts thus interfering with their capital structure (p.9). Covenants in the context of BBG’s bond funding will be contractual devices intended to prevent the occurrence of conflicts of interests between BBG’s bond-holders and its equity holders.

In their research, Dailami and Hauswald (2003) found out that a sample of bond covenants contained usual covenant provisions that mitigated typical shareholder conflicts for instance dividend policies, asset substitution (between bond-holders and shareholders), underinvestment and claim dilution (p.10). To be specific, some of these covenants may include restrictions or provisions to use of funds, asset sale/leaseback, additional indebtedness, adhering to regular reporting requirement, collateral value preservation, and dividend and debt-service coverage ratio restrictions amongst others (Dailami & Hauswald 2003, p.12). To add a more restrictive covenant, bondholders insist that cash flows should be maintained at sound levels.

Contract clauses

BBG will be required to maintain contract clauses relating to all aspects of bond funding (term sheet, covenants, and collaterals amongst others). These clauses have been discussed in their respective areas of this case study.

Collateral

In using US bonds, Billabong International stands to benefit from the collateral services offered by US Federal Reserve banks which act as fiscal agents for the US Treasury. Under this program, BBG will be required by the US law to pledge acceptable securities as collaterals. These securities can be deposited at any Federal Reserve Bank. Collaterals are valued by the bank according to the existing market price or outstanding principal balances. Financial/bank guarantors and insurance or re-insurance policies can be acceptable as surety bonds in this case.

Repayment and Interest

The repayment pattern is determined through a mutual agreement between the various parties involved in the bond transaction (in the case of the US bond; the borrower, lead bank and the US treasury). US bonds repayment lengths have been established to vary between 1 and 10 years with a floating interest rate compounded mostly on a semi-annual payment mode.

In US bond funding, BBG management should be notified that the kind of interest rate that exists is commonly called coupon interest rate (Brigham & Ehrhard 2010, p.176). This type of interest will be arrived at when BBG will be required to repay fixed amounts of dollars of interest (coupon amount) on a semi-annual basis. This coupon amount will be divided by the par or stated value to arrive at the stated coupon interest rate. For instance, if BBG will acquire bonds whose stated or par value will be $1000. A submission of a semi-annual interests of $100 can be forwarded to the company. This would mean that the company’s coupon interest will be $100, while its coupon interest rate will be calculated as $(100/1000) which will be 10%.

Risks involved and their mitigation

BBG is informed that venturing into foreign bonds is quite risky. This is because the fund’s prices can drastically reduce thus causing heavy losses to the parties involved especially in instances of negative fluctuation in the foreign currency in which they are trading. For example, the maturation of the bonds can correspond with the fluctuating in foreign currency prices thus meaning that the borrower (BBG) will have adverse effects on its payouts, dividends as well as its performance. As Kyle (2010) noted, the greatest risk associated with this kind of funding is that it deals with unforeseeable claims.

Though this risk has proved elusive in its mitigation, it is advisable that BBG should carry out detailed analysis of the market analysis to determine the strengths and weaknesses of the US bond market to determine is viability for investment.

Factoring or invoice discounting

Moreover, BBG can decide to adopt the factoring method whereby the company may seek the services of a reputable debt collector firms to collect all its widely dispersed international debts/accounts receivables. In this case, the company’s debt assets will be will be leveraged by factoring firms to provide it with an instant of needed cash to fund its business operations.

To emphasize, BBG may negotiate with a lender for the sale of its debts or sales invoices. In addition, the company may as well relinquish the ownership of its debts to the lender at agreed upon fees. In this case, the lender will issue it with the proposed and approved amounts to fund its activities (Lincoln Finance Ltd 2011).

From its recent end year reports, BBG had recorded a steady increase in its days’ receivables (these were 76, 81 and 95 for the respective years of 2008, 2009 and 2010). This scenario justifies the author’s call for BBG to implement debt factoring.

Pricing and fees

The author notes to the BBG management that this is a suitable funding facility since there has been rapid emergence of factoring companies which have spread across the World’s strongest economies. This exodus has meant that the costs associated with this form of funding have had to vary as the factoring companies try to be competitive to woo more customers.

However, general pricing ethos is similar to most factoring companies. BBG should note that that the greater it’s factoring workload, the greater the pricing/fees. Its workload will be determined based on the sum of invoices generated by the company. An adjustment fee will then be calculated to cover for the risk involved in advancing the money to BBG. This will constitute a service fee which will normally be expressed as a percentage of BBG’s turnover.

Factoring companies also charge an advance rate on the sum advanced. In line with this, the author proposes that BBG adopts longer payment terms to benefit from the one-time factoring flat fees.

Covenants

BBG should be informed that this form of funding does not call for adherence to financial covenants, which makes its one of the most suitable funding method. This is so because the only concern for the factoring companies will be the credit worthiness of BBG’s invoiced customers.

Collateral

For factoring, BBG can pledge all its account receivables (debts) and any (general) intangible assets as its collateral for this form of funding. In most cases, the main collateral will be BBG’s invoice of finance. Very few factoring companies will require BBG to use the secondary or the intangible forms of collateral.

Repayment and Interest

The author points out to BBG management that factoring not been a loan, lacks repayment or interest aspects.

Contract clauses

The factoring company and BBG will be required to adhere to the contractual rules relating to the pricing and fees as was highlighted above.

Risks and their mitigation

The author notes that factors may forward high commissions and administrative fees thus eating into and lowering the value of BBG’s account receivables. To mitigate on this, BBG should source for competitive factoring rates from reputable factors.

BBG is likely to lose control of its ledgers since it is likely to forward the collection of its account receivables to strangers (factors). To mitigate on this, the company should ensure that it partially adopts the use of this funding facility.

By engaging factors to collect debts on its behalf, BBG is likely to loosen its already strong customer relationship/bonding. Some customers who may wish to deal with the company on a direct basis may express their disapproval with BBG’s factoring mode. They may even terminate their allegiance or membership with the surf-wear firm. To mitigate on this, BBG should ensure that it maintains contact with its customers even if it engages factors to collect debts on its behalf.

References

Billabong International Homepage, (2011) Products [online]. Web.

Brigham, E.F. & Ehrhard, M.C. (2010) Financial management: Theory and practice. 13th ed. USA, Cengage Learning.

Dailami, M. & Hauswald, R. (2003) The emerging project bond market: Covenant provisions and credit spreads. World Bank Policy Research Working Paper [Online]. Web.

Interactive Investor, (2008) Australia’s Billbong gets A$600 million loan [online], Reuters. Web.

Investopedia, (2009) Spice up your portfolio with international bonds [Online]. Web.

InvestSMART, (2011) Billabong International Limited (BBG) [online]. Web.

Kyle, (2010) The pros and cons of foreign bonds [online], Amateur Asset Allocator. Wev.

Lincoln Finance Ltd, (2011) Flexible options for asset finance [online]. Web.

Marks, K.H. (2005) The handbook of financing growth: strategies and capital structure. New Jersey, John Wiley and Sons.

Melnik, A. & Nissim, D. (2003) Debt issue costs and issue characteristics in the market for U.S. Dollar Denominated international bonds. European Finance Review, 7(2), pp. 277-296.

Moneycontrol Bureau, (2011) ICIC bank raises $1 billion overseas bond issue [online]. Web.

MSN Finance, (2009) Billabong International Limited [online]. Web.

MSN Money, (2011) Financial results: Billabong International Ltd [online]. Web.

University of Michigan, (2010) Chapter 12: International bond market [Online]. Web.