AMF

The Autorité des marchés financiers (AMF) is an institution that was set up in August 2003 to regulate the financial institutions in France. It protects investors by ensuring fair financial practices in the different companies. It is an important body due to the role it plays in integrated financial markets in the areas of insurance, securities, deposit taking institutions and other financial related companies. It has ensured that the information disclosed in the financial statements is reliable. It ensures laws on financial reporting are adhered to.

European Union’s Fourth Directive and IAS 1

The IAS 1 and the EU fourth directive require companies to provide a fair view of the company’s financial performance. Companies are required to provide four kinds of information, the profit and loss account, balance sheet, cash-flow statements and notes to the financial statements. In the balance sheet, there should be a distinction between the current and non-current/fixed assets shown in the order of their liquidity. Similarly, there needs to be a distinction between the current and long-term liabilities (European Commission, 1998). IAS 1 requires the company to also show the changes in equity. The LVMH Company has shown all these statements and explanatory notes in their annual report.

Legal Reserves

These are statutory reserves where the financial institutions such as banks, insurance companies, building societies and credit unions are expected to segregate a certain percentage of their deposits and keep in a reserve. This portion of money should not be used to pay depositors. According to the French GAAP, the company must transfer 5% of its retained profits to a legal reserve till it reaches 10% of the company’s share capital. In the United Kingdom, the GAAP does not require the creation of such a legal reserve. The practice is not common.

LVMH’s accounting policies and US GAAP

The LVMH Company has used IFRS in the preparation of its financial statements. There are certain similarities and differences between the IFRS and US GAAP. In the treatment of leases, the leases can either be financial or operating leases. The LVHM has disclosed details of both its financial and operating leases. In determining whether a lease is a finance lease, both standards have common determinants. If ownership transfers to the lessee and there is a bargain option in the agreement this is a finance lease. Where the life of the lease term may be equal to the majority of the economic life of the asset the lease should be classified as a finance lease (Deloitte, 2007)

If the present value of the minimum lease payments are equal to the 90% or more of the fair value of property, this lease will also be considered as a finance lease. The US GAAP however is specific on the amounts and measurement criteria in determining finance lease. The lessee’s guarantees of the lessor’s debt are not included in the minimum lease payments. Secondly the US GAAP excludes the executory costs such as insurance, maintenance and taxes from the minimum lease payments. The IFRS include both amounts in their calculations (PriceWaterHouseCoopers, 2008).

In the area of property, plant and equipment, the similarity between IFRS and US GAAP is that the assets are initially recorded at the historical cost in the financial statements. In the future, under the IFRS, the asset can be re-valued where the prices have gone up or down. In US GAAP, however, the company is not allowed to revalue the asset above

the historical cost. The LVHM could use historical cost or fair value accounting and they choose to use historical cost.

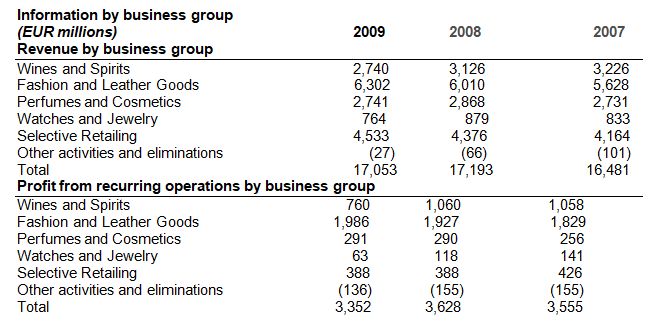

Market Segmentation

The financial statements have been disclosed the different business segments by product and geography as follows:

As shown above, the company is engaged in selling four main products, wines and spirits, fashion and leather goods, perfumes and cosmetics and watches and jewellery. The company also engages in selective retailing. The revenue and profit from each of these segments has been disclosed. The company has also disclosed the following information:

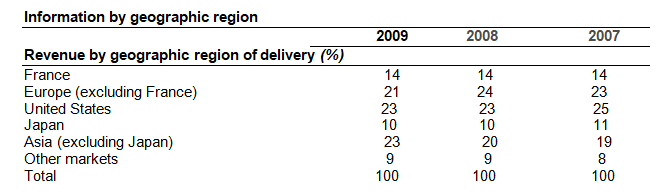

The company has highlighted the major five geographical markets such as Japan, Asia, Europe (France highlighted separately) and the United States. Other markets include other areas not mentioned.

The Global Compact

The company has mentioned that it is a signatory of the United Nations Global Impact. The Global Compact is a strategic policy that businesses around the world can choose to adopt. The companies have a choice whether to align their operations to universally accepted guidelines in sensitive areas such as human rights, employment, anti-corruption and environment awareness (Dilek and Husoy, 2007). The operations should not have incidences of forced labor, child labor or suppression of collective bargaining. There should not be discrimination when it comes to labor. The company should strive to adopt environment friendly technologies. There should be no bribery or extortion practices in the workplace (Nason, 2008)

Social responsibility and Environment disclosures

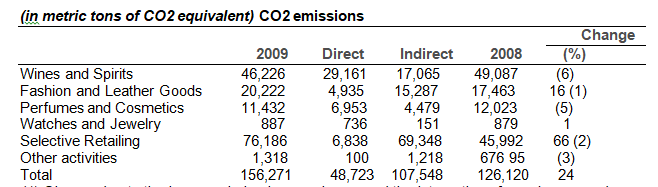

The company has disclosed environmental impact of their product in at least ten categories as follows. The green house emissions data was as follows:

- Change due to the increase in business volumes and the integration of new Loewe and Louis Vuitton sites.

- Change due to the integration of new DFS stores and new Sephora North America stores.

- Change due to the integration of Les Echos and new Moët Hennessy buildings.

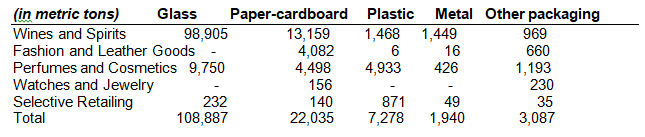

The company has shown the direct and indirect emissions and compared the total emissions with the previous years. Where the emissions increased, the reasons have been disclosed. The company also showed the raw materials used in terms of packaging for the products as follows:

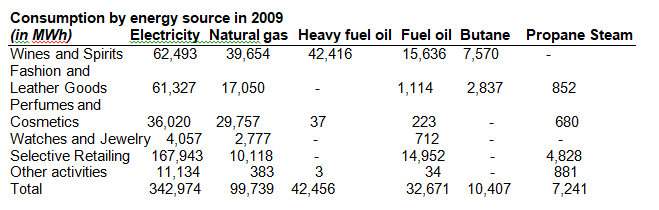

The public have also been concerned about the energy usage by companies and the company has also disclosed its figures as follows:

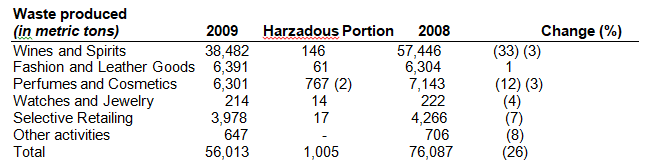

The waste produced by the company operations was also shown and the adverse variances highlighted as below:

Waste produced

- Waste to be sorted and treated separately from other “common” waste (boxes, plastic, wood, paper, etc.).

- Some products that are removed from the manufacturing cycle are treated in the same way as hazardous waste to prevent counterfeiting attempts.

- Decline due to the decrease in business volumes and to the disposal of Glen Moray for the Wines and Spirits business group.

The preparation of perfumes and cosmetics causes excessive release of water that leads to a build up of algae and other aquatic plants. These plants reduce water oxygenation which can be disastrous. The parameter measured is the Chemical oxygen demand (COD) which the company has disclosed as follows:

- Change due to the increase in business volumes and the improvement in the measurement of discharges at a Glenmorangie site.

- Change due to the decrease in business volumes and the improvement in the monitoring of discharges.

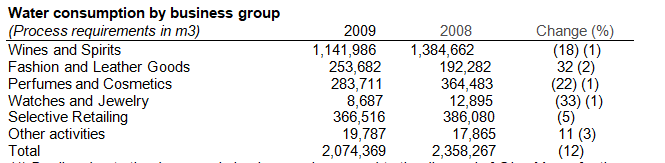

Water consumption which is monitored by local authorities has also been shown as below:

- Decline due to the decrease in business volumes and to the disposal of Glen Moray for the Wines and Spirits business group.

- Change due to the increase in business volumes and the integration of new Loewe and Louis Vuitton sites.

- Change related to the integration of Les Echos and new Moët Hennessy buildings.

The company has also disclosed the efforts they have made towards soil conversation. The company has reduced use of insecticides and has adopted better technology known as Pheromone confusion. The company is also engaging in integrated grape growing practices. Sheep are allowed to graze in the vineyards in the winter to reduce use of herbicides.

The company is also committed to the protection of endangered species of plants. The company partners are required to highlight the bio-diversity and bio-availability of every plant used. The company has policies not to use endangered species but to use common plants or those specifically grown for the production of the specified good.

There has also been growing concerns on animal testing and cruelty and the company has chosen not to test its perfumes and cosmetics on animals but rather it has developed alternate testing solutions particularly when it comes to the allergy tests.

Culture in Hofstede Masculinity/Feminity and Gray’s Notion of Secrecy

According to Hofstede when it came to the culture in different organizations or countries, there were those which are masculine while others are feminine. A masculine culture favours ambition, success and acquisition of wealth (Vitell, Nwachukwu and Barnes, 1993). The United States scored highly when it came to the masculinity aspect. The American society favours an attitude of winner takes all and a person should be the best that he or she can be.

Everyone wants wealth and influence to raise their status quo. France however scored highly in the feminine aspect since the culture favours dialogue and conflict resolution at the work place (Mihaela, Claudia and Lucian, 2011).

The underdog is looked upon with pity. People are not flashy with their wealth. The country values quality of life. The people work for 35 hours per week. The welfare system in the country is also great. Companies in the country will tend to be feminine which is proven by the LVMH group. The group is concerned with quality of life encouraging human rights and great labour practices in the workplace. The environment affects quality of life and the company strives to ensure that the technologies it uses is environment friendly.

Gray in 1998 identified that the sub culture of an accounting company can be analysed according to the parameters of secrecy verses transparency, uniformity verses conformity, professionalism verses statutory and lastly optimism verses conservatism. The first two parameters concern authority while the last two are concerned with the disclosure of financial information in the financial statements. He put forward that the country’s social culture influences the values that the accountants will have in the individual companies (Finch, 2007). France as per Hofstede has a feminine culture which promotes financial disclosure rather than secrecy. The LVHM financial statements prove that Gray’s theory is true.

Financial Ratios

Current Ratio = Current Assets/Current liabilities

It is a measure of the liquidity and the soundness of cash management practices in the company.

2008 Current Ratio = 10,354M/6,615M = 1.57

2009 Current Ratio = 10,975M/6,048M = 1.81

In 2008, the ratio is lower. There are certain associated costs when a company has low liquidity such as the inability to pay creditors on time and taint on the reputation of the company (Wright, 1978). The company’s liquidity improved in 2009. The company’s recommended liquidity ratio in the industry is 2:1. The company should aim to increase liquidity. However it should guard against holding excess cash as this reduces amount used in investment (Kamath, Khaksari and Hylton, 1985)

Gearing ratio = Long term liabilities/Capital employed

It measures the proportion of assets in the company that are sourced from debt. The higher the ratio the riskier it is for the company since repayment of interest and principle is mandatory unlike ordinary share dividends payout.

2008 Gearing ratio = 11,075M /31,483M= 0.35

2009 Gearing ratio = 11,273M/32,106M = 0.35

The company was constant when it came to the level of its gearing.

Return on capital employed = Profit/Total Assets – Current liabilities

It is a measure of the profitability of the company in relation of the company’s capital investments. The ratio went down in 2009 as shown below and the company should strive to raise it up.

2008 Return on capital employed = 2318M /24868M =0.09

2009 Return on capital employed = 1973M /26058M = 0.08

It becomes difficult for investors to compare the financial statements of companies in France and elsewhere in the world especially where the company uses French GAAP and not IFRS.

There are differences in the GAAP of different countries when it comes to treatment of certain items such as consolidation, intangible assets and equity items. To enable investors to have greater understanding of the financial statements, there has been efforts by different companies adopting the use of IFRS where they are allowed. The diffusion of the international accounting standards has great benefits (Nobes and Parker, 2010, pp. 60). IFRS makes things better however the national regulations and reporting traditions affect the way the comparability of the financial statements (Kvaal and Nobes, 2010). Scholars have noted that these traditions continue to affect financial reporting despite the adoption of the standards in many countries in the world (Nobes, 2006).

References

Deloitte. 2007. IFRS and US GAAP: A Pocket Comparison. Web.

Dilek, C & Husoy, K. 2007. ‘Corporate social responsibility practices and environmentally responsible behavior: The case of the United Nations Global Compact’, Journal of Business Ethics, vol. 76 no. 2, pp.163-76.

European Commission 1998. Examination of the Conformity between IAS 1 and The European Accounting Directives. Web.

Finch, N 2007, ‘Testing the Theory of Cultural Influence On International Accounting Practice’, Proceedings of the Academy of Accounting And Financial Studies, vol. 12 no. 1, pp. 27-30.

Kamath, R, Khaksari, S & Hylton, H 1985. ‘Management of excess cash: practices and developments’, Financial Management, vol. 14 no. 3, pp. 70-77.

Kvaal, E & Nobes C. W 2010. ‘International differences in IFRS policy choice: a research note’, Accounting and Business Research vol. 40 no. 2, pp.173-187.

Mihaela, H, Claudia, 0 & Lucian, B 2011. ‘Culture and National Competitiveness’, African Journal of Business Management, vol. 5 no. 8, pp. 3056-3062.

Nason, S 2008. ‘Structuring the Global Marketplace: The Impact of the United Nations Global Compact’, Journal of Macromarketing, vol. 28, pp. 418-425.

Nobes, C 2006. ‘The survival of international differences under IFRS: towards a research agenda’, Accounting and Business Research, vol. 36 no. 3, pp.233-245.

Nobes, C & Parker R 2010, Comparative International Accounting, Prentice Hall, United Kingdom.

PriceWaterHouseCoopers (2008). IFRS AND US GAAP Similarities and Differences. Web.

Vitell, S, Nwachukwu S & Barnes, H 1993. ‘The Effects of Culture on Ethical Decision-Making: An Application of Hofstede’s Typology’, Journal of Business Ethics, vol. 12, pp.753-760.

Wright, F. K 1978. ‘Minimizing the cost of liquidity’, The Australian Journal of Management, vol. 3 no. 2, pp. 203-22.