Performance

Liquidity

The working capital of the two companies is not adequate for their current operations considering the fact that their current ratios are below the recommended ratios of 2:1. It leaves a lot of room for liquidity. The current ratio of the Ladbrokes is 0.57 and in the years 2009 and 2010, it was 0.3 respectively. This means that the ratio is not excellent. Their current assets are 0.3 times lower than their liabilities, which provides little liquid assets to pay for the liabilities in case they are required by suppliers and creditors to pay at a certain time. The case applies to the William Hill Company; it has a ratio of 0.32 and 0.7 for years 2009 and 2010 respectively.

The liquidity ratio is extremely distressing at 0.3 and 0.70 because it is lower than the current liabilities. The company has more expenses than they have cash on hand. Even if some of it can be paid for at a later time or be treated as a deferral, ideally any business should have more cash at hand than what they actually need to prevent themselves from being cornered by creditors and even employees whose wages need to be paid on a regular basis. The target liquidity level is 2:1, which is very different from what the company’s cash on hand, which is right now at belo1:1. The companies are far from being liquid and are always in constant danger with the kind of cash reserves they have at hand (Collier, 2003).

Profitability

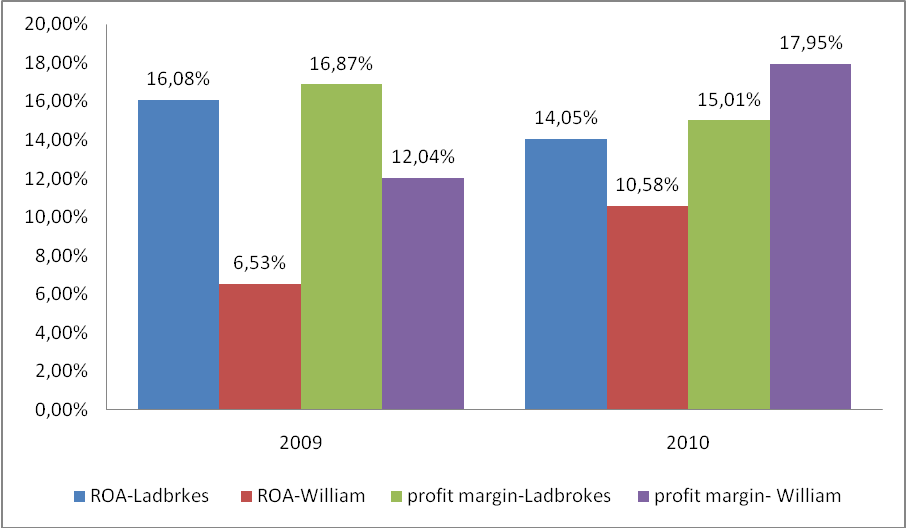

Return on assets is a key profitability ratio that measures the amount of profit made per pound of assets that they own. Return on assets gives an idea as to how efficient management is using its assets to generate earnings. Return on assets of Ladbrokes has decreased in 2010 as compared to the previous year due to an increase in total asset or decrease in profits, while the net income decreases to 15.01% from 16.87% and because of the decrease in net profit, ROA decreased. When looking at William Hill Plc, it seen that it increased from 6.53% to 10.58% this can be attibuted to the increase net profit from 12.04% to 17.95% for years 2009 to 2010. The following graph shows this ratios

The operating ratios tell us that the return actually exceeds to 57.53% which is explained by the contributions the company gets thus, creating a higher returns to assets that didn’t actually require anything to create this additional revenue in the form of a contribution for Ladbrokes and 22.93% for William.

Overall, if we are to consider the two companies financial condition, I recommend that the company does not add any loans or debts because it is already in a dire situation. It is not able to pay its current expenses and the only reason why it is still afloat is the generous donations it has received. It will be disastrous if the company suddenly experiences a drop in donations because their revenue level will not support its current expenses. Its operating margin is also very small at a mere 3% only, which indicates how hard it is for the company to create a profit from all of its operations. The company should either increase its prices or strive to have more sales or take both actions because it should have been bankrupt long ago if not for the donations.

Asset utilization

The two companies are indeed capital intensive because they have long-lived assets comprising 65% of their total asset value. This is to be expected because companies rely on heavy machinery and manufacturing plants to process their various products from raw agricultural products to finished processed food products. The variety of their machinery and plants are as varied as the food products they are selling to the public. All of these have unique processes, as well as unique machinery requirements, this is why the capital needs of Ladbroke are equally great.

The company simply had huge capital structure changes in 2010. There was huge disposal of business in 2010 that was not seen in 2009. There were also many obligations that were met by the company in 2010 which resulted in their increased debt servicing levels but overall, it is still well within the capacity of the company to indulge into.

The companies are also very clear in listing down their human resources as part of their asset base. The only things they have not listed are the values of brand names that contribute to their brand and sales growth. These are somewhat harder to evaluate but nevertheless, provide value for the company (Graham 2006). The disposal of Alcon’s pharmaceutical business yielded a lot of capital for Ladbroke they can use for other profitable venues. The combination of disposing of a huge business segment plus the addition of more debt allowed Ladbroke to weather the financial storm that has gripped the whole world when the US had a recession. Ladbroke has been able to get the capital it needs for investing in areas that are more profitable plus getting enough cash flow to use as a buffer if that sales drop. As it is, Ladbroke has been able to provide the best value for their shareholders while strengthening their market share through the weak economy.

One of the most revealing ratios however is the fixed asset turnover ratio, which indicates the type of capacity Ladbroke has. The difference is not even significant for a company of its size because they are just too big to place emphasis on the 2% difference. The asset turnover isn’t impressive compared to the financial services business where you can commonly see several hundred percent in returns because they don’t really have a fixed capital as part of their business model but for a capital intensive type of industry like food processing, Ladbroke is already very strong within their own category. The others within their industry have only 4-12% of turnover sometimes. Compared to Ladbroke, they already have a very impressive capability of using their capital assets. At the rate of 22%, it means that the company will roughly be able to double its size every five years. Since they are not a technology company with the potential to skyrocket through the charts, Ladbroke can be considered as very impressive for its category.

All in all, Ladbroke has been very strong and smart for freeing up capital on a slow growth area to use its faster income-generating venues for the company. It also allows them to concentrate on their core business, which is food manufacturing. The financial strength of the company is strong no matter what viewpoint you take. The whole organization and its subsidiaries were all fundamentally strong with clear business models and clear margins of financial safety. They have very wide margins of financial strength that allow them to absorb any negative or unexpected events such as a decrease in sales.

Although the industry is capital intensive, Ladbroke has created a lot of defensive barriers to entry in order to protect its market share. The depth of their research on most food processing businesses is already advanced. Their existing logistical distribution network worldwide is also very well established and refined. Their partnership with a host of other business entities cannot be enumerated within the financial statements, but they are a key for creating the best type of defense mechanism to protect their revenues. When it comes to investing and financing, Ladbroke’s capital structure is well utilized to its fullest potential with a conservative approach. No wonder their global reach is well-founded because of these fundamental strengths that have been put in place.

The two funding ratios tell us that the contribution of third-party entities comprises a significant portion of the company’s funds because it was approximately 71% of their total revenues in 2004. The debt ratio, on the other hand, presents a somewhat positive picture because the level of liabilities is approximately at 10 % of the assets only.

Capital structure choice

Capital structure is the combination of debt and equity used to finance a company. Debts can be in the form of bonds, which are similar to loans in the sense that they “promise certain payoffs” to those who would buy them (Kapil, 2011). These payoffs are usually in the form of interests. Equity, on the other hand, is similar to ownership, in the sense that the owners share whatever is left after obligations to bondholders have been met. In some companies, debt is lower than equity because the owners do not want to expose themselves to higher risks. Others choose to have high debts in order to finance ambitious projects. What a company decides on the debt-equity ratio will depend on factors like availability of funds and cash flow, cost of investments, and projected returns on investments. Those with a higher debt-to-equity ratio is often considered risky business because there is a possibility that short-term debts may not be paid using the company’s existing cash flow. Recommendations as to what suitable capital structure they should have will then be made after analyzing each brand.

Analyzing the debt and equity levels of both business firms, we can clearly see that Ladbrokes and William hill is the ones with less risk and a safer amount of debt at manageable levels. It is still far from being optimal or desirable, however. It is only to be expected that their leverage is very high at a 20% gearing ratio. The breakdown in terms of short and long-term liabilities indicates the bank is at least organizing its capital structure around long-term liabilities. Even though there is still a lot of improvements to be made, its advantage level is somewhat to be expected within their industry. William Hill Plc on the other hand has debt levels far better than Ladbroke because they are a retail company and they are not capable of handling such high debt levels for them to operate. Their current debt obligations stem more from their operation rather than from their long-term prospects. The current liabilities of William Hill Plc are mostly derived from the betting retails they are purchasing to hold. The economics that drives these two companies are vastly different, so we cannot logically compare their financial ratios easily. Suffice to say, they are not very good investors because of the high debt levels, no matter what industry they belong to or the type of business model they have. In the case of Ladbrokes though, their debt levels are somewhat reflective of their operations, which requires a lot of capital upfront because they are engaged in the betting deals.

The important consideration for Ladbrokes is how good they are in eliminating their debts at a reasonable pace (Wee 2001). The cash inflow from their clients should be faster and bigger than the cash they are throwing out to finance the projects they are engaged in to ensure the company is still liquid enough to meet its obligations and continue fuelling its growth. For Ladbrokes, the critical question is how they can maintain their operations while keeping long-term liabilities at a manageable level to allow them to profit from the time interval it takes to acquire shops.

These indicate whether the firm is managing its capital structure effectively. The debt Ratio appears to be growing although at a not higher rate. All operations of the organization are financed by debt and its growth increases the chances of insolvency. The following chart shows how the ratio performed;

This is a classic long-term risk ratio that aims at determining what proportion of the company’s capital structure is composed of equity. The ratio helps determine if funding for William hill is available, and the weight of the company with regard to debt or equity financing (Vasigh, Fleming, and Mackay, 2010). Based on the company’s financial data, it is observed that the company reported gearing of 90.04% and 74.40% in the period ending 2009 and 2009 respectively. This signifies that in 2009 for every 1 pound of stockholder equity the company has been able to leverage 90.04% pounds of debt finance. The decline in the figure is therefore positive as it signifies a reduction in the degree of debt.

The Ladbroke is financed by 24.51% debt compared to its equity in 2010 and -5.51% in 2009. It is a very strong position considering that the amount of debt is very small regarding its total asset value. It shows that the company is conservative in its dealings, as well as risk appetite. The ratio is even more revealing of the nature of the company because the ratio is very high for a company of its size. It means that the company is able to meet its financial obligations more than what is required (Graham 2004). Although Ladbrokes is already a very big company, they are not risking their existence with a huge debt load. They are more than capable of paying the debt and the amount they take on is simply for convenience.

It is possible to have an optimum capital structure that would maximize the firm’s stock price, and they have to make a trade-off between risk and return. When a firm’s long-term financing results from debt, it would raise the risk borne by stockholders (Bragg, 2010). Conversely, using more debt would increase the expected return on equity by raising the firm’s financial availability. However, this is influenced by the firm’s flexibility in the ability to raise funds even under adverse market conditions. The firm should retain sufficient financial resources to enable it to take advantage of available opportunities, and to overcome unexpected financial obligations (Moles, Parrino and Kidwell 2011). A firm should have enough financial flexibility to be able to obtain finance for unexpected opportunities in the market. Since it could be difficult to solicit investor funding and get it while the opportunity is still attractive, the firm’s financial flexibility should enable it to acquire such financing promptly. Similarly, the firm should be able to comfortably meet unexpected financial obligations that could be more costly with time (Moles, Parrino, & Kidwell 2011).

A stable supply of capital would promote stable operations in the firm (Brealey, Myers and Allen, 2008). Capital availability also determines a firm’s success and long-term survival, especially during hard economic times. Since creditors and investors prefer to deal with a firm that has a stable equity capital, the financial flexibility of a firm is a major consideration for the firm’s capital structure. A firm should have less debt capital on its balance sheet for future accessibility to finances (Brealey, Myers and Allen, 2008). This would enable it to meet its long-term financial obligations and to benefit from unexpected business opportunities in the market.

The use of debt financing as a way of lowering the effective cost of debt, however, is not always effective. If most of a firm’s income were already exempted from taxation due to interest tax shields, interests on outstanding debt or tax loss carry-forwards, it would have a low tax rate (Brealey, Myers and Allen, 2008). Additional debt finance would fail to have a profound impact on the firm, and would not be as advantageous as it would be if the firm had a higher effective tax rate.

Debt financing affects a firm’s earnings since the interest expense associated with it reduces the reported value of net income (Moles, Parrino and Kidwell, 2011). For managers who are concerned with earnings per share, financing projects using debt instead of equity would increase the reported value of earnings per share, and this could influence the actual prices of the firm’s shares. Since the tax position of the firm would determine its use of debt financing, the position would thus determine the firm’s earnings per share.

The choice of a firm’s capital structure is influenced by the firm’s business risk (Alvarez and Fridson, 2011.). This is the risk related to the firm’s operating activities since they determine the impacts of economic fluctuations on the business. The aim of a firm that is choosing a capital structure is to reduce its overall risk exposure to controllable limits. Managers choose a capital structure that enables the firm to reasonably deal with market fluctuations without high possibilities of loss (Kapil, 2011).

Business risk is the variation in a firm’s income determined by the proportion of fixed costs and varying demand for the firm’s products (Taparia, 2004). A firm’s activities determine its ability to cope with different market conditions without a profound decline in profitability. Investors tend to prefer stocks with a low business risk during times of economic hardships and turn to high-risk-high-return investments during favorable economies (Maguire, 2006). As such, choosing a capital structure that can enable the firm to respond to such variations in the economy is of utmost importance.

A firm’s financial risk also influences the firm’s capital structure. The financial risk indicates the firm’s financial leverage and it is related to fluctuations in shareholder earnings (Kapil, 2011). A firm’s financial risk is the balance between debt and equity in the firm’s capital structure, and it poses the risk of not being able to cover fixed interest charges during difficult economies. Additionally, financial risk determines the ability of a firm to clear its debts in case of liquidation (Thompson, 2003).

A firm strives to keep the business risk and financial risk at a low level, thus reducing its overall risks and costs. Similarly, a low business risk increases the overall value of the firm and improves its relations with investors. Business risk is thus a practical consideration made by the management while choosing a firm’s capital structure. The long-term financing option adopted should enable the firm to cope with fluctuations in the market in a way that does not increase its risks, since a high business risk leads to a low optimal debt ratio (Weetman, 2006).

Stock price fair value, efficient market hypothesis net present value

The price of the stock on the 5th of November is not fair value for both companies. The price of a stock will depend on many factors including dividends that are paid to stockholders and the type of management the company has. The traders will always look for this information before making a purchase or a sell. When information is reflected in share prices, the market is said to be efficient. Therefore, providing the greatest acknowledged strength of the buying- and-holding strategy, it is theorized that by fair valuing every security at all times, no trade would take place. It is posited that securities should never be sold unless one needs the money accruing from them. Buy-and-hold has also been advocated entirely on the basis of costs. In all transactions, costs are incurred. In offer/bid spread and brokerage, for instance, costs add to liabilities. Buy-and-hold, nevertheless, involves the fewest such transactions for any similar amount expended in the market when all other factors in such investment are kept equal.

Proponents of buy-and-hold may therefore be considered long-term market timers, Warren Buffett is an example. Support for the strategy, from the reviews, seems to precede the recent downturn. The support suggests that, on its own, or in a combination with other strategies, buy-and-hold is quite viable. Alternatively, and in the wake of the downturn, it is suggested that the strategy is conditionally viable. After the big market slump seen in mid-2008 and toward 2009, however, there have been criticisms directed at the buy-and-hold strategy. Many consider the strategy outdated and so would wish to see the hype about it reduced or dropped altogether. In other quarters, its value in a continuously speculative market is considered to be unenthusiastic. Some, nevertheless, have gone as far as pronouncing it dead; that it cannot be followed by sure success anymore.

In regard, there have been ardent drives towards rethinking how portfolios should be planned and in the fear that the buy and hold strategy never worked for investors in the wake of the downturn. My opinion is that a better investment strategy would involve investing some money during the dips and rebalancing the investment by periodically getting some of the assets back in order. This would be a mix of buy and hold incisive market timing and diversification. As investment periods lengthen/as an investor gets older, it is necessary to put more into safer assets such as cash and bonds and less into equities. Further, diversifying within and among assets also helps to soften out volatility levels in downturns. Just because the word “sell” does not appear in the word “buy and hold” does not mean an investor cannot reposition his/her portfolio by changing things around.

The rise and growth of the efficient market theory were complicated by the development of behavioral finance. The efficient market theory slowly grows less popular, which, in fact, has not made a difference in the options of investors who either with the choice of an efficient market model or a behavioral-based financial investment option, are limited in their choices and access to information. To highlight further, the Efficient Market Theory is composed of mathematical models that allow investors to make a decision based on the information provided. This consequently means that an investor is unable to make effective decisions without the help of a market professional who has access to the information inside.

The problem of making sound investment choices for a foreign investor is further underlined when it is taken into account that behavioral finance has weakened the effectiveness of the efficient market. Because of the focus on studying the psychology of the investor or the customer leading hence to increased chances of ineffective investment choices the investor is at risk of considering the importance of market professionals’ consultancy due to the current financial and stock market’s structure. Investors are after all not as predictable as the current behavioral theories attempted to approach the foreign individual through. The myth that the market adhered to absolute laws caused at times more harm than it gained people good and with the knowledge that compensations are limited to extremely narrowed cases whose further restriction by the ineffective resolution procedures is even more aggravated (Woelfel, 1994).

The monetary standing of every business organization also changes along with the fluctuations within the global market. Hence, as a result, not one business organization is entitled to completely receive high-end profit at the end of each year. This is the reason why the administrators of each business entity are empowered to utilize several forecasting models of calculations that are assured to have an impact on how they balance the release of their funds in accordance with the entry of monetary assets into the business. This is in relation to the capability of the entire asset resources of the business to be completely flexible with the market fluctuations existing within the global trade. In a short definition of the Black Scholes Model, it could be sensed that the close relationship of the dividend and the stock returns considered within the system suggests the efficiency of capital and assets control.

To make the model more efficient, modern computer programmers designed several software that responds to this particular function of the financial measurement considered herein. Volatility affects the prices of stock options directly. This means that the dividends released by the business entity could be directly affected by the historical volatility of the asset. True, as based on the function of the exponential power within the equation, this model offers a better sense for controlling the outside environment of the financial resource of the business and how this management should affect the outward and inward bound of shallow in the organization.

Net Present Value

The intrinsic value of a share presents the value of all cash flows expected to be received during the holding period. The stock price of the company is also very close to its actual intrinsic value (The present value of future dividends) (Bruner, 1998). Further, the stock and the bond prices are measured to be more volatile than as compared to advocates of rational efficient market theory could have predicted. They literally have bigger assets than the calculated present value from the free cash flow method. It is because of the retailing aspect that makes them capital intensive. In short, they are big and strong but unfortunately, they are also slow in terms of investment growth rate. To provide a rough picture, they are 23% in terms of the actual value they have for investors if we are to compare their calculated present value from the current operating asset size they have. It is not small but it is not big either. They fall in the category of average. They are very profitable when compared to the financial status that banks were in at the height of the recent depression but they are so far behind from the impressive gains that technological companies usually have.

Reference List

Alvarez, F. & Fridson, M. 2011. Financial Statement Analysis: A Practitioner’s Guide. New York: John Wiley & Sons, Inc.

Bragg, S., 2010. Wiley Revenue Recognition: Rules and Scenarios. New York: John Wiley and Sons.

Brealey, R. A., Myers, S. C., & Allen, F., 2008. Principles of corporate finance. NEW York: McGraw-Hill.

Bruner, R. F. 1998. Case Studies in Finance: Managing for Corporate Value Creation. New York: Irwin McGraw-Hill.

Collier, P., 2003. Accounting for Managers: Interpreting Accounting Information for Decision-Making. New York: John Wiley and Sons.

Graham, B., 2004. Securities Analysis. New York: McGraw Hill

Graham, B. 2006. The Intelligent Investor. New York: McGraw Hill

Kapil, S., 2011. Financial Management, New Delhi: Pearson Education India.

Maguire, M., 2006. Financial Statement Analysis. GRIN Verlag: Publisher, Amsterdam.

Moles, P., Parrino, R. & Kidwell, D., 2011. Fundamentals of Corporate Finance. San Francinsco: John Wiley and Sons.

Taparia, J., 2004. Understanding Financial Statements: a journalist’s guide. Illinois: Marion Street Press Inc.

Thompson, L. 2003. Improving accounting efficiency. AllBusiness. Web.

Vasigh, B., Fleming, K. & Liam Mackay, L., 2010. Foundations of Airline Finance: Methodology and Practice. Surrey: Ashgate Publishing Limited, 2010. Print.

Wee, C. H., 2001. Sun Tzu: Art of War and Management. Kuala rumba: Penguin Books

Weetman, P., 2006. Financial Accounting: an Introduction. New York: Financial Times Prentice Hall.

Woelfel, C., 1994. Financial statement analysis: the investor’s self-study guide to interpreting and analyzing financial statements. USA: McGraw-Hill Publishers.