Introduction

All companies worldwide have for the past one and half years experienced the consequences of the COVID-19. Company managers have done their best to control a slew of intertwined problems, which constitutes ensuring the safety of their staff and clients, reorienting activities, cash and liquidity bolstering, and navigating federal support services that are nuanced. As COVID-19 adds to the economic loss and uncertainty, maintaining a company’s long-term viability thorough understanding of shifting market dynamics, and government policy has been in the limelight. This report evaluates the prospective future financial budgeting strategies for the BP PLC Company concerning the lately experienced impact of COVID-19 through financial analysis of its past performance and overviews economic trends in the global market regarding the petroleum industry.

Company’s Background Information

BP PLC is an Oil and Gas British multinational company that functions in seventy countries across the globe. The company’s upstream operations, in the third quarter of 2019, a total of 3.6 million barrels of oil equivalents were extracted per day(Graham et al., 2020, p.340). Oil and gas trading and distribution, as well as the processing and sale of petrochemicals, lubricants, and fuels, are all part of the company’s downstream activities. According to Graham et al. (2020), as at July 2020, BP had capitalization in the market of $77.4 billion. In the oil, energy, and gas industries around the world, BP PLC counts itself among the major player. According to Juliani and Rahadi (2020), market value analyzed as at the 2018 evaluation, BP was the sixth-largest gas and oil firm and posted sales of about 278.4 billion dollars in 2019, putting it in the top ten of the entire industry with more than 70,100 employees across the globe making it one of the most successful oil firms in the industry.

Impacts of COVID 19 to Company

The ongoing COVID-19 pandemic has caused business-related challenges in most departments. Notably, the gas and global oil industry have probably been the major affected industry. Forced shutdown or slow physical operations of most of the companies has been the norm and has subsequently involved production in both downstream and upstream markets (Graham et al., 2020). The price collapse of crude oil in a short period of time was perhaps the most significant effect of COVID-19. On January 1, 2020, based on the New York Stock Exchange, a barrel of crude oil was exchanged for $67.05, and by March 15, 2020, a barrel’s price had plummeted to $30.00. With regard, the company has been severely impaired, and its capitalization in the market as of March 15 2020, was reduced by half.

Evaluation of Financial Performance of the Company

In a broad sense, financial performance refers to how well financial goals are being met or have been met, and it is a significant part of financial risk management. It is a method of valuing a company’s policies and activities in terms of money. It’s used to evaluate the overall financial health of a company over time and to compare similar businesses in the same market, as well as industries and sectors as a whole. Financial statements are used in financial reporting for financial management (Atrill and McLaney, 2015). A financial statement is a reasonable and coherent set of data structured according to accounting procedures. Its aim is to convey an understanding of some of a business’s financial aspects. It can report a series of events during a specific time span, as in a balance sheet, or it can show a condition over a period of time, as shown in income statement.

BP PLC profitability ratios

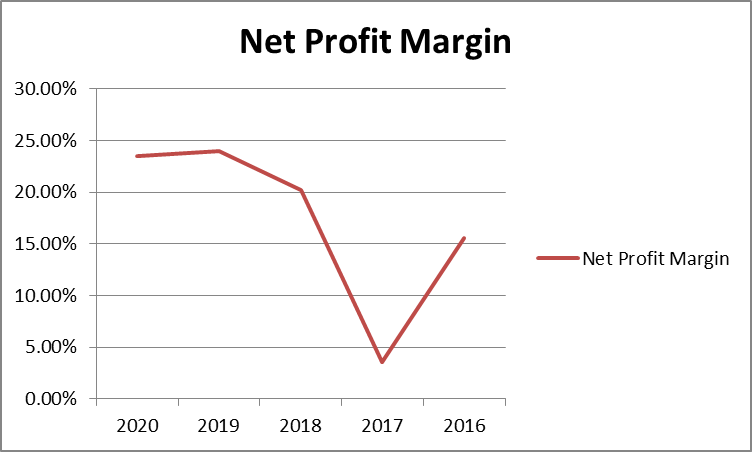

Profitability analysis enables businesses to maximize profits and limit losses. As a result, businesses should maximize the resources available to them to continue expanding in a highly diverse, competitive, and vibrant (Watson and Head, 2013). Profitability analysis aids companies in identifying growth opportunities, fast/slow-moving stock products, industry patterns, and other factors that give decision-makers a clearer view of the enterprise as a whole. In profitability gouging, the profit margin is found to be perfect for determining the Company’s business health over the years, as evaluated in the past five years (see Appendix A). NBP PLC, Net Profit Margin Analysis is described as the ratio of net income to sales and is a measure of profitability basically known as the Net Profit Margin. From 2018 to 2019, BP PLC’s net profit margin ratio increased, but from 2019 to 2020, it marginally declined (see Appendix A).

BP PLC Liquidity Ratios

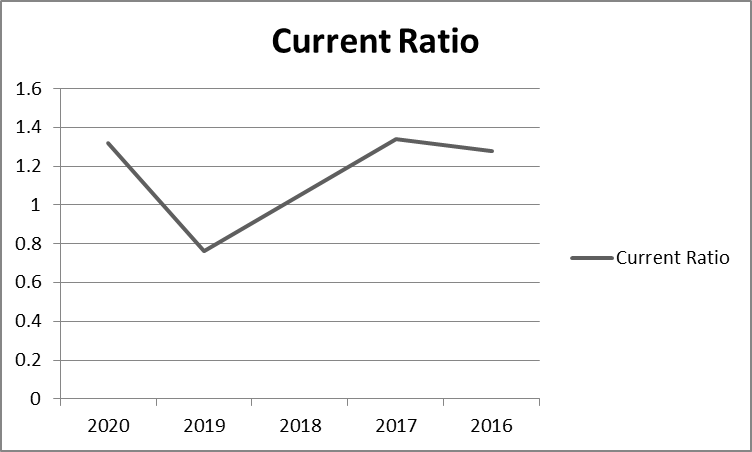

The company uses the concept of liquidity ratio to assess the financial obligation with regard to debt. According to Wilson and Head (2013), a financial metric that aids in assessing the ability of the debtors to repay the present debt obligations with no other financial support is the liquidity ratio. For BP PLC Company to determine its financial performance critically, it must ensure that it is eligible for financial loans from financiers; it must evaluate its capability to meet the short-term obligations using the liquidity ratios (Bamber and Parry, 2014). Therefore, liquidity is described as the ability to convert assets into cash at a low cost and with ease.

This critique is normally carried out either externally or internally. Internal liquidity ratio analysis, for example, necessitates the use of different accounting periods reported using similar accounting methods. By comparing past periods to current operations, analysts can keep track of market shifts. In general, a higher liquidity ratio indicates that a firm is more liquid and has good debt coverage. To measure a company’s liquidity, three-star evaluations are necessary, as indicated in Appendix B. Current Ratio is the liquidity ratio given by the division of the current assets by current liabilities. The current BP PLC ratio declined from the year 2018 to the year 2019 however, increased from the year 2019 to the year 2020, surpassing 2018.

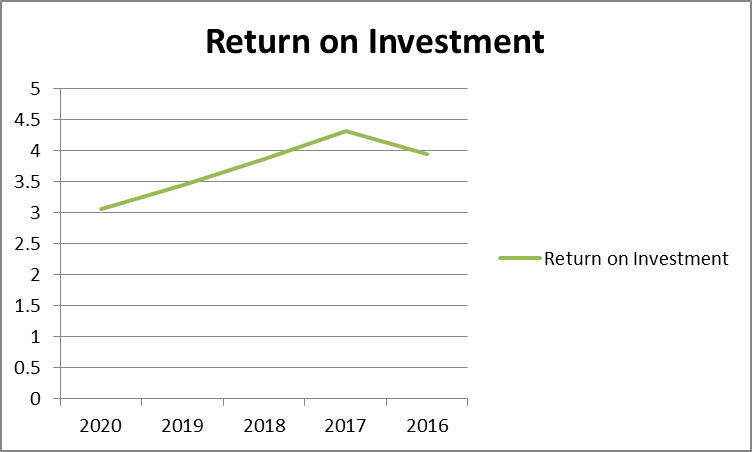

Investment Ratios/Long-Term Activity Ratio

The Return determines the productivity of a company’s investments on investment ratio analysis. Simply put, it indicates whether or not an investment would be successful. To assess management’s success in growing a business these calculations can be used. When comparing similar companies, a lower ratio may indicate poor executive investment decisions. For BP PLC to determine the amount accrued upon investment, the best ratio to check on is the Return on investment shown in the diagram below for the past five years as illustrated in Appendix C. Return on Investment is described as the total revenue divided by net fixed assets is the expenditure ratio. The investment level of BP PLC declined from 2018 to 2019 and from 2019 to 2020.

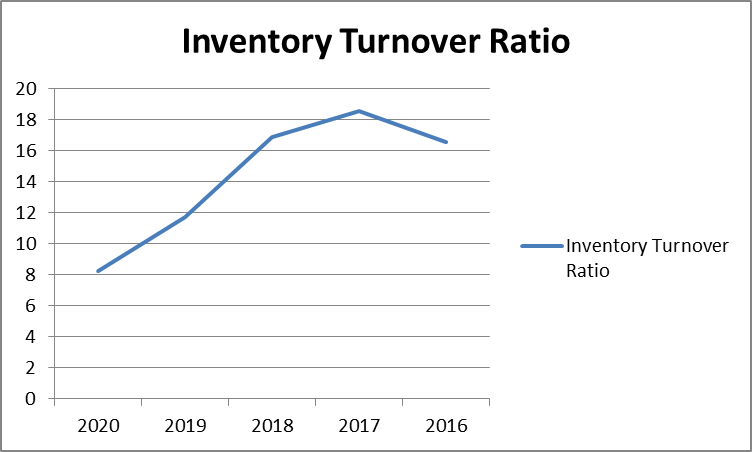

Efficiency Ratios

They are the ratios used to evaluate a company’s ability to produce revenue by effectively using its resources, such as capital and assets. The ratios are used to equate expenses to earnings, indicating how much income or benefit a company can generate from the money it spends to operate its operations (Juliani et al., 2020). The more efficiently a company is managed and controlled, the more likely it is to generate maximum long-term income for its shareholders and owners. Similar productivity ratios focus on different areas of operations, such as a company’s asset management, cash flow, and inventory management. Several performance ratios can be used by financial analysts to get a comprehensive image of a company’s overall operating efficiency. The inventory turnover ratio would be the best financial ratio to gorge the BP PLC company’s efficiency, as shown in Appendix B. For instance,

Limitations of Using Financial Ratios for Assessing Financial Performance

Ratio analysis, like any other financial analysis methodology, has its drawbacks. It is essential to understand these limitations to avoid drawing incorrect conclusions. Below is the ratio analysis with regards to the evaluation of BP’s financial performance.

- Changes in accounting practices: The financial statement is affected when the company’s accounting process and practices changes. The key financial metrics used for analyzing ratios changes and the financial results after the adjustments are reported as they vary from the financial results reported before the change. The analyst, therefore, has a duty to keep up with changes in accounting policy. The corrections are usually described in the section of the financial statements called notes to the financial statements.

- Historical Data: The conclusions of the report are focused on actual historical documents that the organization has made public. As a result, ratio calculation metrics aren’t always accurate predictors of future business results.

- Inflationary effects: Financial reports are published on a daily basis, with several gaps in between. The valid values are not stated in the financial statements if between the periods there had been inflation. As a result, once inflation is taken into account, the figures can no longer be compared over time periods.

Capital Budgeting Approach

This entails choosing projects that immensely increase the value of the company’s Capital budgeting phase can include anything from land acquisition to fixed asset purchases such as machinery or new truck. Normally the corporations are expected and encouraged to pursue ventures that will boost profitability and thereby increasing the wealth of shareholders (Morales Burgos, Kittler and Walsh, 2020). Other factors unique to the business and the project affect the return rate considered reasonable or unacceptable (Watson and Head, 2013). The importance of capital budgeting is that it establishes quantity and transparency. Any company that invests in a project without thoroughly understanding the costs and benefits would be considered rash by its shareholders or owners. Excluding non-profit organizations, all corporations operate to increase wealth. This model is a measurable way for companies to assess any investment project’s long-term economic and financial viability. A decision done with the capital budgeting model entails both expenditure and financial commitment.

Zero-based Budgeting Approach

Financial planning requires that first growing companies to perform their budgeting for the foreseeable years. Because of the present COVID-19 pandemic and the mass vaccination, zero-based budgeting approach (ZBB) is the most appropriate financial planning method because it allows managers to execute their financial planning from scratch. In this approach, BP PLC executives must justify their expenses because of the lack of acuity of what the pandemic can cause in terms of business losses and reduced values at the stock exchange securities. As such, the $50 million budget should only be financially planned to such expenditures that are not recognized as absolutely important to the firm. It is an approach considered as bottom-up budgeting (Clark, Menifield and Stewart, 2018). Therefore, because of losses in gas and oil since the emergence of COVID-19, BP PLC must only use ZBB and wait for the new normal to commence.

When BP PLC is faced with a decision evaluation using a capital budgeting model and ZBB, the first main task is to decide the profitable probability of the project. According to Watson and Head (2013), for a project selection, the major approaches are the payback period (PB), internal rate of Return (IRR), and net present value (NPV). These models are applied in cases where a company wants to comprehend with of the payback periods best suit them depending on their financial abilities.

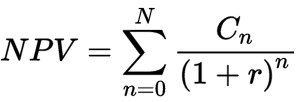

Internal Rate of Return

The discount rate that reduces the net present value of all potential cash flows from a project to zero is known as the Return’s internal rate (IRR). It is often used to compare and choose the best project, with an IRR more significant than the minimum reasonable Return (hurdle rate) being chosen. Formula-

Table 1: The Internal Rate of Return Vs. Net Present Value.

The IRR approach, Projects are boiled down to a single number that will be used by management to decide if they are financially viable. The project will be followed if the IRR exceeds the company’s required Return rate or demonstrates a net profit over time (Watson and Head, 2013). However, if the return rate falls below that threshold or if a long-term loss is predicted, a business can decide to object to a project. The IRR might not be suitable for capital budgeting at BP PLC, necessitating an NPV review.

Discounting Rate= 10%

Table 2: The number of years for completion of the project is ten years.

Where NPV- Present Net Value

Rt- Net cash flow at the time

I-Discounting rate

T-time

In the case of BP PLC, the company’s potential cash flows is forecasted by the NPV of a project. The capital costs and risk cost of capital for the project are then discounted into present value amounts using a discount rate that reflects the project’s capital costs and risk. The project’s anticipated positive cash flows are then reduced to a single present value figure (Watson and Head, 2013). This sum is subtracted from the total investment amount required. The difference between a project’s expenses and earnings is its net present value. Since it includes such assumptions as the discount rate and the probability of receiving the cash payout, the NPV approach is inherently challenging. As such, the effectiveness of using the Net present Value to evaluate BP PLC’s budgeting is perpetuated because of the emergence of COVID-19. Therefore, the company should build on better projects of 10% discounting rate for effective return within the next ten years.

Thunder Horse

The concept of the Thunder Horse scheme is used for this analysis. The project aims to increase the capacity of the current Thunder Horse sector, which is the Gulf of Mexico’s major oil ground. In the near future, this plan will complement the two novel manufacture units approximately two kilometers from the present Thunder Horse unit, as well as two new production wells. As part of the overall construction, eight mines will ultimately be drilled. To ensure that the company does not lose its assets and make substantial profits, the concept of BP PLC financial analysis will be applied.

The Rationale for Choosing the Target Project

At its height, the project is projected to add 50,000 gross profits in output to the current Thunder Horse podium, with principal oil production in 2025. The newest development at Thunder Horse is a case in point of how Mexico is at the forefront in managing advantaged oil development for BP, unraveling noteworthy costs and securely increasing a high-profit margin market. As such, the new project has demonstrated possible sustained growth and momentum in a market that will continue to play a central role in BP’s international portfolio for foreseeable years.

The Gain to the Company

In the immediate future, this massive upstream scheme, as illustrated, will see an addition of two manufacturing plants with two massive wells drilled close to the current location of BP’S station in the Gulf of Mexico.

Financial Cost of the Project and Sources of Financing the Project

Overdrafts are convenient short-term financing options that require repayment in less than a year. Interest is paid only when the facility is used, and interest payments are tax-deductible. They can be organized quickly, and the sum lent can be changed at any time.

Loans have higher interest rates and are less flexible since payments must be made for a pre-determined sum and at a pre-determined period. Loans may be paid back in installments or at the end of the term. Interest is, therefore, tax-free, and the loan’s return could be greater than the interest payments. The Internal Rate of Return can be used to equate the cost of borrowing money to the return of the ventured project.

Risks in the Project

In order to take advantage of the US Private Securities Litigation Reform Act of 1995, BP issued a statement about BP’s Thunder Horse production platform and sector. In this case, the planned production levels and existence, as well as BP’s plans for potential Gulf of Mexico projects was to be initiated. Actual outcomes can vary from what is stated in such statements. The Gulf Coast states economic prospects were bleak, as the spill damaged many of the businesses that people relied on. At the height of the leakage, more than a third of federal gulf waters were locked to fishing due to pollution concerns.

Conclusion

In conclusion, at this critical moment when the world is dealing with the effects of COVID-19, BP and the rest of the oil sector are dealing with the effects of sharp drops in commodity prices and stock markets. Such uncertainty is nothing new for BP; the company is well-versed in responding to external challenges. With the evaluation of the past five years’ past performances, the company in 2020 faced a significant challenge in operations. It was transforming from the confusion caused by COVID 19 to the whole Oil and Gas industry. With capital budgeting, the company can evaluate the best method of investing its funds on the most appropriate project with an excellent return rate after the required time. The company’s projects for the next subsequent years should be effectively evaluated using the Net Present Value analysis.

Reference List

Atrill, P., and McLaney, E. (2015) Accounting and finance for non-specialists. 9th edn. London: Pearson.

Bamber, M., and Parry, S. (2014) Accounting & Finance for Managers. London: KoganPage.

Morales Burgos, J. A., Kittler, M. and Walsh, M. (2020) ‘Bounded rationality, capital budgeting decisions and small business’, Qualitative Research in Accounting & Management, 17(2), pp. 293-318.

Clark, C., Menifield, C. E. and Stewart, L. M. (2018) ‘Policy diffusion and performance-based budgeting’, International Journal of Public Administration, 41(7), pp. 528-534.

Graham, P. J. and Sathye, M. (2020) ‘The relationship between national culture, capital budgeting systems and firm financial performance: evidence from Australia and Indonesia’, International Journal of Management Practice, 13(6), pp. 650-673.

Sarwary, Z. (2020) ‘Strategy and capital budgeting techniques: the moderating role of entrepreneurial structure’, International Journal of Managerial and Financial Accounting, 12(1), pp. 48-70.

Juliani, M. and Rahadi, R. A. (2020) ‘Improving financial performance using capital budgeting method towards cleaner eyewear product: a case study of Nasho’, Malaysian Journal of Social Sciences and Humanities (MJSSH), 5(6), pp. 128-135.

Watson, D., and Head, A. (2013) Corporate Finance. Harlow: Pearson.

Appendix A

Appendix B

Appendix C

Appendix D