Introduction

The airline industry can broadly be split into two markets: passenger and cargo with sub-markets. The marketplace for air cargo services is made up of companies that sell aviation services and employ aircraft, including jets and helicopters, to move goods. The air cargo market comprises both scheduled and unscheduled air operators’ companies but excludes air courier services and picturesque air travel (O’Connell, 2018). This information is provided for a basic understanding of the difference between the two markets because the main focus will be on the passenger market.

Airlines that specialize in carrying people are called passenger airlines. The majority of passenger airlines run a fleet of passenger planes that are either wholly owned by the airline or rented from businesses that sell and lease commercial planes. Passenger airlines can function regionally across shorter, non-intercontinental routes or as mainlines, with flights managed by the airline’s central operations unit (Castiglioni, Gallego, & Galán, 2018). Passenger airlines may also be low-cost providers of essential services at lower costs. These charter airlines fly outside of regular schedule windows or with big airlines that generate much money in annual revenue. This paper was written with the intent to study how the passenger side of the airline business has performed over the past 20 years, using statistical and strategic data.

Passenger Market Performance in the Last 20 Years

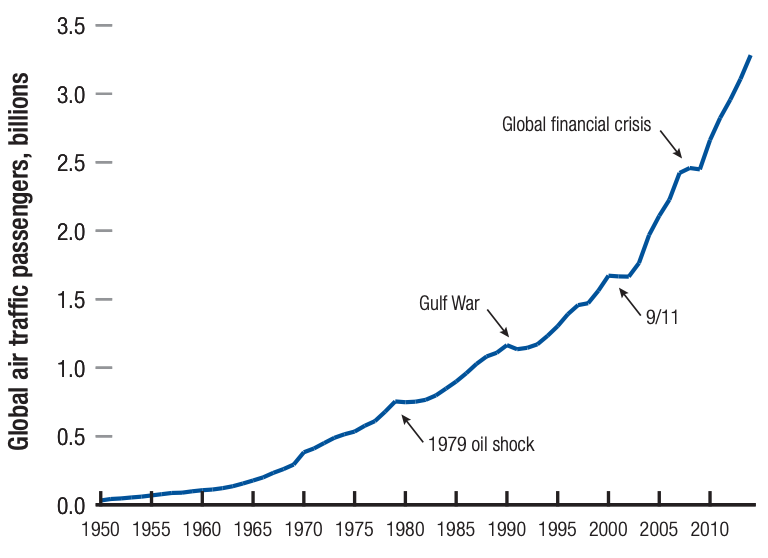

Unexpected shocks will undoubtedly affect how much air travel there will be in the future. Even though it is impossible to predict the exact nature and timescale of these shocks, examining how the sector has responded to past shocks can better determine how it will likely fare in the face of potential shocks. The enormous decreases in the actual cost of flying that have been observed throughout time play a role in why global air traffic has proven to be so durable.

Following the merged 2000–2001 shock of the dotcom crash and 9/11, as well as the startle of international economic meltdown in 2008, the comparative drops in passenger numbers were the greatest; however, in both instances, transportation had brought back to its trend standard within four years. Moreover, in 2008, many airlines ceased operations, citing high oil prices as the primary cause, and mention these airlines that went bankrupt/shut down. Global air passenger numbers have been increasing, somewhat inconsistent with the overall trend since recovering from the most recent shock (Bouwer, Saxon & Wittkamp, 2021). It should not be assumed that adaptability will always be automatic, even though the industry has traditionally been able to adapt its operational and financial models to new problems and outside shocks. After the crisis of 2008, the figures rose continuously until 2020 and the COVID epidemic.

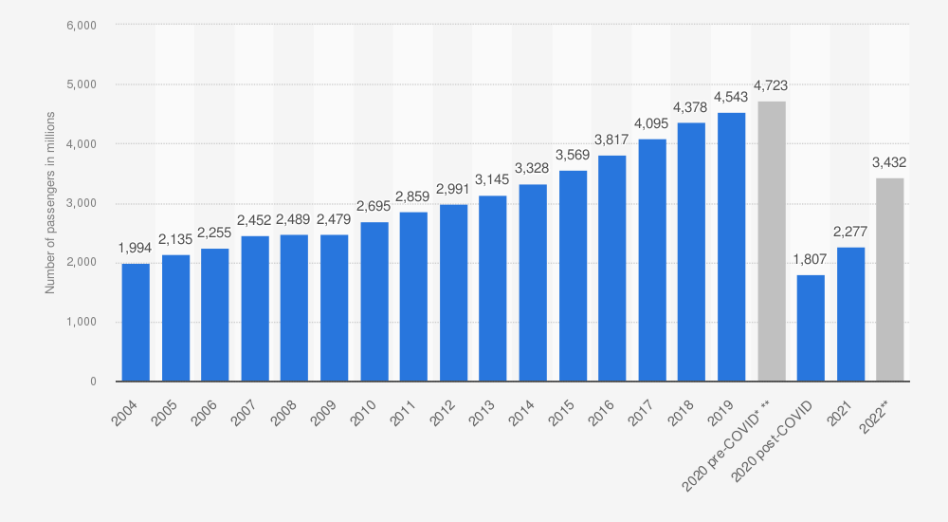

The term “scheduled passengers” describes the number of travelers who have made reservations with a commercial plane. Travelers on charter flights, in which a private organization rents out a whole plane, are exempted. Due to the coronavirus pandemic, the world’s airlines are expected to have boarded just over 2.2 billion commuters on scheduled flights in 2021 (Statista, 2022a). In comparison to 2019, this represents a 50% decline in global air passenger traffic. In all but one of the past ten years, the number of planned passengers served by the world’s airlines has climbed (Statista, 2022a). With one-third of the worldwide total, the Asia Pacific state had the highest percentage of airline passenger numbers in 2019 (Statista, 2022a). The busiest air routes are also found in this area.

The continued increase in air travel throughout the world is typically attributed to three key factors. The first is the rise of low-cost carriers, whose market share has nearly doubled over the past 15 years (Statista, 2022a). Second is the trend in the global working class, especially in China. These two changes have expanded the number of consumers who can afford to fly. Finally, the Asia Pacific area is leading the development in airport infrastructure expenditure, which has raised the world’s maximum capacity.

The travel sector has been significantly impacted by the coronavirus outbreak. Nearly all countries have issued orders for their borders to be closed and for airlines to cease operations. Most tour operators and travel companies are witnessing a severe fall in income. Airlines being compelled to cancel flights has a knock-on impact that is bad for hotels and restaurants as well (Czerny, Fu, Lei & Oum, 2021). For the travel, tourist, hotel, hospitality, and airline businesses, this translates to a considerable loss of income. Some travel businesses are fighting to stay open, but they are forced to wait it out.

Low-Cost Carriers’ Worldwide Market

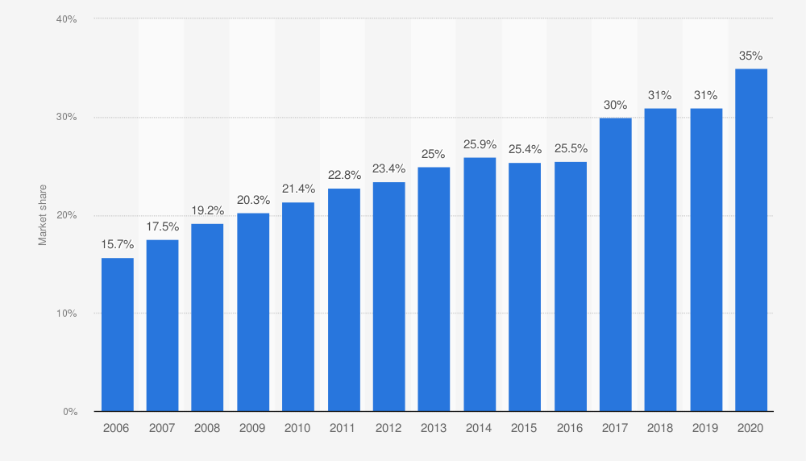

In order to offer passengers cheaper tickets, low-cost carriers generally rely on two different mechanisms than full-service carriers. Over the past ten years or so, low-cost airlines have significantly increased their market share in the global air travel industry; in 2020, they accounted for 35% of the world’s total seat capacity (Statista, 2022b). The first is to tack on extra expenses for items that full-service companies often offer, such as checked baggage and onboard meals and drinks. Second, low-cost flights frequently run out of auxiliary airports, which are typically less expensive for airlines to utilize.

Airline Passenger Strategies for Market Growth

With the urgent stated objective of cost-cutting to lower cash burn and strengthen their liquidity, airlines have switched into dire straights. Airlines, municipalities, and labour unions are at odds over how to satisfy investors, secure financial support, and safeguard livelihoods (Bieger & Agosti, 2017). Foreign travel, which depends on the lack of rare epidemics to maintain transit corridors, will recover more slowly than domestic air travel. Furthermore, a re-segmentation of the air travel markets is probably attributable to the drop in household expenditure brought on by the current economic climate.

Mergers

Mergers in the airline sector take place in response to shifts in the sector’s volatile economic environment. Due to the progressive deregulation of global markets, international aviation has undergone a significant transformation. Mergers are regarded as an adequate reaction to deregulation. Historically, the aviation sector has had poor profit margins and, therefore, is highly susceptible to the world economy (Khezrimotlagh, Kaffash & Zhu, 2022). The overlapping non-stop routes and interconnecting routes are particularly vulnerable to anti-competitive impacts from the merger of two overlapping networks.

The airline sector has been drastically transformed during the last several decades. American Airlines and Trans World Airlines (TWA) agreed to an agreement in January 2001 for the complete acquisition of TWA (Hsu & Flouris, 2017). Additionally, a contract to start the full acquisition of US Airways was part of this accord. TWA had its headquarters in the Midwest and established a distinctive hub at JFK Airport in New York City. Before being bought by American Airlines, the airline had three bankruptcy. The TWA brand was dropped from airports and flight listings after the sale was finalized in December 2001, and the logo was taken out over a two-year period (Hsu & Flouris, 2017). The TWA Hotel at JFK Airport, which was constructed near the airline’s original New York City hub, is where the heritage of the company, nevertheless, continues.

Mergers Acquisition

An airline must make a substantial investment before it can purchase an aircraft. Airlines have a variety of procurement options at their disposal, including direct purchase from manufacturers, capital or finance leasing, and operations leasing. Since the cost of the fleet is one of the airline’s most significant expenses, aside from fuel, the choice of these aircraft acquisition strategies will affect how financially successful the airline is (Naumovich, 2018). Airlines must thus select the most effective means of acquiring aircraft in order to reduce unit costs and maximize revenue.

The ideal fractional ownership option is for someone who travels between 50 and 100 hours annually. They exchange a portion of their ownership for shares in an aircraft. Notably, the fraction software runs the aircraft and provides individuals with improved access as needed (Yan, Fu, Oum & Wang, 2019). The fractional program typically expires after three to five years. In wet leasing, the lessor takes care of the crew, servicing, and insurance for the aircraft. As a result, they cover the costs of operating times, fuel, tariffs, taxes, airport fees, and other expenses. Wet leases often last up to two years. Those who choose dry leasing, however, only get the plane from the lessor.

Global Alliances

An arrangement for cooperation among several airlines is known as an airline alliance. They collaborate to sell, offer, and provide connections throughout their networks. Additionally, they guarantee advantages for connected travelers and their respective elite memberships; passengers and airlines benefit equally from alliances (Douglas & Tan, 2017). They provide additional options for travel with their home airlines, make the booking and connecting flights easier, and provide customers with more methods to redeem miles and elite rewards.

Airlines sell their services to new customers and locations without operating their own flights. Membership airlines may provide services to many more places than they could alone by merging their networks (Zou & Chen, 2017). There are several instances of this succeeding at scale: American Airlines and Japan Airlines as examples of OneWorld Alliance members. American Airlines can run a number of aircraft into Tokyo each day, providing connections to several internal Japan Airlines locations.

Alliances provide travelers with more alternatives that may be purchased as a single connecting ticket. Members of each airline’s frequent flyer program can accrue miles on all member airlines of the alliance. Member is assigned a level inside the alliance based on the airline’s superstar status, and this level will give uniform advantages to all member airlines (Migdadi, 2022). Additional baggage limit, a waiver of the booking and seat-selection costs, and expedited airport check-in, security, and boarding are a few examples of this.

Although many more airlines have joined them and several have departed, their operations remain primarily unchanged. They appear to be well-established and integrated, and their frequent flyer program is well-used, but there have been a few recent developments that might have an impact on them moving ahead (Payán-Sánchez, Pérez-Valls & Plaza-Úbeda, 2019). They provide one-way tickets and little frequent flier advantages. Passengers now have more choices than merely staying with their favorite alliance, and this trend is expected to continue.

Airline Revenue Management

The clearest examples of price and revenue management are widely mentioned as being used by airlines. The industry has made significant investments in the creation of complex systems for demand forecasting, inventory management, and monitoring and reacting to rivals’ pricing in the market (Bondoux, Nguyen, Fiig, & Acuna-Agost, 2020). They can use this to their advantage when looking for a competitive edge and bigger yields. However, technology simply serves as a tool for a more comprehensive approach. It is a development of the abilities possessed by the pricing teams, commercial executives, and flight analysts who must provide revenue outcomes.

Technology has, without a doubt, made it possible for teams in charge of price and financial management to react more swiftly, but it is probable that the benefit of these previous or future expenditures has been or will be under-realized. The first investment must go toward adopting a more comprehensive perspective on price optimization administration, in which airlines take a step back and think about their commercial goals and how they relate to the plans, structures, and methods used for price optimization planning. Airlines set lucrative ticket pricing depending on a plethora of variables, including willingness to purchase, competition, and destination, using a sliding scale incorporating price, inventory, promotion, and numerous sales channels (Wang, Wittman & Bockelie, 2021). By doing this, airlines may avoid having constantly set fares by always pricing based on what the market deems suitable. Taking cognizance of the opportunity that both airline and hotel customers are accustomed to pricing fluctuations is one way the hospitality sector may profit from adopting airline income management solutions.

Pricing sensitivity, or the possibility that a consumer will not buy anything because it is too expensive, is one of the most novel factors taken into account by revenue management services. The pricing strategy may be more effectively guided by an understanding of how price sensitivity varies across different consumer categories (Buyruk & Güner, 2021). Additionally, several airlines have put in place internal controls to improve, and in some cases even guarantee, their odds of maintaining total flights. Airlines that operate flights to and from particular locations negotiate deals with businesses that often conduct business in both cities, guaranteeing a predetermined quantity of tickets at a subsidized rate.

Conclusions

Passenger airlines are those that specialize in transporting passengers. Low-cost airlines often rely on two distinct methods than full-service carriers in order to give passengers less expensive tickets. Most passenger airlines operate a fleet of passenger aircraft that is either entirely owned by the airline or hired from companies that buy and lease passenger airliners. One of the most cutting-edge considerations made by revenue management services is pricing awareness or the chance that a customer will not buy anything because it is expensive.

Reference List

Bouwer, J., Saxon, S., & Wittkamp, N. (2021). ‘Back to the future? Airline sector poised for change post-COVID-19’. McKinsey and Company. Web.

Buyruk, M., & Güner, E. (2021). ‘Personalization in airline revenue management: an overview and future outlook’. Journal of Revenue and Pricing Management, 1-11. Web.

Bondoux, N., Nguyen, A. Q., Fiig, T., & Acuna-Agost, R. (2020). ‘Reinforcement learning is applied to airline revenue management’. Journal of Revenue and Pricing Management, 19(5), 332-348. Web.

Bieger, T., & Agosti, S. (2017). ‘Business models in the airline sector–evolution and perspectives’. Strategie Management in the Aviation Industry. Routledge. pp. 41-64. Web.

Czerny, A. I., Fu, X., Lei, Z., & Oum, T. H. (2021). ‘Post pandemic aviation market recovery: Experience and lessons from China’. Journal of Air Transport Management, 90, 101971. Web.

Castiglioni, M., Gallego, Á., & Galán, J. L. (2018). ‘The virtualization of the airline industry: A strategic process’. Journal of Air Transport Management, 67, pp. 134-145. Web.

Douglas, I., & Tan, D. (2017). ‘Global airline alliances and profitability: A difference-in-difference analysis’. Transportation Research Part A: Policy and Practice, 103, pp. 432-443. Web.

Hsu, C. P. C., & Flouris, T. (2017). ‘Comparing global airline merger experiences from a financial valuation perspective: An empirical study of recent European-based airline mergers’. Transportation research procedia, 25, 41-50. Web.

Khezrimotlagh, D., Kaffash, S., & Zhu, J. (2022). ‘US airline mergers’ performance and productivity change’. Journal of Air Transport Management, 102, 102226. Web.

Migdadi, Y. K. A. A. (2022). ‘The impact of airline alliance strategy on the perceived service quality: A global survey’. Journal of Quality Assurance in Hospitality & Tourism, 23(2), pp. 415-446. Web.

Naumovich, A. (2018). ‘Domestic Airline Mergers and Defining the Relevant Market: From Cities to Airports’. J. Air L. & Com., 83, 839. Web.

Oxley, D., & Jain, C. (2015). ‘Global air passenger markets: riding out periods of turbulence’. IATA The Travel & Tourism Competitiveness Report, pp. 59-61. Web.

O’Connell, J. F. (2018). ‘The global airline industry’. The Routledge companion to air transport management. Routledge. pp. 11-28. Web.

Payán-Sánchez, B., Pérez-Valls, M., & Plaza-Úbeda, J. A. (2019). ‘The contribution of global alliances to airlines’ environmental performance’. Sustainability, 11(17), 4606. Web.

Statista. (2022a). Global air traffic – scheduled passengers 2004-2022, Web.

Statista. (2022b). Low-cost carrier market – global capacity share 2007-2020. Web.

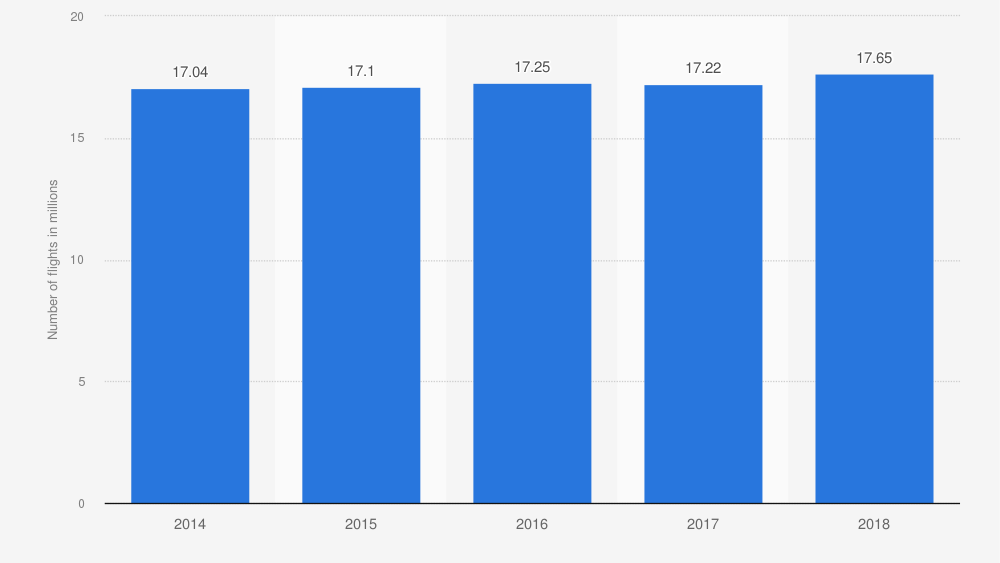

Statista. (2022c). Global airline alliances’ total number of flights 2014-2018. Web.

Wang, K. K., Wittman, M. D., & Bockelie, A. (2021). ‘Dynamic offer generation in airline revenue management’. Journal of Revenue and Pricing Management, 20(6), p. 654-668. Web.

Yan, J., Fu, X., Oum, T. H., & Wang, K. (2019). ‘Airline horizontal mergers and productivity: empirical evidence from a quasi-natural experiment in China’. International Journal of Industrial Organization, 62, 358-376. Web.

Zou, L., & Chen, X. (2017). ‘The effect of code-sharing alliances on airline profitability’. Journal of Air Transport Management, 58, pp. 50-57. Web.