Introduction

The knowledge of economics is crucial for every society since it enables companies and individuals to understand how the market works. Economics encompasses several areas that each contribute to the stability of a given company or country, which is why it is essential to understand the concepts. Traffic congestion, opportunity cost, and market equilibrium are crucial areas that can help in addressing the economic needs of a business or country.

The Economics of Traffic Congestion

Traffic congestion results from the need for mobility and the desire for individuals and businesses to meet their business goals. Traffic congestion slows the economy because most businesses fail to meet their target markets in time (Marshall & Dumbaugh, 2020). On the positive side, traffic congestion provides an opportunity for economic growth. According to Rahayu and Kipuw (2020), this is the ideal time for creating toll centers on expressways to generate more income while speeding up transportation. Thus, the congestion is best for economic growth if the government builds more roads with toll centers.

Opportunity Cost

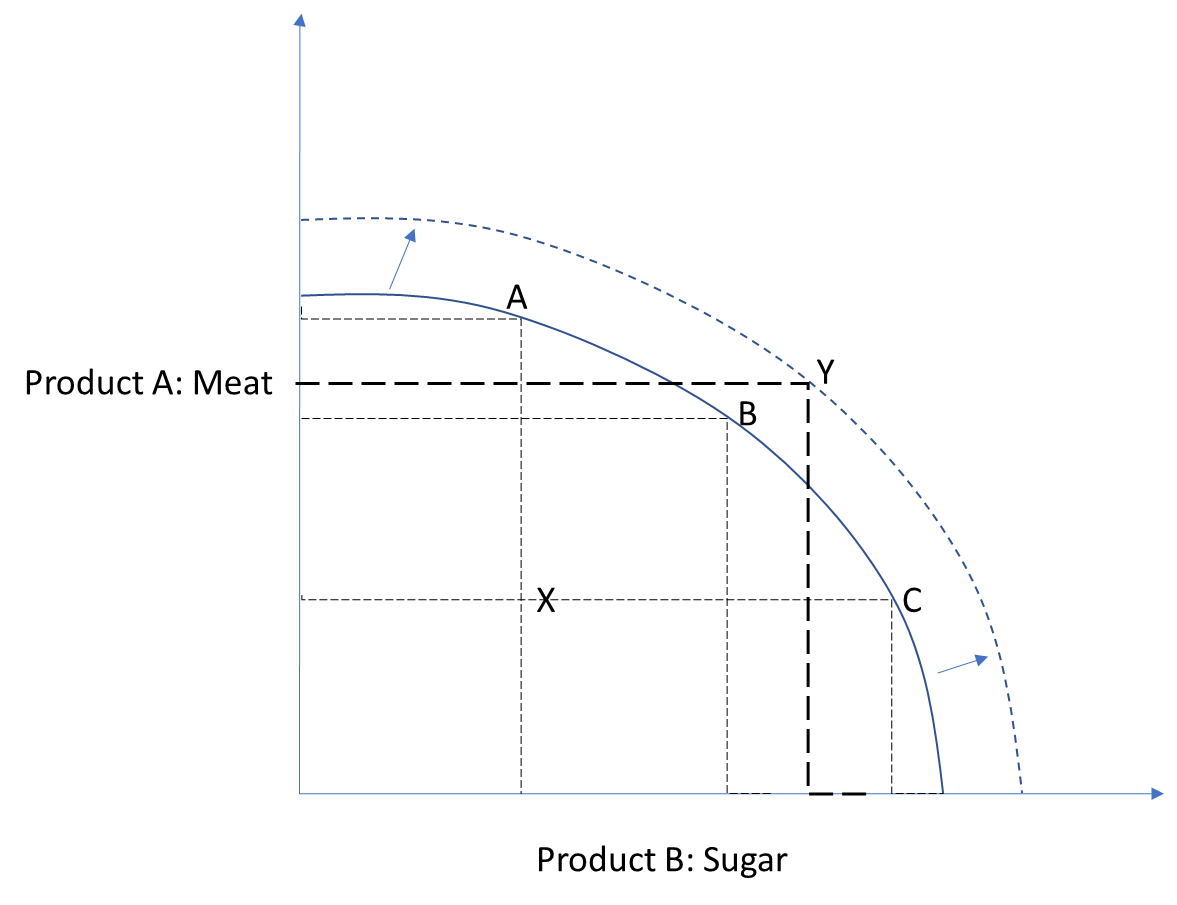

Opportunity cost refers to the value a business, an individual, or a country misses by choosing one alternative over the other. It is expressed as the return on the best-forgone option less than the chosen option (Bellemare, 2018). A country that with meat and sugar, as shown in Figure 1 below, can produce 1000 units of meat and 1000 units of sugar as indicated in point B. It can also produce more meat (point A) or sugar (point C). Point X is where the country does not use its resources efficiently, while Y is where it cannot attain them based on its available resources. Shifting the production from A to B reveals a smaller decrease in meat production compared to the increase in sugar production. On the contrary, moving from B to C reduces meat production by almost 50% but increases sugar production by 75%. All these points indicate resource allocations and the impacts of such strategies on the opportunity costs of the two products.

Market Equilibrium

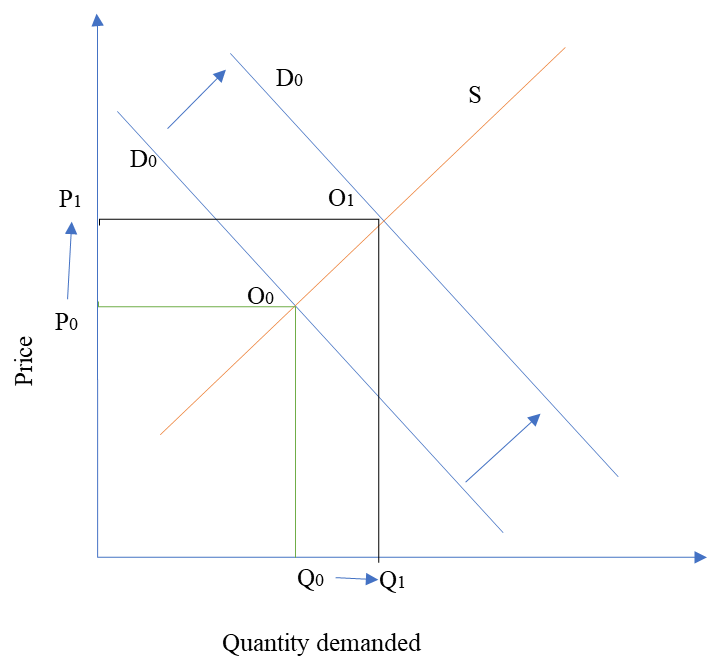

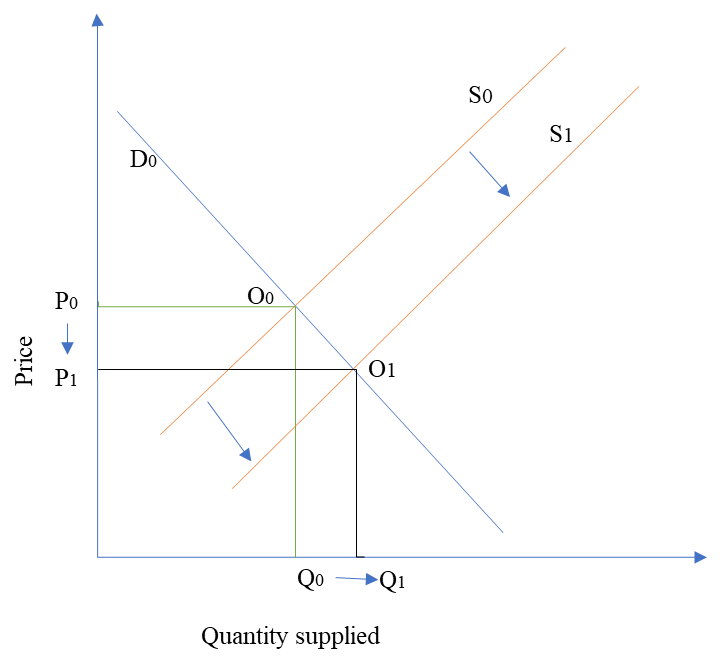

Market equilibrium refers to the point at which the product demanded by customers equals that supplied by sellers. According to O’Sullivan et al. (2012), the equilibrium is mainly affected by the price of the product or service, whereby the suppliers and the buyers are satisfied with the charges. The forces resulting in market equilibrium can be considered from the supply and demand, since a shift in one, results in the change of market equilibrium.

Figure 2 above shows the scenario for pizza demand and the associated price. When demand for pizza increases, the suppliers increase their product prices. For instance, if the initial quantity demanded was Q0 and the price charged was P0, the market equilibrium settled at O0. An increase in demand in Q1 shifts the market equilibrium to O1, enabling the suppliers to increase their prices from P0 to P1. On the other hand, Figure 3 below presents the scenario where the supply increases. If the initial market equilibrium was O0 at a supply of S0 and price P0, an increase of supply to S1 shifts the equilibrium to O0. Consequently, there is a surplus in the market, forcing the buyers to sell at a lower price of P1.

Conclusion

In conclusion, the analysis conducted for traffic congestion, opportunity cost, and market equilibrium indicates how these aspects impact the economy. Traffic congestion impedes the development of a country but introducing expressways and toll centers becomes avenues for more revenue. Opportunity cost enables a business to choose an alternative product, thus producing more of it while reducing the production of another to gain tradeoffs needed in the economy. Finally, changes in demand and supply affect the prices of commodities due to changes in equilibrium prices and quantities demanded and supplied.

References

Bellemare, M. F. (2018). Contract farming: Opportunity cost and trade‐offs. Agricultural Economics, 49(3), 279-288.

Marshall, W. E., & Dumbaugh, E. (2020). Revisiting the relationship between traffic congestion and the economy: A longitudinal examination of US metropolitan areas. Transportation, 47(1), 275-314.

O’Sullivan, A., Perez, S. J., & Sheffrin, S. M. (2012). Economics principles, applications, and tools, 7th Edition. Pearson.

Rahayu, L., & Kipuw, D. M. (2020). The correlation between toll road development and the improvement of local economy (case study: The Soroja toll road). International Journal of Sustainable Transportation Technology, 3(1), 26-36.