“An increase in demand causes a price increase, but an increase in price causes a decrease in demand. Demand increases, therefore, largely cancel themselves out.”

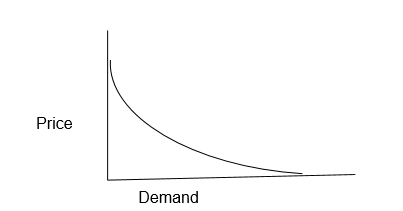

Based on classical theories of economic and the real-world situation, an increase in demand can be attributed to an increase in prices. It implies that demand is the factor behind an increase in price. A simple demand curve is illustrated below.

It is important to note that demand in the market is influenced by other market factors. In addition to that, the curve demonstrates that when the demand for a product is high, the price is high and when the price for a similar product appreciates, the demand diminishes. The price however is not the only factor that influences demand, as illustrated above, even though other factors remain constant.

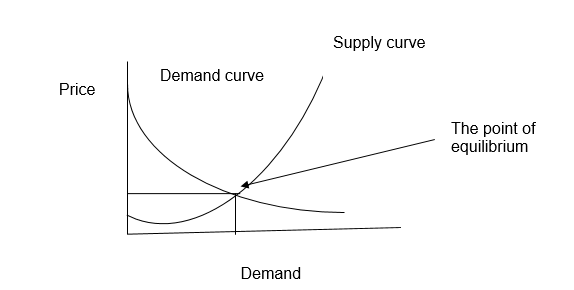

However, an interaction between the two factors of demand and supply indicates that when prices for different commodities are raised, the willingness for buyers to purchase such commodities reduces, but when the price reduces, the willingness to purchase diminishes.

The canceling out effect is demonstrated in the demand and supply curve illustrated below. Equilibrium or canceling out is reached when both demands for commodities and the supply for the same commodities attain an equilibrium value.

When the demand for a commodity increase, the inventory levels for the commodity have to be increased to cancel out the rising effect of demand. On the other hand, when the supply for a commodity increases, the demand for the same commodity decreases because inventory levels have gone up, implying that inventory levels for a product have to be decreased to restore the equilibrium position of the demand and supply for the commodity.

However, the classical economic model focuses on the forces of demand and supply in a single market condition and does not reflect the dynamic nature of market conditions. It is possible, therefore, a situation to occur where the demand is low, the price is low, and the supply is low. On the other hand, prices can be high, demand high, and the supply of a product still high. Different commodities and market environments sometimes change the behavior of the market.

During 2000, Orlando, Florida, was growing rapidly, with new jobs luring young people into the area. Despite increases in population and income growth that expanded demand for housing, the price of existing houses barely increased.

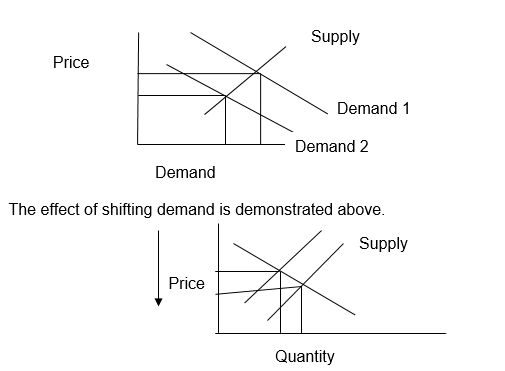

Demand for a product can be high, but the price for the commodity remains the same despite a rise in the income level of the consumers for the product. That is well illustrated in the demand and supply curve illustrated below and as discussed below.

The effect of shifting the quantity of the units with supply on the pricing of the housing units is illustrated above. When tie inventory level remains constant, as in the case of housing at Orlando, implying that the demand for the number of housing units was equal to the desired number of housing units. That condition was descriptive of an equilibrium situation. Prices remained constant because the inventory level of housing units was equivalent to the demand for housing. That also implies that the price change delay had to occur because of the equilibrium conditions that had been achieved.

Another reason that led prices to remain the same was due to t the ft that providers of housing units built more units to accommodate the rise in demand for the housing units.

When excess demand exists for tickets to a major sporting event or a concert, profit opportunities exist for scalpers. Explain briefly using supply and demand curves to illustrate. Some argue that scalpers work to the advantage of everyone and are “efficient.”

I do agree with the statement that profit opportunities exist for scalpers. When the demand for service increases, particularly in the sporting field, people will have exhibit the behavior of demanding services from scalpers to satisfy their needs. That is so because the demand has risen for the tickets and the supply is fixed, therefore an alternative to satisfy the demand is sought fro from the scalpers.

To “support” the price of some agricultural goods, the Department of Agriculture pays farmers a subsidy in cash for every acre that they leave unplanted. The Agriculture Department argues that the subsidy increases the “cost” of planting and that it will reduce supply and increases the price of competitively produced agricultural goods. Critics argue that because the subsidy is a payment to farmers, it will reduce costs and lead to lower prices. Which argument is correct?

The correct argument, in this case, is that subsidies increase the price of the final product. Based on the law of demand and supply, when the supply for a commodity reduces, the possibility of demand for the same product rises because the inventory level of the product is low. The department of agriculture bases its argument on delaying a product from reaching the market. That reduces the inventory level of the commodity with the supplier creating a rise in demand as the supply shifts to the left, the pricing shifts to the right.

A female student who lives on the fourth floor of Bates Hall is assigned to a new room on the seventh floor during her junior year. She has 1 heavy box of books and “stuff” to move. Discuss the alternative combinations of capital and labor that might be used to make the move. How would your answer differ if the move were to a new dorm 3 miles across campus, and to a new college 400 miles away?

The right combination of capital and labor for the student to optimize output is to use the most feasible combination of technology and human capital for optimal results. Assume the output is Q and the input variables such as technology and individual energy is x, then, for optimal results, the student has to base the calculation on the function, Q = f (X1, X2, X3,…, Xn). However, if the student has to move 400 miles away, then the right mathematical relation to use is Q = a + bX1 + cX2 + dX3 +, where the variables are influenced by distance to be covered and associated costs.

Do you agree or disagree with each of the following statements?

- For a competitive firm facing a market price above average total cost, the existence of economic profits means the firm should increase output in the short run even if the price is below marginal cost.

I do agree with the statement. A firm survives on profits generated from the sales of its products. However, completion may force a company to lower the price of its products to just below the marginal cost to survive in the short run. That is the case because unfair completion practices do not last for a long time, but exists for a short period. When production is increased under these conditions, supply for the same product increases in the market sparking or stimulating demand for the product. It may be beneficial in the short run to increase production to sustain supply and maintain a market share before the prevailing conditions cease to exist.

- If marginal cost is rising with increasing output, the average cost must also be rising.

The accumulated effect of the rising marginal cost will indeed have a final impact on the rise of the final cost of the product and the cost of production.

- Fixed cost is constant at every level of output except zero. When a firm produces no output, fixed costs are zero in the short run.

Fixed costs may arise when a firm outputs products for sale or does not at all. Fixed costs remain constant even though a firm engages in production or not. An example is when a bank does not operate for some time, fixed costs will still be incurred in the form of security and the infrastructure. A car manufacturer must pay rent irrespective of engaging in the production or not. Fixed costs help economists evaluate the performance of a business.

For each of the following businesses, what is the likely fixed factor of production that defines the short run?

- Potato farm of 160 acres

They include salaries for firm employees, the cost of the land, the cost of machinery, and administrative expenses.

- Chinese restaurant.

Rent paid for the housing facility hosting the restaurant.

- Dentists in private practice.

Cost of equipment used in the practice, bills due to electricity, telephone bills, and consultancy services.

- Car dealership

They include the cost of renting the ground for hosting vehicles, agreements, security, and networking costs.

- Bank

Back office operations, labor agreements, gatekeeping, computer information systems, salaries, and network infrastructure are among the fixed costs incurred by a bank.