Financial Statements for the Year Ended 31 December Y5

I am pleased to present the Financial Statements for the year ended on 31 December Y5 to the Directors of Business Plc. The enclosed statements are the ones that follow:

- Statement of Comprehensive Income for the year ended 31 December Y5;

- Statement of Financial Position as on 31 December Y5;

- Statement of Changes in Equity for the year ended on 31 December Y5;

Also included in the statements, is a set of journal entries that should be present in your books in order to tally the balances in the audited financial statements.

During our preparation of the statements, we came across the information that we would like to present, explain its impact on the financial statements and suggest a way forward on what had to be done with reference to the United States Generally Accepted Accounting Principles (USGAAPs), and the International Financial Reporting Standards (IFSR).

Inventory

Inventory has been valued at $63,648,000, as shown in the trial balance. However, this includes raw materials that cost $4,960,000 that are only worth $3,200,000 in the market now. A depot with $2,000,000 worth of finished goods was missed off the count. Returns with an original sale value of $640,000 have not been included in the valuation yet, but they could be sold for $320,000 if we did repairs of $80,000.

The missing count of the depot with finished goods has an effect on the cost of closing inventories, hence overstating the net profits (Holthausen & Watts 2001). Since income tax is calculated on the net profits, the tax due to the government is overstated. A journal debiting inventory and crediting the cost of sales ought to be passed.

Regarding raw materials’ worth $4,960,000 that could only fetch $3,200,000, the USGAAPs state that assets shall be recorded at cost. However, when the market value of an asset (revenue-producing ability) declines below its cost, the general rule is that the historical cost principle is abandoned because the future utility of the asset is changed (Kieso, Weygandt, Warfield 2010, p. 471). The market value is therefore preferred over the historical cost principle. The “Lower of cost or market value” rule means that assets are to be valued at their historical cost or the cost of replacing them (market value), whichever is lower. It is therefore advisable to pass a journal to reflect the current market value of inventory by debiting the cost of sales and crediting inventory with the difference between the original cost and the current market value.

The same “Lower of cost or market value” rule applies in the third scenario where the market value includes the cost of repairs. We, therefore, have to pass a journal debiting the cost of sales and crediting inventory with the difference in value.

Insurance, Rates and Rent

Insurance of $984,000 for the whole business runs from 1 September Year 5 to 31 August Year 6 and was paid in August Year 5. Rates were $960,000 and were paid until 31 March Year 6. A rent of $2,560,000 per quarter was paid on 31 March Year 6. All these figures are included in Administrative expenses in the income statement.

According to Encyclopedia of Business, the Matching Concept “is an accounting principle that requires the identification and recording of expenses associated with revenue earned and recognized during the same accounting period”. Thus, under this concept, the expenses during certain periods present the prices of the assets for the revenues (Barth, Beaver & Landsman 2001, p. 80). Therefore the amounts paid for insurance, rent and rates that spill over to Y6 should be debited to the prepayments account where they effectively become a current asset to Business Plc and credited to the respective expenditure accounts to match the revenue of Y5 with the expenses incurred in deriving it.

Share Capital and Dividends

Section 30 (2) of the Corporations Act states that dividends must not be declared unless the directors have made a recommendation to the amount. This dividend should be within the amount suggested by the directors. In this case, the directors do not declare any dividends but they are under the pressure from the shareholders to do so. Section 103 states that “subject to the provisions of the Act, the directors may pay dividends if it appears to them that they are justified by the profits of the company available for distribution” (Dividends n.d.). The amendment of Section 254T however makes paying out of dividends more flexible as long as the following conditions are met:

- The company’s assets exceed its liabilities immediately before the dividend is declared and the excess is sufficient for the payment of the dividend,

- Payment of the dividend is fair and reasonable to the company’s shareholders as a whole,

- Payment of the dividend does not materially prejudice the company’s ability to pay its creditors.

Since Business Plc satisfies these conditions as shown by its different ratios, the best way is to make the right issue that effectively reduces the share capital of the company and releases part of it to retained earnings to be used as dividends. The following journal entries, therefore, need to be passed to effect this transaction:

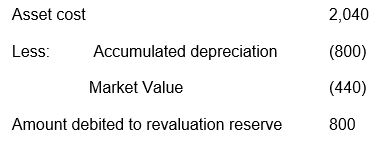

PPE Revaluation

Plant and equipment that cost $2,040,000 in year 1, have been revalued at $440,000. The depreciation policy was to write off this asset over 10 years with a residual value of $40,000. A full year of depreciation has been charged during the years 1 to 4, but nothing was done about this in the year 5 figures. The remaining useful economic life is judged to be 5 years including year 5 with the same residual value. All depreciation is included in the Administration expenses. In this, a new account, the revaluation reserve account is opened as part of equity. The loss of value of plant and equipment is debited to this account and the asset account. The calculation is as under:

The amount of credit to an asset account is an accumulated depreciation plus the cumulative depreciation. Thereafter the depreciation expense is charged based on the net asset value, that is, (440,000-40,000)/5=80,000

Operating Lease

Included in administrative expenses is $300,000 of leasing costs. This is the deposit per the terms of the lease. The first payment is due to go out in month 1 of year 6. The terms of the deal are 3 payments of $100,000 as a deposit and then 33 equal installments of the same amount for 33 months. The lease is for a machine that will speed up production to satisfy the largest contract the company has ever won. The capital cost of the equipment is $3,168,000 and the lease charges are $432,000 spread equally over all 36 lease payments. Repairs and maintenance costs become the responsibility of The Business as soon as they have signed that the delivery and installation are satisfactorily completed. The equipment has an expected useful economic life of 5 years. The lease was signed and the deposit was paid in year 5, but the equipment will be delivered in year 6. The following corrective journals should be passed:

The asset becomes the company’s once the lease contract is signed, the lease charge should commence once the asset is commissioned and ready to be used by the company.

Intangible Non-Current Assets

Research has been going on for the past 5 years into whether it would be possible to make a product that would prevent current customers from going to the competitors. At the end of the year, 4 tests provided conclusive evidence that a new product could be developed and that would beat the competition. It got a code-named ThetaX1. Development started immediately, and in October of Year 5 some consumer testing gave very positive results that mean full production should start in March Year 6 and sales should start in the Autumn of Year 6. The research and development costs in Year 5 were $10,032,000. The research cost for the previous 5 years totaled $31.2m and was included in administration expenditure in prior years.

The costs of research and development activities could be treated as an expense and be charged to the profits and loss account in the period they re-incurred, or they can be deferred and amortized over future periods in order to match with the costs of the activities with the benefits derived from them. When amortizing, the cumulative costs are treated as intangible assets. In this case, the $10,032,000 spent on R&D in Y5 and included in administrative expenses should be debited to the Intangible assets and be capitalized for amortization when the business starts deriving benefits from the research carried out.

Conclusion

As shown by the ratios calculated below, the company is not doing very well.

For example, the company is not in a position to meet its current financial obligations from its current assets. This may discourage the payout of dividends and deal a blow to investor confidence. It may also mean that for the company to meet its current financial obligations, it may be forced to dispose of part of its non-current assets.

The company’s debt position is also not very healthy. The debt is more than 5 times the stockholders’ equity. We would therefore advise that the company hold on to its dividend payout.

The financial statement has been prepared based on the USAAGPs and IFRS, taking into consideration the normal trends within the industry.

References

Barth, ME, Beaver, WH & Landsman WR, 2001 ‘The relevance of the value relevance literature for financial accounting standard setting: another view’, Journal of accounting and economics, vol. 31, no. 1, pp. 77-104.

Dividends n. d. Company Law Solutions. Web.

Encyclopedia of Business, 2nd edn, Reference for Business, Man-Mix, Reference for Business. n.d.

Holthausen, RW & Watts RL 2001, ‘The relevance of the value relevance literature or financial accounting standard setting’, Journal of accounting and economics, vol. 31, no. 1, pp. 3-75.

Kieso, DE, Weygandt, JJ & Warfield, TD 2010, Intermediate Accounting: IFRS Edition, John Wiley & Sons, New York.