Introduction

An overview of a business company is generally required for the proper analysis of the company’s performance and for defining the key aspects of its activity. Originally, the key aspects of the company’s strategy and performance may be briefly outlined in reviews and newsletters. The aim of this paper is to analyze the Toll Holdings PTY LTD business performance, including the company overview, financial performance, with the calculation of financial ratios, media coverage of the company, and the teamwork aspects, including the information on stakeholders of the company. The entire analysis will represent the financial and business image of the company’s performance, thus, providing the solid basis for the deeper analysis of the company.

Company Overview

The toll is a regional company, engaged in the sphere of integrated logistics. Thus, it provides a wide range of logistics and transportation services, associated with the rail freight service, container handling, storage and rent, temperature-controlled transportation, ship freight and overseas transportation, and also rail and air passenger and cargo transportations. (Rigoglioso, 2006) The accounting period which is covered in the paper is the 2008-2009 period, as it is the latest financial data available and which gives a clear representation of the development tendencies and values of the financial performance.

The board of directors entails three CEO:

- Chief Executive Officer Toll Global Resources David Jackson

- Chief Executive Officer Toll Global Logistics Wayne Hunt

- Chief Executive Officer Toll Global Forwarding Hugh Cushing (England, 2008)

Managing director Paul Little is on the top of the managerial structure.

The members of the Board of Directors are:

- Ray Horsburgh AM Chairman

- Harry Boon Independent Non Executive Director

- Mark Smith Independent Non Executive Director

- Barry Cusack Independent Non Executive Director

- Frank Ford Independent Non Executive Director

- Bernard McInerney Company Secretary (Leighton and Coakley, 2008)

The annual results and the dividends paid to entail the following data:

Annual Revenue totals up to USD 6500 million. The company made 80 acquisitions in 2009, and the number of employees totaled 35 000+. There are more than 800 sites and places where the company operates, and the total warehouse capacity is close to 3 000 000 m2. The company’s average annual revenue totals up to $7 billion, while the issued capital is approximately $400 million. ( M6 Toll PR Deal a Coup for Warman, 2004)

Financial Reports Analysis

Profitability ratios entail several indexes, which are gross profit margin, return on assets, and return on equity:

(P/$ Rate Closes at P49.495/$ 1, 2008)

Liquidity Ratios

As for the capital structure analysis, the following factors should be considered:

- Taxes ($ 29,8 million)

- Risk (Integrated risk management programs aimed at ensuring risks are identified, assessed, and appropriately managed, and include regular reports to the Board on the status of business risks. The Audit and Financial Risk Committee also receives reports on financial risks in accordance with its charter, and is further responsible for reviewing the effectiveness of the Group’s risk management and internal control system (Kasper, Helsdingen and Vries, 2009))

- Asset characteristics (including the calculated ratios)

- Costs of financial distress ($ 19,9 million)

Thus, considering the ratios and return indexes, as well as the asset analysis (total asset rate – $ 5 009,7 million) and the liabilities (total liabilities – $ 1 378,7 million), it should be stated that the capital structure of the company is equity financed. (Droms, 2007)

Market Performance Ratios

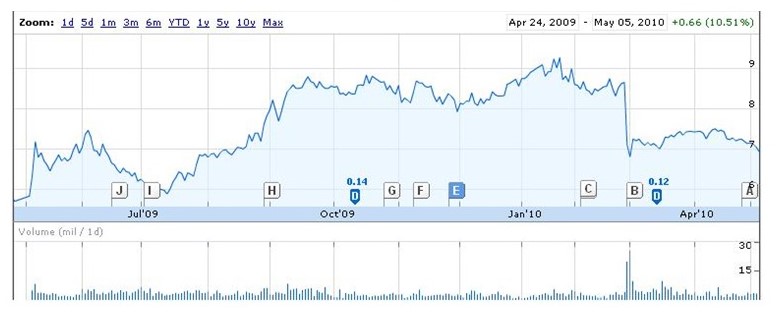

The p/e performance of the company is represented on the following chart:

The current situation is the following:

- P/E – 21.75

- Vol. 2.95M

- Mkt cap 4.85B

- Div/yield -/3.60

- EPS 0.32

- Shares 699.36M

Asset Efficiency Ratios

Company and Media Coverage

The media coverage of the company mainly entails online sources on the matters of the company profile and the performance in the sphere of logistics and transportation. Considering the fact, that the aspects of logistics services develop constantly, the company expands and improves its business performance. Thus, these innovations play an important role in the comments of the competitors and consumers of the company. (Bhimani, 2008)

The most important fact, which is stated in media sources is the differentiating factor of the company:

Toll Holdings’ differentiating factors are arguably its strong record of profit growth and its exceptional record in cutting costs. Its post-de-merger debt-free structure has provided an exceptional platform for future acquisition growth in Australia and abroad, particularly in Asia. Its market size and scope mean it is well-positioned to make large acquisitions, leveraging off its existing low-cost base and quality management skills. (Christopher and Peck, 2008)

In the light of this statement, it should be emphasized that the logistics operator of the Asian and Australian market is featured as the reliable partner, and, considering the sizes of the analyzed market, it should be emphasized that these aspects are closely associated with the extensive development of the company. (Companies Having Second Thoughts over Property; Location Credit Squeeze Takes Toll on Holdings, 2008)

Independently on the comments of the company’s performance and profile, the financial performance of the company does not change, as these comments are not able to influence the company’s customers’ base, as the company is featured with a stable reputation of a reliable partner, and the possible negative comments are avoided by the timely solution of the appearing problems. (Novack, Novack and Goodbread, 2003)

Company Announcements

The stated analysis period of the company’s announcements (2007 – 2009) is featured with numerous announcements and the various market share reactions for these announcements. Originally, these were associated with the capital structure of the company and the values associated with expansion. (Wielemaker, Elfring and Volberda, 2001) Originally, the market processes fluctuated considering not only the current announcements and actions but also the financial forecasts, associated with these announcements. Thus, July 2009 market share decrease is associated with the announcement of decreasing the outdated ship fleet, as the number of accidents was too numerous. This inevitably meant the decrease in the sea transportation volumes, thus, the shares decreased, and the company experienced additional losses. Nevertheless, the p/e index grew for the following period, which also caused the increases in market share values, however, this period was not featured with the serious announcements. (Tidd, Bessant, 2006)

Conclusion

The business performance of the Toll Holdings in the sphere of global logistics and transportation is featured with the extensive development and the steady growth of the volumes of transportation. Originally, the provided market analysis revealed the positive ratios, including effectiveness, liquidity, and market performance ratios.

Reference List

Bhimani, A. (Ed.). 2008. Management Accounting in the Digital Economy. Oxford: Oxford University Press.

Christopher, M., & Peck, H. 2008. Marketing Logistics (2nd ed.). Boston: Butterworth-Heinemann.

Companies Having Second Thoughts over Property; Location Credit Squeeze Takes Toll on Holdings. 2008. Daily Post (Liverpool, England), p. 10.

Droms, W. G. 2007 Finance and Accounting for Nonfinancial Managers: All the Basics You Need to Know (4th ed.). Cambridge, MA: Perseus Books.

England, R. S. 2008. The Mounting Toll. Mortgage Banking, 68, 38

Gotanda, J. Y. 2008. Compound Interest in International Disputes. Law and Policy in International Business, 34(2), 393

Kasper, H., Helsdingen, P. V., & Vries, W. D. 2009. Services Marketing Management: An International Perspective. New York: John Wiley & Sons.

Leighton, R. M., & Coakley, R. W. 2008. Global Logistics and Strategy, 1990-2000. Washington, DC: Office of the Chief of Military History.

M6 Toll PR Deal a Coup for Warman. 2004. 29.

Novack, R. A., Grenoble, W. L., & Goodbread, N. J. 2003. Teaching Quality in Logistics. Journal of Business Logistics, 14(2), 41

P/$ Rate Closes at P49.495/$ 1. 2008. Manila Bulletin, p. NA.

Privatisation to Push Toll’s Growth. 2003. Business Asia, 10, 21.

Rigoglioso, M. 2006. Shipping Companies to the Rescue. Stanford Social Innovation Review, 4, 64

Tidd, J., Bessant, J. 2006. Managing Innovation: Integrating Technological, Market and Organizational Change (2nd ed.). New York: John Wiley & Sons.

Wielemaker, M. W., Elfring, T., & Volberda, H. W. 2001. How Well-Established Firms Prepare for the New Economy. International Studies of Management & Organization, 31(1), 7.