Introduction

Since the culmination of the financial crisis, the banking system in the globe has witnessed heightened interest rate risk (IRR). The IRR is currently almost reaching the pre-recession levels, thereby calling for the integration of relevant measures that can alleviate the situation. The issue mainly affects small banks compared to the situation for big banks in the industry. In this concern, it is crucial to address issues that trigger the increasing IRR in the industry by focusing on areas such as the competitiveness of the environment, products, and services.

As such, in contemporary times, managers of banking organizations identify the quantification and administration of interest rate threats as crucial elements in their scope of work. In this respect, reviewing the literature to gain an understanding of the causes of IRR, its effects on financial institutions, and/or how financial institutions manage and measure IRR is relevant in the context of this paper.

The Causes of IRR

According to Chan-Lau, Liu, and Schmittmann (2015), IRR has a considerable influence on the financial health of banks. As such, it is crucial to examine factors that shape interest rate movements, which are posing a considerable threat to banks’ capital base and earnings. Several causes expose the banking system to IRR. According to the Federal Housing Finance Agency (2013), the notable sources of IRR include the “repricing risk, yield curve risk, basis risk, and optionality” (p. 1). As Sharifi, Saeidi, and Saeidi (2014) imply, the repricing risk is one of the leading sources of IRR in the banking sector.

According to Aspal and Nazneen (2014), timing variations associated with the maturity and repricing of financial institutions’ liabilities, property, and off-balance-sheet (OBS) positions account for the emergence of IRR. Repricing inconsistencies are part of the basic operations of the banking sector. Consequently, as the Basel Committee on Banking Supervision (2004) reveals, such discrepancies may subject financial agencies to undesired returns while also affecting the institutions’ economic value, especially when income rates fluctuate (Bessis, 2015). In this view, banks that use short-term deposits to fund a long-term fixed-rate loan may record reduced revenue and lower economic value in case the interest rate increases. Therefore, as Aspal and Nazneen (2014) reveal, mismatches in repricing pose a considerable threat to the financial health of commercial banks when interest rates vary.

Repricing variations have the potential of subjecting financial agencies to differences in the gradient and nature of the productivity curve. Consequently, according to Aspal and Nazneen (2014), the productivity curve threat triggers IRR in a manner that undermines the financial status of banking organizations. Notably, unanticipated movements of the yield curve threaten banks’ economic value and income. In most cases, investments in fixed instruments may expose banks to adverse interest rates, which undermine their income levels. Important to note, Alessandri and Nelson (2015) insist that market yield variations have considerable effects on the price of a given fixed-income instrument. Therefore, the price of a bond in which a particular bank has invested in may decrease due to the increase in market yields. Therefore, the yield curve risk is a notable source of IRR in the banking sector since it affects the prices of fixed-income instruments such as bonds.

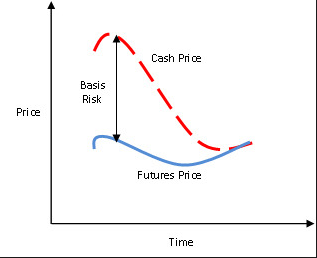

According to Bessis (2015), the basis risk is also a major trigger of IRR in the banking system. Figure 1 below illustrates how the basis risk can be determined.

Particularly, any defective alteration of the rates gained and paid on various instruments with otherwise identical repricing attributes leads to the emergence of the basis risk. As such, interest rate fluctuations may prompt the emergence of unanticipated currency movement variations and income spread with reference to liabilities, property, and Off-Balance Sheet tools. It is crucial to point out that these instruments have identical repricing rates of recurrence. In the event banks apply different approaches when determining the interest attained in each section of the balance sheet, they are exposed to the basis risk that lowers the final interest returns (Alessandri & Nelson, 2015). In this view, the basic risk is also an essential trigger of IRR in the banking industry.

Esposito, Nobili, and Ropele (2015) reveal various options that underlie various liabilities, assets, and OBS instruments in the financial sector. In a formal sense, Esposito et al. (2015) clarify that optionality offers the proprietor the privilege, as opposed to the obligation, to purchase, retail, or modify the cash movement of a given instrument or a pecuniary agreement. Notably, options may appear in the form of individual instruments, including over-the-counter (OTC), as well as exchange-traded options. Additionally, options may also be integrated within standard instruments. In this respect, instruments with underlying options, including bonds and notes, offer the respective holders the liberty to make transactions at their will. As such, the optionality offered to depositors influences them to make withdrawals at any given time. Consequently, options have the potential of undermining the profitability of banks.

The Effects of IRR on Financial Institutions

Undoubtedly, as earlier mentioned, the IRR issue poses significant effects on the income and the economic value of financial institutions. In this respect, the two adverse effects of the IRR problem in the financial sector represent distinct but complementary views of evaluating IRR exposure to banks. Therefore, assessing the degree to which the IRR problem undermines earnings and the worth of banking institutions is crucial.

Any discrepancies in interest charges in the financial industry significantly affect the accumulated earnings of the particular parties. According to Bessis (2015), many financial institutions approach the aspect of monetary threat management by assessing the effect of interest charge fluctuations on the earnings realized over a specified financial year. According to Bloom (2014), managers of financial institutions identify outright losses or lessened earnings as an issue that is directly influenced by drastic changes in interest rates. Risk managers take account of the IRR issue since it contributes to the inadequacy of capital while at the same time undermining the prevailing market confidence. In this respect, reduced earnings arising from IRR affect the financial stability of banks negatively.

The net interest income is one of the identified areas that are affected by the IRR issue in the banking sector. In this view, Chan-Lau et al. (2015) hold that IRR may influence the disparity between the final interest returns and the cumulative interest fees. Important to note, most banks realize their accrued earnings from the net interest income. As a result, such net interest revenue is an important aspect of profitability.

Nonetheless, financial institutions widen their operations into activities that generate income through fees, as well as other products and services that create non-interest returns. Surprisingly, the unpredictability of interest charges in the market also affects non-interest income activities, thereby denoting the degree to which IRR affects the anticipated earnings of financial institutions. Currently, income realized through transaction-processing fees is also sensitive to the fluctuation of interest charges. This state of affairs reveals that non-interest returns are equally influenced by changes in the prevailing interest fees (Esposito et al., 2015). Therefore, varying interest rate settings have a substantial impact on the earnings of financial institutions.

IRR also poses significant effects on various portfolios that determine the economic value of financial institutions. In this concern, according to Jiménez, Lopez, and Saurina (2013), the instability of interest charges is identified to influence the monetary worth of a financial institution’s expenses, property, and Off-Balance Sheet instruments. Thus, supervisors, managers, and shareholders identify the fluctuation of the prevailing interest fees as a crucial consideration since it determines the monetary worth of financial institutions. Important to note, as Jokipii and Monnin (2013) assert, the economic significance of a financial institution is a representation of the anticipated cash flows of a bank. Since material goods, expenses, and OBS conditions influence the cash flow of a financial institution, it is important for the market to establish stable interest rates since they affect the mentioned components.

Notably, the worth of a financial organization may be obtained after identifying the disparity between the anticipated cash flows on expenses and the probable currency movement on resources before adding the value to the projected net money circulation realized from the institution’s OBS positions (Bloom, 2014).

In this view, discrepancies in interest charges have a significant influence on currency movements in financial institutions. According to Taiwo and Adesola (2013), the influence is substantial since it determines the actual worth of the financial organization. Therefore, shareholders, supervisors, and managers need to continually engage in effective and efficient risk management practices for the sake of bolstering the economic significance of a particular commercial bank.

In line with Jiménez et al.’s (2013) views, the IRR issue also prompts managers, supervisors, and shareholders to assess the impact of past interest rate fluctuations on the current financial performance of a given financial agency. In this respect, IRR necessitates the evaluation of the past and current interest rate unpredictability to obtain a picture of the prevailing and future financial position of the banking system. Additionally, instruments not associated with market interest rates also record gains or losses due to the past and current interest rate fluctuations, thereby denoting the impact of IRR on the net worth of a bank (Taiwo & Adesola, 2013). Therefore, the issue of IRR is central when it comes to determining the financial performance of multiple and different players in the banking sector.

The Measurement and Management of IRR by Financial Institutions

Financial institutions may apply several approaches to managing IRR. The management of the issue usually starts with the measurement of IRR. In this respect, according to Beets (2004), banks have the option of incorporating either the GAP analysis or financial derivatives to facilitate the measurement, as well as the management of IRR. The two approaches employ different techniques of measuring and managing IRR in the banking system.

How GAP and Financial Derivatives Work

GAP analysis entails a fixed evaluation of threats that are regularly linked to the net interest returns (margin) targeting. According to Koch and MacDonald (2014), GAP analysis emphasizes the determination of the disparity that exists between the value of assets and liabilities on which interest rates change during any specified period. In this case, the GAP analysis facilitates the assessment of IRR through an asset-liability management approach (Van Deventer, Imai, & Mesler, 2013). The simplicity of the measurement approach reveals the variation between assets and liabilities sensitive to interest rate instability over a particular time span.

According to Beets (2004), the use of financial derivatives is one of the recent methods of measuring and managing IRR in the banking sector. Particularly, financial derivatives infer to instruments that derive their value from one or multiple underlying financial assets (Chance & Brooks, 2015). The underlying instruments may be in the form of a securities index, financial security, or the integration of securities and indices, as well as commodities (Hull & Basu, 2016). Notably, they appear in various forms, including options, futures, forwards, and swaps.

Advantages and Disadvantages of GAP and Financial Derivatives

According to Hull and Basu (2016), the traditional GAP analysis IRR measurement approach is advantageous since it helps banks to compare the current or actual performance of the net interest income with the desired performance. Therefore, in line with Sharifi et al.’s (2014) findings, an asset-sensitive “gap” denotes that the bank’s assets surpass the liabilities in a particular time span. This finding indicates the positive performance of the financial institution’s net interest income. On the other hand, Koch and MacDonald (2014) assert that the identification of a liability-sensitive “gap” indicates that a financial organization may realize undesired net interest returns.

However, the GAP analysis is disadvantageous since it disregards variations in spreads concerning interest charges, which may result from market fluctuations. Additionally, according to Van Deventer et al. (2013), the IRR measurement method fails to consider the optionality aspect of assets, as well as liabilities. Moreover, the repricing assumptions subjected to non-maturity deposits undermine the reliability of this IRR management method.

Forward contracts represent binding agreements between parties that settle to purchase or sell government security, a given amount of a commodity, or foreign currency in addition to other financial instruments at a specified price whereby delivery and settlement are anticipated at a particular time (Chance & Brooks, 2015). Futures contracts denote similar characteristics with forwards, although this category is advantageous since it subjects parties in agreement to less risk compared to the former by including an intermediary. Interest rate swaps combine futures rate agreements (FRAs) to enable counterparties in agreement to exchange the collection of future cash flows (Saunders, 2014).

Options provide underlying security in the form of a debt obligation to facilitate interest rate management (Bingham & Kiesel, 2013). Options also offer counterparties with protection from the floating-rate loan, thus mitigating the adverse effects of interest rate fluctuations. The mentioned financial derivatives assist banks to measure and manage IRR through hedging (Bingham & Kiesel, 2013). Such derivatives may be applied in different situations to ensure that financial institutions realize desirable earnings, as well as the economic value of their instruments (Hull & Basu, 2016). Nonetheless, they (financial derivatives) are disadvantageous since they require banks to pay money or premiums to use the instruments to foster the measurement and management of IRR.

Conclusion

IRR is a major issue that has is threatening the operations of present-day banking systems, owing to the unprecedented volatile nature of market interest rates. The sources of interest rate fluctuations range from the repricing of liabilities, assets, and OBS to the optionality of financial instruments. Consequently, IRR affects financial institutions’ accrual earnings and their economic worth. This situation denotes the impact of interest rate volatility on the performance of industry players. In response, financial institutions apply methods such as the GAP analysis and derivatives to facilitate the measurement and management of IRR.

References

Alessandri, P., & Nelson, B. D. (2015). Simple banking: Profitability and the yield curve. Journal of Money, Credit and Banking, 47(1), 143-175.

Aspal, P. K., & Nazneen, A. (2014). An empirical analysis of capital adequacy in the Indian private sector banks. American Journal of Research Communication, 2(11), 28-42.

Basel Committee on Banking Supervision. (2004). Principles for the management and supervision of interest rate risk. Web.

Beets, S. (2004). The use of derivatives to manage interest rate risk in commercial banks. Investment Management and Financial Innovations, 2, 60-74.

Bessis, J. (2015). Risk management in banking. Hoboken, NJ: John Wiley & Sons.

Bingham, N. H., & Kiesel, R. (2013). Risk-neutral valuation: Pricing and hedging of financial derivatives. Berlin, Germany: Springer Science & Business Media.

Bloom, N. (2014). Fluctuations in uncertainty. Journal of Economic Perspectives, 28(2), 153-76.

Chance, D. M., & Brooks, R. (2015). Introduction to derivatives and risk management. Boston, MA: Cengage Learning.

Chan-Lau, J. A., Liu, E. X., & Schmittmann, J. M. (2015). Equity returns in the banking sector in the wake of the Great Recession and the European sovereign debt crisis. Journal of Financial Stability, 16, 164-172.

Esposito, L., Nobili, A., & Ropele, T. (2015). The management of interest rate risk during the crisis: Evidence from Italian banks. Journal of Banking & Finance, 59, 486-504.

Federal Housing Finance Agency. (2013). Interest rate risk management. Web.

Hull, J. C., & Basu, S. (2016). Options, futures, and other derivatives. New York, NY: Pearson Education.

Jiménez, G., Lopez, J. A., & Saurina, J. (2013). How does competition affect bank risk-taking? Journal of Financial Stability, 9(2), 185-195.

Jokipii, T., & Monnin, P. (2013). The impact of banking sector stability on the real economy. Journal of International Money and Finance, 32, 1-16.

Koch, T. W., & MacDonald, S. S. (2014). Bank management. Ontario, Canada: Nelson Education.

Saunders, A. (2014). Financial markets and institutions. New York, NY: McGraw-Hill Higher Education.

Sharifi, O., Saeidi, M., & Saeidi, H. (2014). Interest rate risk management using income and duration gap analysis in banks – An empirical study. Management Research Report, 2(7), 3058-3071.

Taiwo, O., & Adesola, O. A. (2013). Exchange rate volatility and bank performance in Nigeria. Asian Economic and Financial Review, 3(2), 178-185.

Van Deventer, D. R., Imai, K., & Mesler, M. (2013). Advanced financial risk management: Tools and techniques for integrated credit risk and interest rate risk management. Hoboken, NJ: John Wiley & Sons.