For this study, Abu Dhabi Islamic Bank has been chosen for analysis.

Supply, Demand, and Elasticity

Main Products &general characteristics of Abu Dhabi Islamic Bank

Abu Dhabi Islamic Bank (ADIB) carries out its operations in the National commercial bank’s sector. The bank is headquartered in the United Arab Emirates. The bank is a public listed company majoring in the provision of Sharia-compliant Islamic financial products, investment, and banking products and services. Throughout the country (United Arab Emirates), Abu Dhabi Islamic Bank has a total of 69 branch networks (AMEinfo: Abu Dhabi Islamic Bank posts record quarterly profit of Dhs319.1m, 2012, para. 5).

For this study, we will evaluate the Al Bateen main branch. The branch operates under five main business segments that are: the wholesale banking segment, which offers credit facilities and financial services current accounts and deposit accounts both for institutional and corporate customers, the retail segment offers commercial and consumer Ijara, Murabaha, funds transfer facilities, and Islamic covered card (AMEinfo: Abu Dhabi Islamic Bank posts record quarterly profit of Dhs319.1m, 2012, para. 5).

Also, trade facilities are provided under this segment. The third segment is the private banking segment, this segment provides credit and financing facilities, similarly, the segment offers current accounts and deposit-taking for individual affluent customers. The fourth segment is the real estate category, which majors in acquisition, development, selling, and leasing (Money Camel: Abu Dhabi Islamic bank -new car loans-AIDB car finance, 2012, para. 2).

The final category is the capital markets segment that undertakes treasury and trading services, a brokerage in the money market. The total revenues for the company registered in the 2010 fiscal year stood at AED 3074 million representing an increase of 22 percent from the 2009 figure. Net profit registered was AED 1024 million over the same period (Money Camel: Abu Dhabi Islamic bank -new car loans-AIDB car finance, 2012, para. 2).

Islamic covered cards and car finance product

The Islamic covered cards and the car finance product are two important products respectively that Abu Dhabi Islamic Bank offers (AMEinfo: Abu Dhabi Islamic Bank posts record quarterly profit of Dhs319.1m, 2012, para. 4).

Islamic cover cards

The cover cards are products offered by the bank to individuals seeking to be protected against financial emergencies. This product gives the customer unmatched convenience in accessing quick liquidity during emergencies. The bank was the pioneer in the issuance of Islamic cover cards (AMEinfo: Abu Dhabi Islamic Bank posts record quarterly profit of Dhs319.1m, 2012, para. 5). The cards are of two categories; a Gold card which combines both high coverage and competitive profit margins and a Platinum card with high limits of spending, lifestyle benefits, and high-profit rates.

The sales from Islamic cover cards increased from AED 98686, in 2009 to AED 158448 in 2010 representing an increase of 61 percent (Money Camel: Abu Dhabi Islamic bank -new car loans-AIDB car finance, 2012, para. 6). The selling rate thus increased by 60% between the two year periods. Generally, the selling rates among these financial institutions have a difference of less than AED 3 and stands at 17.5 percent and 20.1 percent for car loans and credit cards respectively. This translates into the selling price of 158448 for cover cards and AED 340,000 for a Murabaha vehicle loan.

Car finance (Vehicle Murabaha)

Over the last two years, the product has experienced a decline in its sales revenues. In 2009, sales from vehicle Murabaha generated a total of AED 8,022,334,000 while in 2010, the product registered total sales of AED 7,904,499,000 representing a decline of 1.5 percent (Money Camel: Abu Dhabi Islamic bank -new car loans-AIDB car finance, 2012, para. 9).

Analysis of the firm’s supply and demand

Product: Car Finance (Vehicle Murabaha)

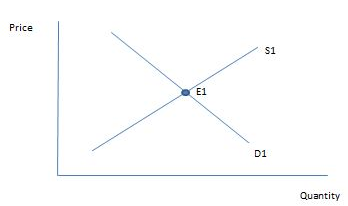

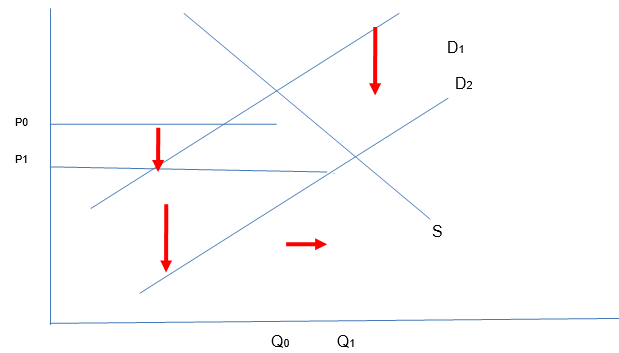

The Initial Demand and Supply chart

The initial equilibrium falls at E1. At this point, the initial demand and supply curves are assumed to be in a perfect relationship before market forces influence the nature of these curves (Dar & Presley, 2000). At E1, quantity demanded and that supplied are aligned perfectly to the prevailing market prices for that particular commodity. As indicated above, an increase in interest rates on car loans negatively affects demand.

Due to high interest payable on loans from banks, it will mean that repayment of loans will cost extra money. In response, customers will shy away from getting loans to buy cars. As a result, demand for car loans will decrease and this will automatically and negatively affect the relationship between demand and supply. However, at ceteris paribus, the opposite will create a positive relationship between demand and supply of car loans in the market since demands for car loans will increase when interest rates charged per loan has decreased. As a result, a potential customer will benefit from the ground of retaining more money during loan repayment (Dar & Presley, 2000, p. 6).

Factors Affecting the shape and behavior of Demand and Supply Curves

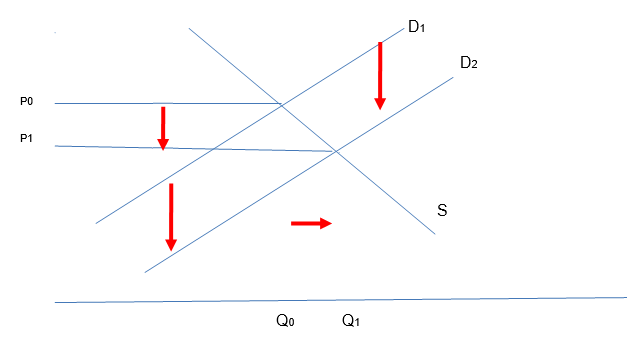

Consumers’ income

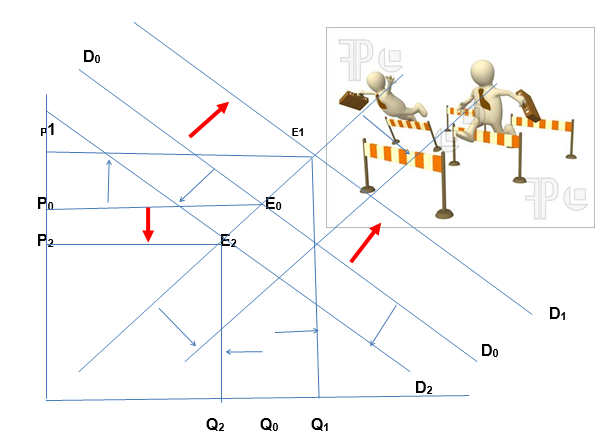

When a consumer’s income increases, the total disposable income increases. The consumers can afford to pay their interests on loans. For this reason, they demand more loan products from the bank. This leads to an outward shift in the demand curve for loans from D0 to D1 a new equilibrium is achieved at point E1 with price P1 and a higher quantity Q1.

Conversely, when income reduces, individuals’ disposable incomes reduce (Dar & Presley, 2000), given that cars are luxury goods, the demand for car finance declines, the quantity of car finance demanded from the bank drops from the initial quantity and the corresponding price falls from the initial P0 to P2. A new equilibrium is achieved at point E2.

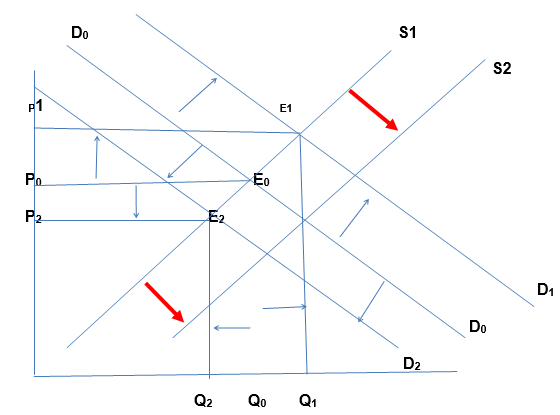

Prices of competing products/services

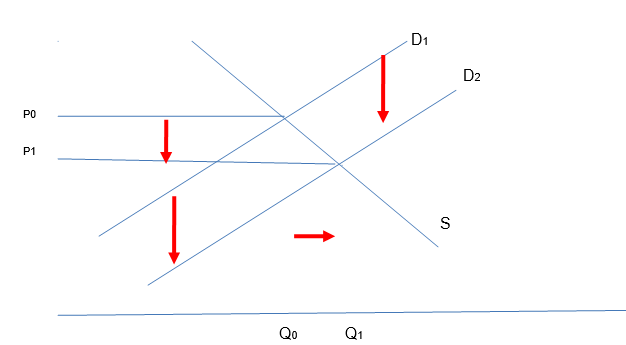

The car loan market in the UAE is significantly developed with many competitors and products to choose from. Given the stiff competition, ADIB faces a situation where consumers have more power in that they tend to select the best deals in the market. Currently, the bank offers car loans up to a maximum of AED 350,000 for new cars representing approximately 80 percent of the new car value. The loan amount is to be repaid within 4 years (48 months).

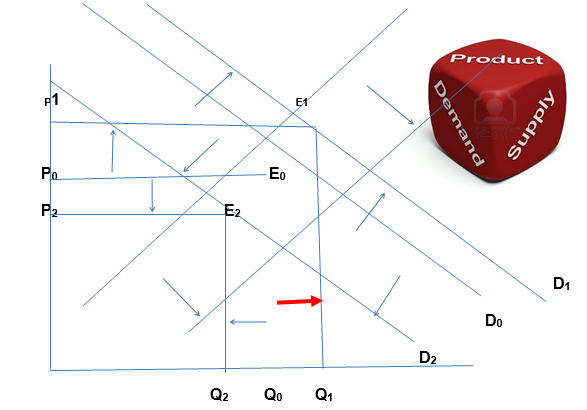

One percent of the loan amount is charged as a processing fee (ADIB Annual Report: Bank overview, mission, vision, and values ADIB, 2010, para. 4). The bank faces substitutes such as Auto finance offered by the Noor Islamic Bank, which also increases competition for the products offered y the bank. If the interest rates charged on Auto finance in Noor bank is reduced, then the demand for car loans offered by ADIB will decline represented by an inward shift in the demand for car loan products. On the other hand, if the price (interest) on the substitute product (Auto finance) is increased (Dar & Presley, 2000).

Customers will show more preference for Car loans offered by Abu Dhabi Islamic Bank. This will lead to an outward shift in the demand for car loan products offered by ADIB quantity demanded increases from Q0 to Q1 and a new equilibrium is attained at the point E1.

Number of consumers

The specific consumers that the ADIB targets with the Car Finance product are employees of Multinational Companies, Employees From Reputable Local Organizations, Private Universities, Airlines, Colleges, Schools, UN Bodies, International Aid Agencies, Government employees and Business Persons, Self-employed Professionals for instance Engineers, Doctors, Certified Accountants, Consultants and Architects (ADIB Annual Report: Bank overview, mission, vision and values ADIB, 2010, para. 5).

The loans are specifically meant for the purchase of new vehicles and reconditioned non registered cars. The loan amount is approximately 80 percent of the cars total value. The target populations are people between the ages of 30-55. Demographic changes that result in more people joining this age bracket will result in increased demand for car finance. The increased demand will push the demand curve outwards to the right from D0 to D1, the bank will be compelled to increase the quantity of car finance supplied to Q1 at an increased price P1.

A new equilibrium is attained at the point E1 with a higher price and a higher quantity supplied of the car loans. Conversely, if the demographic changes result in fewer people falling within these age brackets, we expect the demand for ADIB car finance to decline (ADIB Annual Report: Bank overview, mission, vision, and values ADIB, 2010, para. 9). This is reflected by a leftward shift of the demand curve from D0 to D2. The bank is forced to reduce the quantity supplied of the car loans from Q0 to Q2 and a lower price P2. A new equilibrium is attained at the point E2.

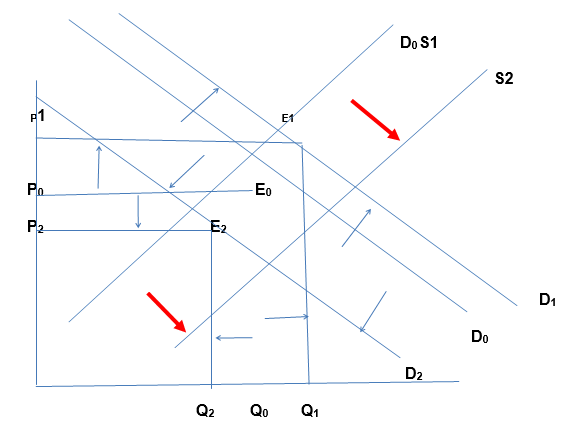

Technology

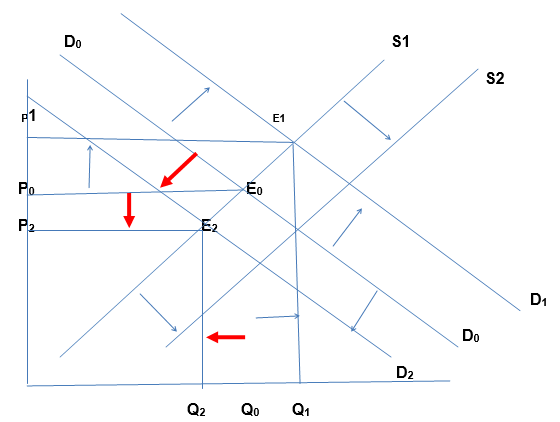

Technology is increasingly becoming an integral part of banking service delivery. An improvement in technology that results in increased deposit creation by the bank will make ‘loanable funds’ more available (Dar and Presley 2000). As a result, there will be more money available to lend under the car finance. The supply of car finance loans will shift outwards to the right from S1 to S2.

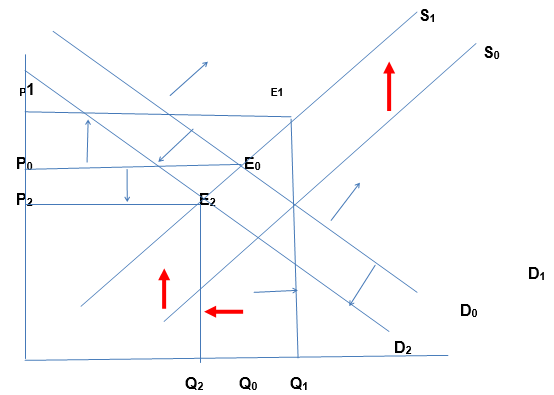

Number of competitors

Many competitors in the UAE banking industry compete for the same customers as ADIB. Also, the banks offer almost similar products with the only difference being the brand names. These banks include First Gulf Bank, Emirates Islamic Bank, National Bank Of Dubai, Commercial Bank International, Citibank, Emirates Bank International, Lloyds TSB bank among others. Given the fact that the industry already has a large number of players, the industry can be said to be operating under perfect competition.

For this reason, the entry or exit of a single firm will not affect the ADIBs supply of car finance (Dar and Presley 2000). However, if many firms join the industry, they are likely to take away ADIBs customers by offering low prices and interest rates on their products (ADIB Annual Report: Bank overview, mission, vision, and values ADIB, 2010, para. 6). This will lead to a decline in the demand for ADIB loans because the demand shifts inwards to the left.

Similarly, the exit of a single firm will leave ADIB bank lending unaffected. However, many firms exit from the industry; ADIB will acquire a substantial market share because of reduced competition (Money Camel: Abu Dhabi Islamic bank -new car loans-AIDB car finance, 2012, para. 5-6). This will be reflected in the form of increased lending with the supply curve shifting outwards to the right from S1 to S2

Costs of production

The major costs incurred in processing car finance loans are employee salaries, processing fees, and the costs incurred in situations of bad debts and debt collection (Dar and Presley 2000). The costs are critical in determining the profitability of an organization. When the cost of production increases, it means that the price charged for the final product will increase. The increase in the cost of production will make the supply curve to shift to the left; the quantity supplied will decrease as the cost of materials for production increases. However, in a monopolistic market, this may not be the case since the producer may have complete control of the final price tag of a product. In this case, the relationship between the cost of production and supply are inversely proportional. As a result, the quantity will crease from Q0 TO Q1 as the supply curve shift from so to S1. This is shown in the figure below.

Other non-price determinants (if applicable)

Other non-price determinants equally affect the demand for car finance. These include religion. Islam as a religion prohibits the setting of fixed interest rates on loans (riba) neither are the banks allowed to levy interest on their loans. For this reason, charging interest on loan products like car finance in a Muslim country affects the demand for the product (Money Camel: Abu Dhabi Islamic bank -new car loans-AIDB car finance, 2012, para. 8). Other non-price determinants include variations in consumer preferences and tastes, demographic changes, and changes in the prices of substitutes and compliments (Dar and Presley 2000).

Analysis of the Price Elasticity of Demand for one of the products

The price elasticity of demand (PED) for (product/service) as a proportion of income

Price elasticity refers to the degree of responsiveness of the quantity demanded of a product to changes in price. The price elasticity of demand for loan products has significant implications for the overall performance of the bank. Consumer price elasticity determines the firms pricing policy more specifically if it commands some market power. Borrowers often face several incentives that compel them to repay their loans.

According to Dar and Presley (2000), “It can be argued that goods that account for a large proportion of disposable income tend to be elastic. This is due to consumers being more aware of small changes in the price of expensive goods compared to small changes in the price of inexpensive goods” (p. 8). These include; the possibility of increased future loans if they exhibit a good credit history. This affects the price elasticity of demand for the bank’s loan products since more incentives motivate clients to repay their loans.

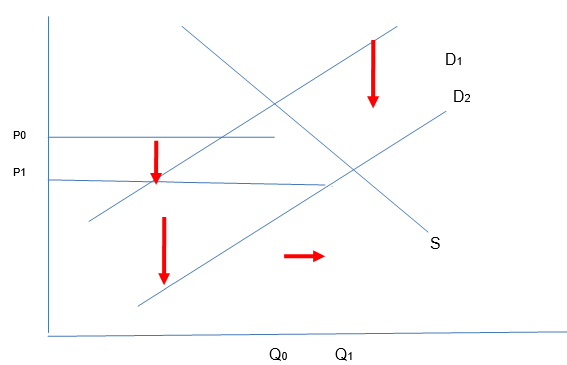

Price elasticity of demand diagram as a proportion of income

Loan products are very responsive to price changes, for this reason, they are said to be price elastic. A small price change (P0-P1) leads to a greater change in quantity demanded (Q0-Q1).

Number of Substitutes

When there are more substitutes besides a product, chances of shifting to these substitutes are higher. Specifically, the shift can be necessitated by an increase in the price of that product when the substitute remains relatively cheaper or of better quality. Therefore, the availability of a substitute may lead to a decrease in demand when the price for a product increases. When the price increases, the household might opt for the best alternative especially when doing the same will positively affect savings or add value to the disposable income (Dar and Presley 2000).

Therefore, the several available substitutes, in this case, will make the demand curve to be highly elastic as responsiveness to changes in the price of the same attracts immediate change in customer behavior such as purchasing pattern. A small price change (P0-P1) leads to a greater change in quantity demanded (Q0-Q1) as customers will opt for substitutes that have a cheaper price tag or are more affordable in long run.

Degree of necessity

The degree of necessity depends on the nature of a product meant for a household. Reflectively, products that are basic and necessary in the daily lives of a household will not affect the demand curve very much despite the increase in the price of such a product. The household has no option but to continue consuming or using the product as it is basic. However, in this case, cars are considered a luxury and not easily affordable by households. Therefore, an increase in the price of such a product will lower the demand (Dar and Presley 2000). A small price change (P0-P1) leads to a greater change in quantity demanded (Q0-Q1) as customers will opt to wait and do the purchasing when prices are lower since the product is but a luxury in the product market as opposed to necessities.

Price of the good as a proportion to income level

Disposable income levels determine the behavior of the demand curve for necessity and luxury goods. “Goods that account for a large proportion of disposable income tend to be elastic. This is due to consumers being more aware of small changes in the price of expensive goods compared to small changes in the price of inexpensive goods”( Dar and Presley, 2000, p.9). In the demand for vehicles, the demand curve can be described as elastic since the product have several substitutes making customers respond almost immediately whenever there is a change in the price of the same.

Besides, it is not a necessity and thus customers can do without it or opt for cheaper alternatives of acquiring the same rather than from bank loans. Since this product requires heavy encroachment into the disposable income and contributes to a greater percentage of the total amount of expenditure, the demand curve for the same is more elastic.

A small price change (P0-P1) leads to a greater change in quantity demanded (Q0-Q1) as customers will opt to keep away from purchasing the product since it will eat further into the disposable income, This is because motor cars require a commitment of a greater percentage of the disposable income and account for a better part of the total expenditure against other competing needs.

References

ADIB: Business covered cards. (2012). Web.

ADIB Annual Report: Bank overview, mission, vision and values ADIB. (2010). Web.

AMEinfo: Abu Dhabi Islamic Bank posts record quarterly profit of Dhs319.1m. (2012). Web.

Dar, H., & Presley, J. (2000). Lack of profit loss sharing in Islamic banking: Management and control imbalances. International Journal of Islamic Financial Services, 2 (2), 1-10.

Money Camel: Abu Dhabi Islamic bank -new car loans-AIDB car finance. (2012). Web.