Acquisition Situation

Contractual negotiations on the matters of supplying H-19C helicopter systems, as well as enhancing the computer program development, is one of the key steps in H-19 Helicopter Program development, as this will help to define the general aspects of the program as well as help to outline the cost and financial strategy of the program. Additionally, as this is closely related to the contractors involved, the DCAA, and the overview terms of the Government’s position, the success of the program will define the patterns of further cooperation and development.

Cost Analysis Summary

The H-19 model is used by the U.S. Navy, Marines, Air Force, Coast Guard (rescue mission), and the Department of Interior (fire fighting mission). H-19’s are widely used to support deployed U.S. military peacekeeping forces throughout the world. The universal nature of the model created the necessity to create specifications that involve modifications of avionics, navigation systems, radio navigation and communication, computers, etc. The key costs of the project are offered in figure 1

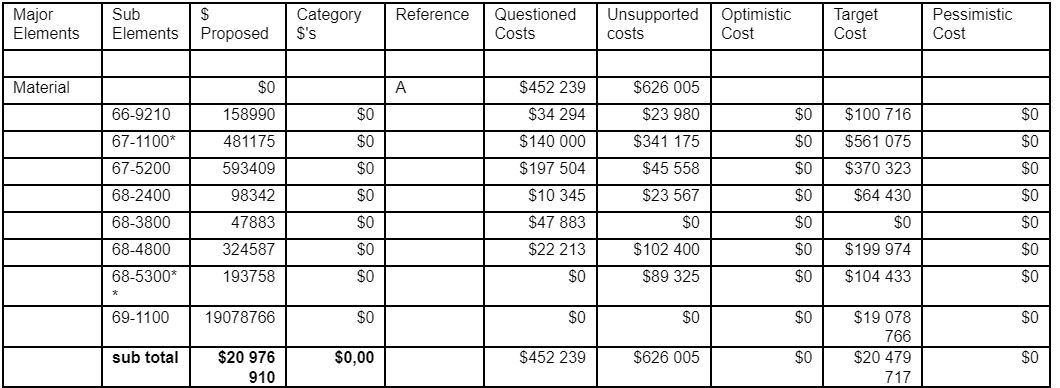

Material Costs

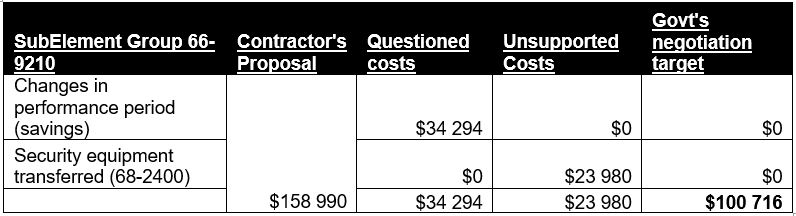

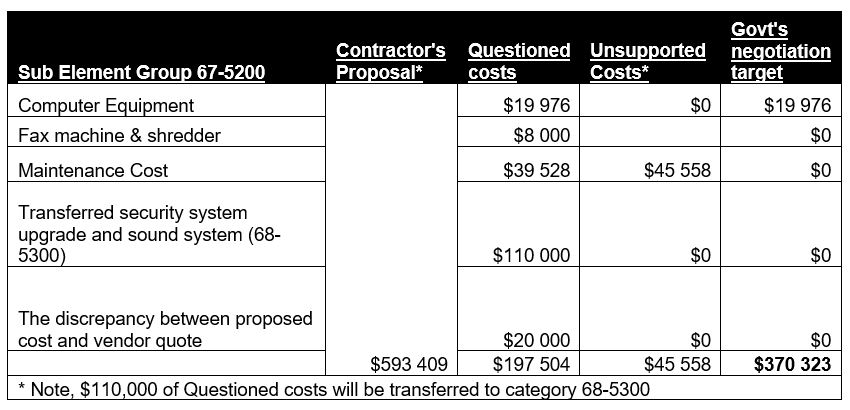

In general, the costs offered, as well as the pricing data are quite adequate for the basis of the negotiation purposes. Though, It should be stated that the prices and costs that are provided by the offeror on the matters of support and materials do not correspond with the Cost Accounting Standards. The justification of the costs is closely associated with the aspects of specifications of the equipment used for manufacturing H-19C, and the specified models for various aims. The costs that are offered in Figure 2 represent the costs that are associated with the changes in the manufacturing performance for creating another modification of the H-19C. Because the proposal itself involves both aspects of the costs, including changes and security equipment transfer, the government’s negotiations target is to exclude these costs from the final investment sum. This is explained by the fact that the contractor undertakes all the required costs by itself, while the customer needs to get the final product. Additionally, the three-month reduction in the performance period should result in savings in computer and test equipment rental time and maintenance.

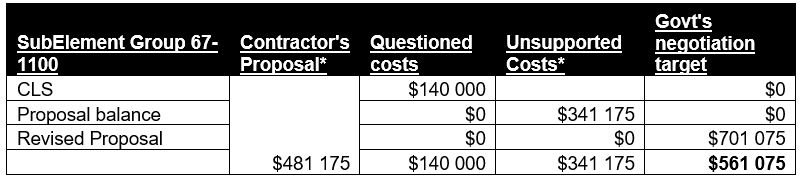

The reduction of cartridge lead software is the key requirement for lowering the service costs of the entire system. The lowering of the price is based on the corrected quote of the service works, and the unsupported costs are the adequate alternative for assessing the developmental needs for the

Figure 4 represents the costs and values of the equipment required for the performance of the contractual obligations. Hence, the maintenance costs may be decreased if Fax machine & shredder are removed from the cost spreadsheet. This is explained by the statement that these discrepancies between the proposed cost and vendor quote provide an adequate image of the maintenance costs, consequently, the unsupported costs associated with maintenance may be removed from the contractual obligations. $39,528 of the ADPE was questioned as to the required maintenance cost due to the required decrease in maintenance. Furthermore, the maintenance requirements had been scaled down.

The values of decrement factors are not the proper justification of the costs, however, it should be emphasized that the unsupported costs are included in a single basis of decrement factors. Hence, the sample of 15 parts is the construction basis of the modification which is historically defined. Hence, it should be stated that Malahy Aero Systems disagreed stating that their proposal is based on sampling 50% of the parts and applying the decrement factor accordingly, hence, the questioned costs are based on the traditional approach linked with the negotiation target.

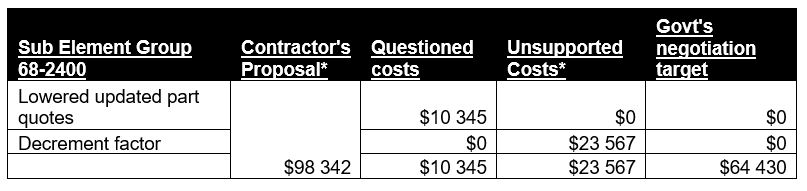

Figure 6 The maintenance and MX costs are closely linked with the proper service of the contracted helicopter modification, as the traditional aspect of the agreement is closely linked with the values of the unsupported costs linked with documentation requirements. The proposal was submitted before the receiving of the vendor quotes, hence, the $ 102 400 is required for unsupported costs, as some maintenance costs are not specified in this sector.

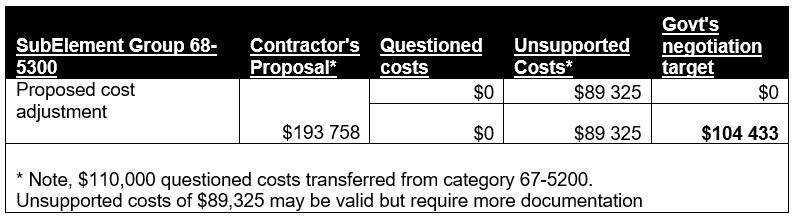

In general, the proposed cost was based on test equipment required before the BRU-55 wiring modification and the video upgrades. Hence, the justification of the costs is closely associated with the values of the negotiation target.

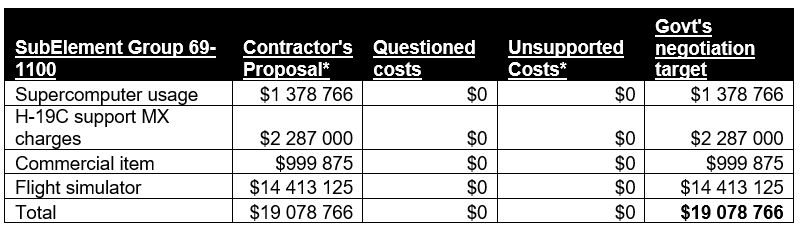

No exceptions are offered concerning the costs associated with super-computer usage. The maintenance charges are linked with the aspects of the complexity of the technology employed, though, the commercial item of part 12 involves flight simulator system testing and training, which requires up to $14,413,125

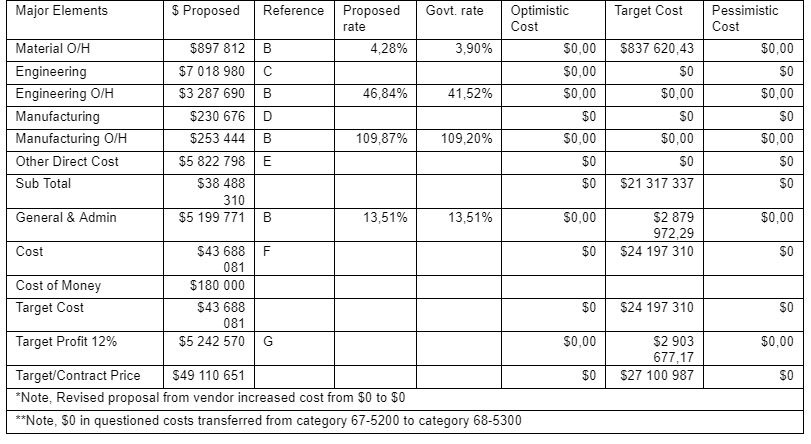

Overhead and G & A

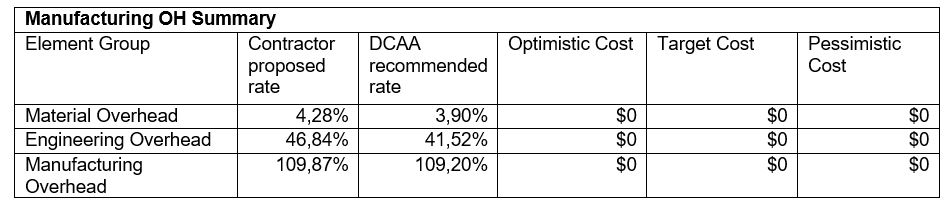

Material Overhead

The general value associated with materials is linked with the necessity to provide the forecasted sales rate. As the recommendation of a 3.9% rate was offered by ACO, it should be stated that the rate is quite adequate. The target cost of $837 620.43 is justified by the necessity to perform the timely supply of materials. Some materials need to be processed before applying them for the project, hence, the overhead rate will compensate these costs.

Engineering Overhead

This rate is justified by the necessity to arrange proper and coordinated engineers’ teamwork. Moreover, the changes in the labor principles will inevitably affect the productivity of the team, hence, the engineers will require additional compensation, especially because some had been working on the other projects, and would have to restructure their schedule for adapting for the new one.

Manufacturing Overhead

The standard overhead for similar projects is close to 109%. Considering the particularities of the order, and the necessity to create a unique product, the adequate rate may be increased in comparison with the standard values. As for the offered rate of 109.87%, it should be emphasized that the performer will have to restructure the manufacturing process, as it will involve the implementation of additional technologies, and qualification improvement of the personnel.

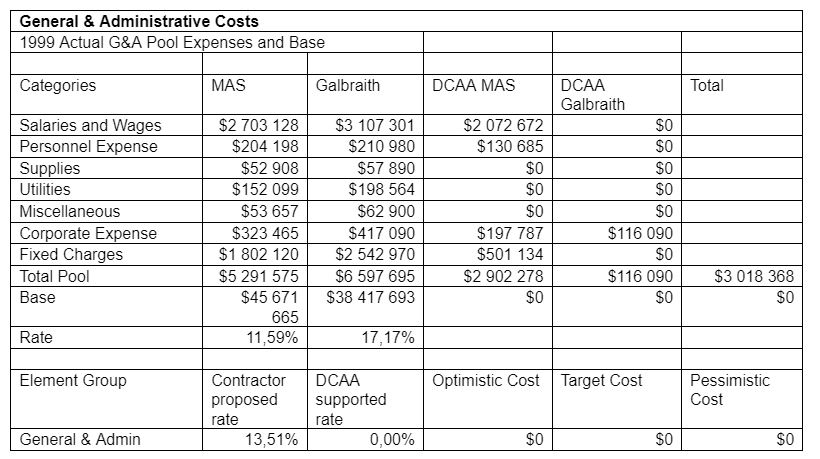

General and Administrative Costs

The administrative costs are the key aspect of the work coordination and management, hence, the values of these costs should not b underestimated. Expenses and charges associated with supplies, utilities, wages, etc., are inevitable for such a large-scale project; as for the adequacy of the rates, these are close to standards, however, the actual importance of these rates is justified by the insurance and guarantee necessities.

DCAA Concerns

The executive staff wages of $630,456 of the Malahy Aero Systems material center are unsupported. Since Whitty Global Material Centre is heading up the new organization, there is no need for the Material Vice Presidents at Malahy Aero Systems. The justifications of these rates are close to the fact that the general costs of the administration are as high as the administration’s professionalism level, nevertheless, effective management presupposes lesser costs.

Galbraith Executive Salaries and Wages

Both salaries ($840,615 and $555,615) exceed the compensation benchmark set forth by the Office of Federal Procurement Policy (OFPP), hence, they may be decreased, however, OFPP needs to consider that this rate is defined by the marketing environment and project requirements. The decrease of the rate will inevitably cause the violation of the marketing position of the company and a further decrease in performance effectiveness.

Miscellaneous and Corporate Expenses

The miscellaneous point of the expense plan presupposes the required operational expenses that may be associated with classified technology or components usage. Managing these technologies may require additional expenses and costs. Legal aspects of the cooperation are also included in this line.

Corporate expenses for Malahy and Galbraith the capital consolidation and leasing control of these participants will provide additional effectiveness levels of the companies.

Fixed Charges

$1,300,986 in depreciation costs are unsupported, hence, the actual importance of this expense point is inevitable for performing all the necessary supplies and preparations for the manufacturing process.

Engineering Labor

FY00 35,900 hrs x $35.72/hr = $1,282,348

FY01 140,250 hrs x $35.72/hr = $5,009,730

FY02 20,350 hrs x $35.72/hr = $726,902

Total Engineering Labor = $7,018,980

The rate is a composite across engineering labor categories and the period of performance.

The DCAA auditor considers all engineering labor costs as unsupported due to unsupported labor rates. The contractor has submitted a new forward pricing rate proposal for engineering labor to the ACO. The auditor considers the forward pricing rate proposal inadequate and requests supporting information. No forward pricing rate agreement currently exists for engineering labor. To arrive at a reasonable engineering labor hour estimate, it was determined that regression analysis would be used to determine if there is a historically legitimate relationship between function points and engineering hours. This analysis was performed and it was determined that there does appear to be a legitimate correlation between function points and engineering hours. The historical information is identified below:

Function Points* Engineering Hours

FY95 Mission Computer Upgrade 15 74,395 hrs

FY96 Mission Computer Upgrade 20 98,996 hrs

FY97 Mission Computer Upgrade 40 194,000 hrs

FY98 Mission Computer Upgrade 10 49,000 hrs

Estimated Functional points for upgrade 38 184,741 hrs

*Estimating using function points is an alternative to estimating using lines of computer code. Examples of function points include sending information, receiving information, and execution of a command.

The contractor’s proposal estimates the effort will require 184 741 hours. The Regression Analysis calculations indicate that the effort will require 416 391 hours. The regression analysis calculations also indicate that with a 90% confidence level the engineering hours will fall within the range of 120 264 to 200 033 hours. For negotiations and calculating award fees, it is the cost/price analysts recommendation that the low range (1 789 036 hours) be used as the optimistic cost, the calculated value arrived at through regression analysis (740 069 hours) be used as the target cost and the high range number of the 90% confidence level (499 343 hours) be used as the pessimistic cost. Although a forward price rate agreement has not been established, the contractor’s proposed rate of $35.72 will be used as a placeholder until a rate can be negotiated.

Engineering Labor Analysis

Manufacturing Labor

The costs of the labor are closely linked with the contractual obligations of the company with the workers and engineers. They get their salaries for their qualification and efforts, and, because the manufacturing process is not disclosed, labor costs also include non-disclosure fees.

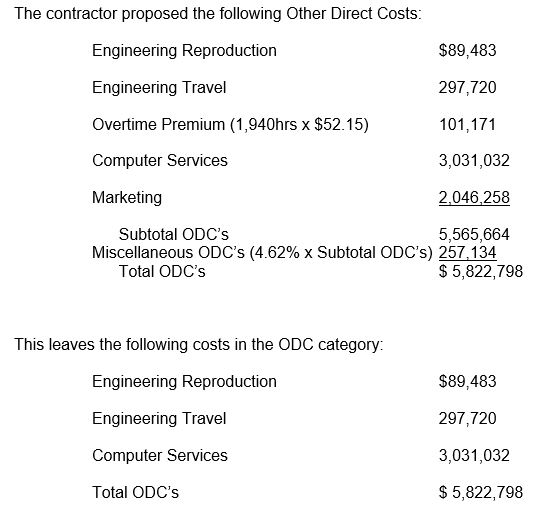

Other Direct Costs

Cost of Money

For this case, $180,000 will be used for the contractor proposal and Government objective.

Profit

The target profit is 12%. In general, this is the valued sum, and, considering similar projects it is quite adequate. It is justified by the necessity to invest in further company’s development.

Target Price

$27 100 987. This number is originated from the amount of all the costs and expenses that are inevitable for the project. Because the actual importance of the total price is defined by the success of the project performance, the adequate price is the crucial point of the contract.