Introduction

Gazprom is a global gas exporter producing 15% of the world’s natural gas. The Russians’ Federation owns 50.002% of the company’s shares. The company’s liquefied natural gas (LNG) sales “between 2005 and 2011 was 6.3 million tons in total” (Gazprom Today, para. 6). Apart from gas, the company produces electricity. In Russia, it accounts for 17% of electricity production. By the end of 2010, it was producing 36 GW. In 2011, “Gazprom Group sold 503.6 billion cubic meters of gas” (Gazprom: Marketing para. 1).

This included 156.6 B in Europe, 265.3 B in Russia, 81.7 B in CIS & Baltic states, and 3.06 B in America & Asia-Pacific (Gazprom: Marketing). At the end of 2012, 1,000 cubic meters of gas was priced at 319 Euros ($429.40) (Russian Natural Gas Monthly Price – Euro per Thousands of cubic meters”). This can be used to estimate the value of its reserves and inventory.

Financial Analysis

Share prices

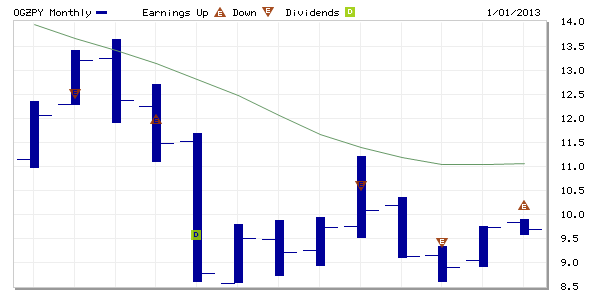

The Gazprom share price closed at $9.70 on 25 Jan, 2013. The highest price for the day was $9.75 and the lowest price was $9.66. The average of low prices during the last 52 weeks is $8.57. The average of high prices during the same period is $13.63. The average volume of shares traded is 791,330 under OGZPY. However, under “GAZP.ME” the volume of shares traded is 22,497,380 for a closing price of RUB 146.40 (GAZPROM: GAZP.ME – MCX). According to Gazprom website, the total initial number of shares issued was 23,673,512,900. The value of each share in RUB was 5.0. The total value of shares issued was RUB 118,367,564,500 (Gazprom: Shares). Today, the book value of each share is RUB 349.

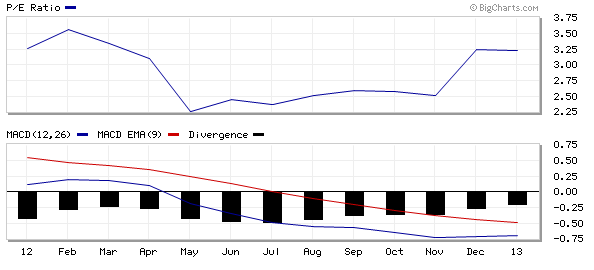

The company’s market capitalization of shares through OGZPY is at $115.11B. Seyhun (2000) discusses that P/E is obtained from “dividing the closing stock price by the annual earnings per share” (p. 215). The P/E ratio is 2.87. A low P/E ratio may indicate low rating by investors or the company is reinvesting. According to Brigham & Houston (2009), the P/E ratio indicates the amount “investors are willing to pay per dollar of invested earnings” (p. 98).

They discuss that a high P/E ratio shows that a firm has broad growth opportunities. The P/E ratio (ttm) on Yahoo finance indicates a different value. Gazprom has a P/E ratio of 1188.99. It is the market leader in the integrated oil & gas industry. This can be compared to Exxon Mobil’s 121.40 and BP’s 507.82 (Industry Center – major Integrated Oil & Gas 2013). Gazprom is the investors’ favorite.

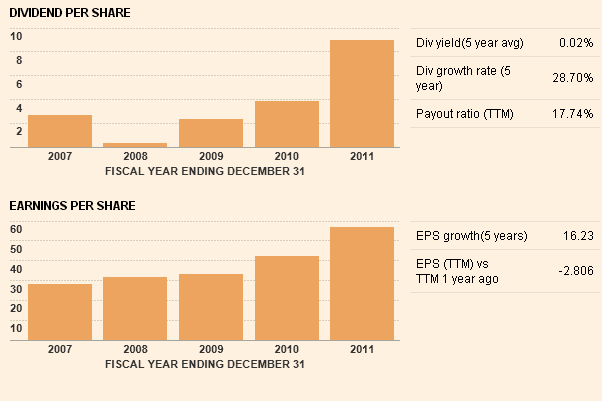

Revenue per employee stands at $377,683. Earnings per share (EPS) are at $3.38. Dividend issued per share on 8 May, 2012 is 0.56. Dividend yield is 5.77% (Market Watch, 2013). Dividend yield expresses the amount paid as dividends as a percentage of the share price. In short, dividend yield = annual dividends per share/ price per share (Dividend Yield 2013). The EPS share is expected to reduce in the next financial year to $3.00. Last year it was $3.49 which shows a decline to the present $3.24. The trend is expected to continue (see appendix 2). It also indicates that P/E ratio has stabilized.

Actual capitalization

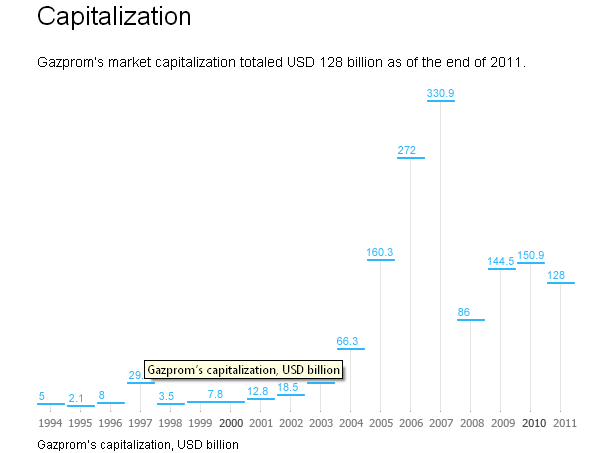

Capitalization is the net worth of a company. Bose (2006) discusses that capitalization can be obtained from the value of profits multiplied with the industry’s rate of return. It can also be obtained from the “aggregate value of shares, debentures and non-divisible retained earnings of the company” (p. 45). According to the balance sheet in Market Watch (2013), total liabilities & shareholders’ equity stood at RUB10.9T in 2011 and RUB9.24T in 2010. Goodwill was valued at RUB3.2B in 2011 and no values for previous years. The actual capitalization using total number of shares is 2,296,633,075,130 (23,673,512,900 * $ 9.7). In simple terms, this is approximately $2.3T.

Profitability

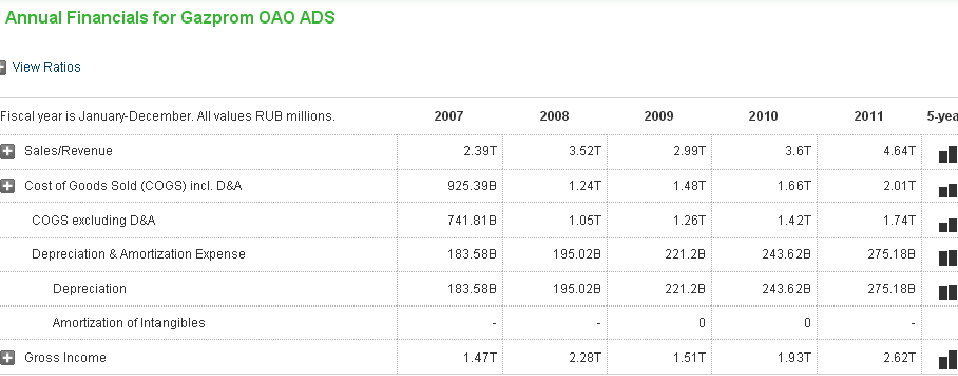

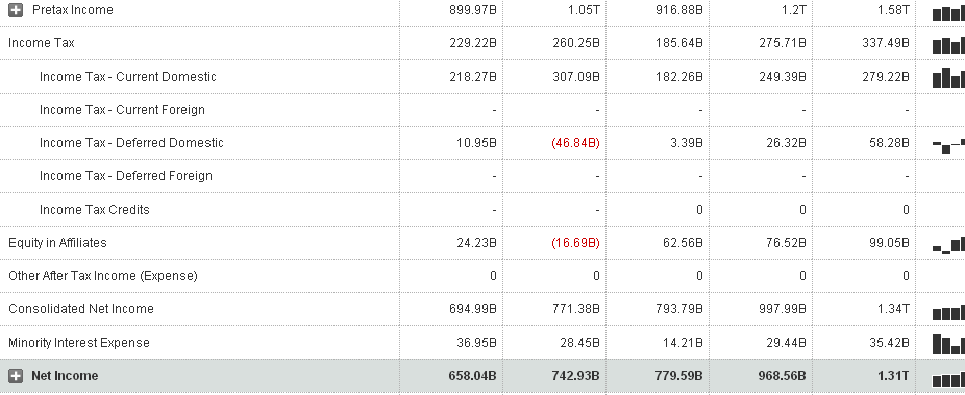

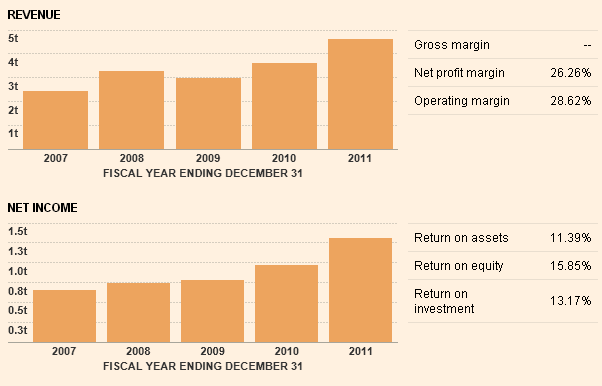

The returns to capital indicate Gazprom is a profitable company. According to Financial Times, “Gazprom OAO’s revenues went up by 28.77% from RUB 3.60T to 4.64T” (Gazprom OAO). Net income increased by 34.94%. In nominal values, it moved from RUB 968.56B to RUB1.31T. The net profit margin is at 26.26% and an operating margin of 28.62%. The company’s return on assets is at 11.39% and return on equity is at 15.58%. Return on investment is at 13.17%.

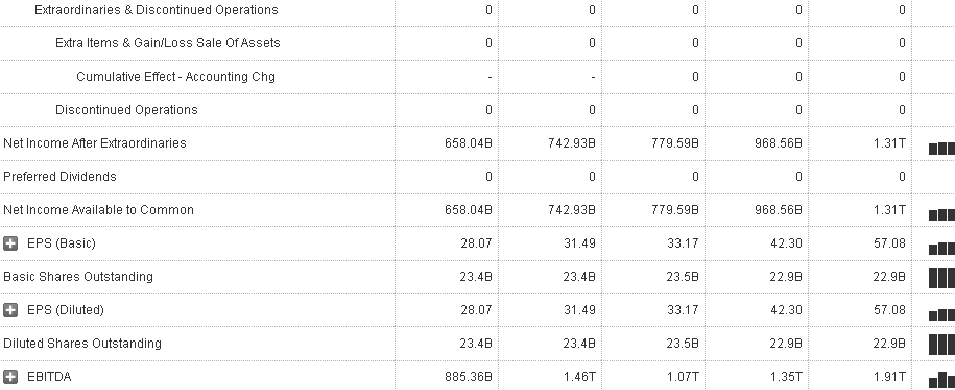

Earnings per share grew by 34.94% and dividends per share grew by 132.99% (Gazprom OAO “Financial Times”). The high growth in dividends may be as a result of returns coming from previous business expansion. Dividends per share have been increasing in the five year period (see appendix 4). It can explain the reason it has the highest P/E (ttm) in the oil & gas industry. Investors consider it as a good investment.

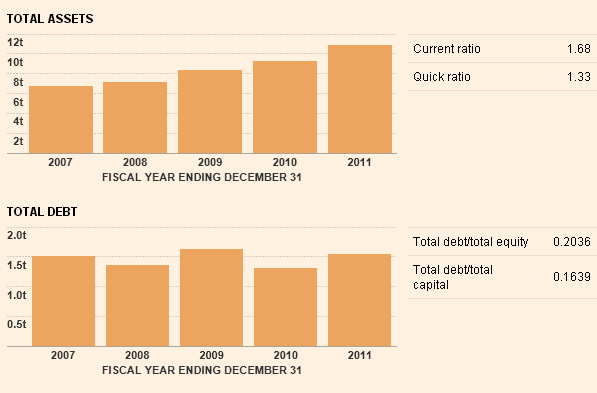

The company has the ability to repay liabilities. According to Financial Times (2013), “Gazprom has a debt to total capital ratio of 16.39%” (Gazprom OAO). A current ratio of 1.68 and a quick ratio of 1.33 (see appendix 6). Current ratio is obtained by dividing current assets by current liabilities. It indicates the firm’s ability to pay its debts within a year. The quick ratio eliminates the value of inventory which is considered less liquid than other assets. Cash flow per share is RUB 67.95 and share price divided by cash flow per share is 2.23.

The book value per share is RUB 349.42 (Gazprom OAO “Financial Times”). The book value per share indicates the amount that would be paid per share to shareholders if the firm was to be liquidated (Book Value per Common Share “Investopedia”). This is after paying all debts. The book value per share makes its stock to be considered as safe investment.

Threats

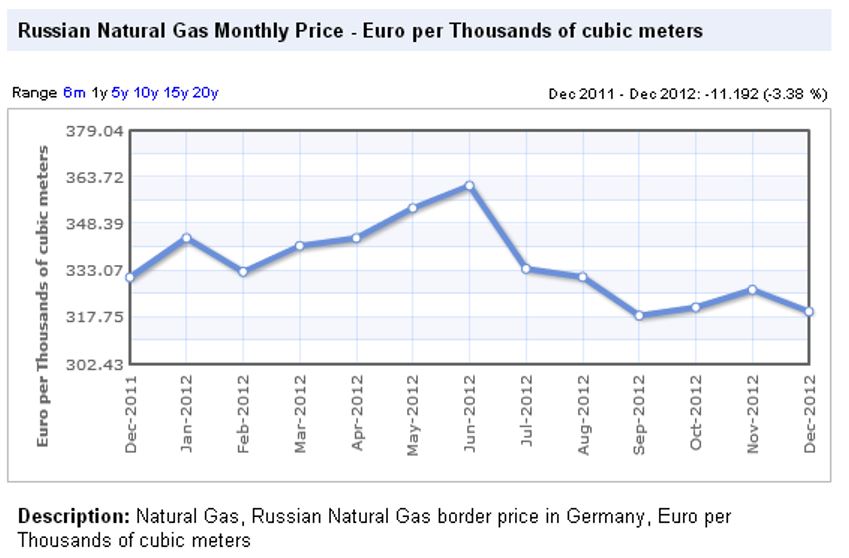

Ukraine, one of the importers, has signed a deal with Royal Dutch Shell to explore local gas reserves aimed at reducing importation. According to Neely (26 Jan, 2013) Ukraine was “committed to import 42 billion cubic meters (bcm) of gas through Naftogaz in 2012” (para. 16). This is a big volume that can reduce revenues by a big margin. In 2012, it imported 33 bcm from Russia’s Gazprom. Ukraine considers $439 per 1,000 cubic meters to be higher than market prices. From the graph below the prices in Europe are 317.75 Euros ($427.71) per 1,000cubic meters. Ukraine’s reserves, estimated at 1.2 trillion cubic meters, could turn into a competitive force.

A graph indicating the prices of natural gas in Europe retrieved from Index Mundi.

Rosneft is taking over TNK-BP. It plans to invest $7 billion to increase gas production in Russia (Marson 21 Jan, 2013). This is still a small portion of investment compared to what Gazprom invests annually.

Research and development

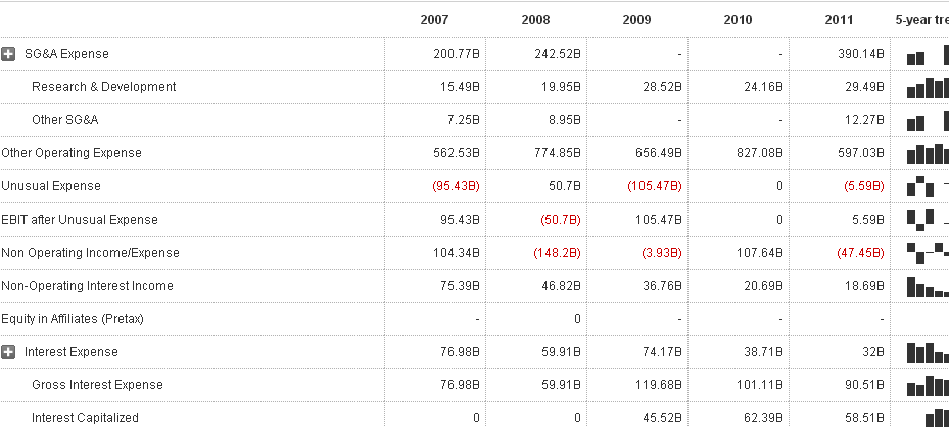

Gazprom spent RUB28.52B in 2009, RUB24.16B in 2010, and RUB24.94B in 2011 towards research and development (see appendix 1). This ensures that it uses the most efficient methods of extraction, production, and supply. It also seeks methods that are conservative to the environment.

Gazprom has been spending billions of dollars in expansion of gas fields and distribution over the years. Marson (20 Dec, 2013) reports that “Gazprom board of directors approved a cut in investment from RUB 974.6B to RUB 705.4B ($22.9B)” (Market Watch “Gazprom’s board approves 2013 investment reduction”). It is a small reduction which means the firm will still expand its operations to new areas.

Gazprom relies mainly on its reserves and fixed assets. Gazprom owns 51% stake at Nord Stream, “the consortium that operates natural gas pipelines that ship gas to western Europe” (Marson 8 Oct, 2012 “Market Watch”). The company is owned partly by foreign companies such as BASF SE’s Wintershall, and French’s GDF Suez SA among others. The company plans to build two additional lines to increase pumping capacity to four times 27.5 billion cubic meters (bcm) annually. The company owns two parallel lines that are 1,220km long. Each has a capacity of pumping 27.5 bcm annually.

Gazprom has signed a deal that will see it acquire 50% of the German’s BASF SE subsidiary company, Wintershall. BASF SE will also hand over assets that had revenues of about $10.9B in 2011. In return, Gazprom will allow BASF SE 25% of its new gas exploration projects in Siberia estimated at 274 billion cubic meters (Market Watch). Consolidation will reduce competitive forces, and make the company more profitable.

Quantitative assumptions

The Yamal project launched jointly with Novatek is considered to have 22tcm (trillion cubic meters) in reserves. It is expected to produce up to 360bcm by 2030. By the end of 2010, the company’s reserves of gas and oil had reached 33.1tcm and 2.98 billion tons respectively. In the Eastern Russia gas project, Gazprom is expected to produce 7tcm by 2030. It has stakes in the production of gas in more than ten other countries such as Algeria, and Vietnam (Gazprom: Fields). Considering the two major reserves’ production up to 2030, totals 7.36tcm (7tcm + 360 bcm). Assuming the standard discounting factor for oil reserves is 10%.

From January 2013 to the end of 2030 can be considered to be 18 years. The discounting factor is 0.1799 (Table 2: Discounting Factors @ 1% to 10% “Department of Finance and Personnel”). From calculations, the NPV of these two reserves can be estimated at $0.569T (0.1799 * 7.36 tcm * $429.40/1,000). This is $569B, the NPV in only two of its production reserves. The value is about 25% of the value of shares obtained by multiplying the share price by number of shares $2.3T (23,673,512,900 * $ 9.7).

Gazprom forecast includes producing 640 to 660 bcm annually from 2020 onwards (Gazprom). Considering 2020 is eight years from Jan 2013, this has a NPV of $128.20B (0.4665 * 640bcm * $429.40/1,000), and $116.55B in 2021 (0.4241 * 640bcm * $429.40/1,000). In total, between 2020 and 2030, Gazprom is expected to generate an NPV of $787.76B (from annuity tables (8.2014 – 5.3349) * 640 * $429.40/1,000)). This is a third of the capitalized value $2.3T. Out of this, 26.26% is likely to be profit and 15.58% to be returns on equity. It also indicates that Gazprom has the ability to generate more in revenues than its capitalization value in the next 20 years.

Competitor analysis

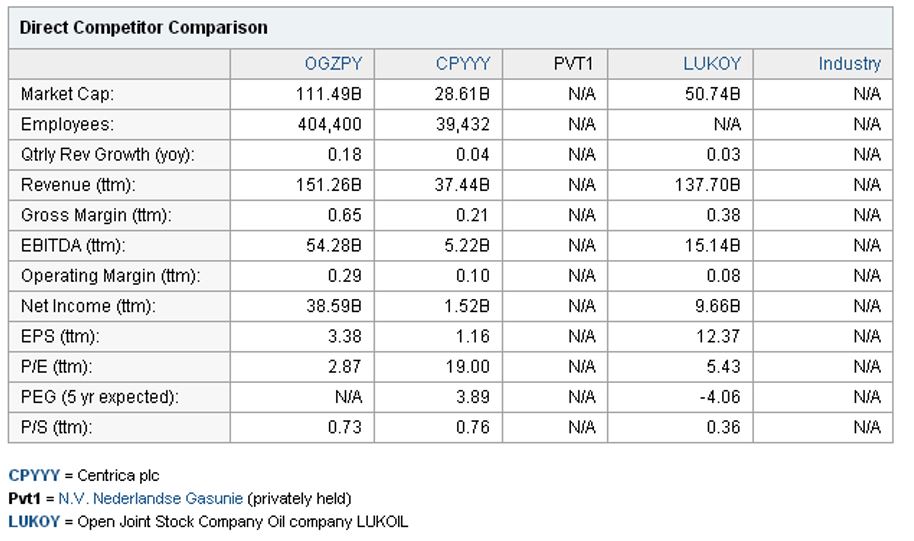

Gazprom supplies gas in North America, Europe, and Asia. Centrica is a company that supplies gas and electricity in the UK, North America, and other parts of Europe. Lukoil holds 16.6% of oil produced in Russia. Its revenues are over $133B and net income of about $10B (Today’s Lukoil). The two competitors are presented below as analyzed by Yahoo Finance.

Its performance is better than the two companies. Its EPS is lower than for Lukoil, and its P/E ratio is also lower. It means investors are willing to pay more for the other two companies’ shares than for Gazprom’s “OGZPY”. This analysis considers OGZPY because the real company stock, GAZP.ME, competitor analysis has not been presented.

Rosneft stock closed at RUB 272.62 on 24 Jan 2013 compared to Gazprom’s 146.40. Shares traded were 8.93m compared to GAZP.ME’s 22.4m. Its revenues grew by 41.1% compared to Gazprom’s 28.77%. Net income went up by 7.85% while Gazprom’s went up by 34.94% (NK Rosneft’ OAO ROSN: MCX “Financial Times”). This indicates that Gazprom’s fixed assets, such as pipelines, make it to reduce operating costs. Its net income percentages are higher than for Rosneft. Its operations must be more efficient than for Rosneft.

The 5-year dividend yield growth rate for Rosneft is 21.00% compared to Gazprom’s 28.70%. EPS grew by an average 5.97% over the last five years compared to Gazprom’s 16.23%. The book value of Gazprom shares (349.42) is higher than for Rosneft (239.58). However, with a current ratio of 2.01 and quick ratio of 1.70, Rosneft indicates a higher ability of repaying debts than Gazprom. Gazprom’s overall performance is better than for Rosneft.

Conclusion

Gazprom performance is outstanding compared to competitors in the industry. It continues to acquire more oil and gas reserves. Its expansion activities include acquisitions of other companies’ gas production sites. It may be considered to become a global monopoly in the gas industry. Its P/E ratio is the highest in the oil & gas industry. Other major gas companies consider consolidating their assets with Gazprom. Its expenditure on R & D indicates there is more to be expected on its operations worldwide. Its share values have appreciated to a value far much higher than the value they had at its foundation.

References

Book Value per Common Share. 2013. Investopedia. Web.

Brigham, E & Houston F. J. 2009. Fundamentals of Financial Management, South-Western Cengage Learning, Mason, USA.

Bose, C.D. 2006. Fundamentals of Financial Management, Prentice Hall, New Delhi, India.

Dividend Yield. 2013. Investopedia. Web.

Gazprom: Fields. 2013. Web.

GAZPROM: GAZP.ME – MCX 2013, Yahoo Finance. Web.

Gazprom: Marketing, 2013. Web.

Gazprom: Shares, 2013. Web.

Gazprom Today n.d. Web.

Gazprom OAO. 2013. Financial Times. Web.

Industry Center – Major Intergrated Oil & Gas 2013, Yahoo Finance. Web.

Market Watch, 2013. Annual Financials for Gazprom OAO ADS, Wall Street Journal. Web.

Market Watch, 2013. Gazprom OAO ADS, Wall Street Journal. Web.

Marson, J. 2013, Gazprom’s board approves 2013 investment reduction, Market Watch.

Marson, J. 2012, Gazprom says Nord Stream in pipeline build: report, Market Watch. Web.

Marson, J. 2013, TNK-BP to invest $7 Billion in Rospan gas project, Market Watch. Web.

Neely, J. 2013, Russian $7 bln gas bill dampens Ukraine’s glee at shale deal, Reuters. Web.

NK Rosneft’ OAO ROSN: MCX. 2013, Financial Times. Web.

Russian Natural Gas Monthly Price – Euro per Thousands of cubic meters. Index Mundi. n.d. Web.

Seyhun, N. H. 2000, Investment Intelligence from Insider Trading, MIT Press, Cambridge, USA.

Table 2: Discount Factors @1% to 10% Jan 2013, Department of Finance and Personnel. Web.

Today’s Lukoil n.d., Lukoil Oil Company. Web.

Appendices