Introduction

This paper examines the information system of McDonald’s to provide responses to issues related to information systems and the accounting information system. These issues are tackled in four cases all involving the McDonald’s. The paper includes points on the internal and external users of the system, information produced by the McDonald’s information system, decisions made as a result of the systems outputs, and the company’s strategy and strategic position. Further, the paper examines the transaction cycles in the company as well as notes the activities making up these cycles, the source documents involved, reports produced, and the company’s chart of accounts. The paper looks at the company’s business cycle to pinpoint people involved in data processing as well as information flowing in the organization, and documents and databases used in the system. The paper concludes with the examination of the company’s database management system and the DBMS logical data model as well as the advantages of the database system, problems of system implementation and the level of accountants’ involvement.

About McDonald’s

The McDonald’s Corporation, often referred to simply as McDonald’s, is the “world’s largest fast-food service chain” (Ferrante, 2008, p.143). It was founded in 1940 in the US, and has since spread into various parts of the world. The company is now present in the Middle East, where the company’s branch being investigated in this paper is located.

McDonald’s vision is “to be the world’s best quick service restaurant experience. Being the best means providing outstanding quality, service, cleanliness, and value, so that we make every customer in every restaurant smile” (Pradhan, 2006, p.326).

The information systems

McDonald’s information system is based on an Enterprise Resource Planning System. This system supports a number of subsystems: the “office and user productivity support system”, the “transaction processing system”, and the “decision making support system” (Morley & Parker, 2009, p.504). The office and user productivity support system is used to assist communication and productivity within the organization. The transaction processing system helps in recording and processing transactions. The decision making support system deliver information to people involved in decision making.

The subsystems within the office and user productivity support system include document processing system and communication system. The transaction processing subsystems include the order entry system, the accounting systems (including accounts receivable, accounts payable and general ledger, systems), and the payroll system (Morley & Parker, 2009, p.508). The decision making support system includes the management information system (MIS). The MIS is used to provide decision makers with information on time and on a regular basis.

External and internal information users

The main internal users of the of the company information include the departmental managers and the company’s top executives. The external users are mainly the company’s shareholders or investors, business partners, and financial institutions. Information produced for the external users includes financial information, sales and accounting information, and information on human resources and inventory. Information for external users is mainly financial information, especially the financial position of the company.

Outputs of the systems

The outputs for the company’s information system are useful in making decisions. For instance, sales forecast can be used in making decisions related to goods productions; that is, the amount of goods produced is dependent on the expected sales. Output related to human resources is useful in making decisions regarding staff recruitment, personnel training and development, payroll decisions, and provision of incentives. Financial information supports decision such as dividends awarding to shareholder, investments to make, and whether to seek credit (loans) and more inventors.

Data that would be useful in generating sales forecasts include daily sales figures. Human resource output is generated from data such as the number of people recruited in the company, number of employees on leave in each department, and number of employees who have left each department. Each data meant for the company’s information system is stored in centralized electronic databases. A computer system (software) is used to store data on the databases, as well as manipulate the database. Workstations are part of the company’s information system; they are linked to the central database such that input of data and output of information is done through these workstations.

The information provided by the McDonald’s information system is very useful to the company. It is timely (that is, it is available at the time it is needed), complete and sufficient, and highly accurate. Since it is accurate and verifiable, the information can be regarded as reliable. Moreover, the information is free from bias and most of it can be quantified. The information is also relevant and economical.

McDonald’s strategy and strategic position

The company is pursuing both “cost leadership” and “differentiation” to develop its competiveness (Porter, 2008). The company aims at reducing its operations costs to an appropriate minimum by utilizing various economies of scale, employing advanced technology, and standardization. The company also aims at differentiating its products from its competitors. Its strategy is to produce products of high quality.

McDonald’s aims at acquiring the largest market share for its products. Acquisition of a larger market share would require more efforts in research and development of products.

The Accounting Information System (AIS) helps McDonald’s to realize its strategy and strategic position in a number of ways. It provides relevant information that is useful in efficient allocation of resources, it eliminates some human process which would necessitate additional costs, and ensures that information is available on time. The AIS also enhances the efficiency of data collection and information reporting.

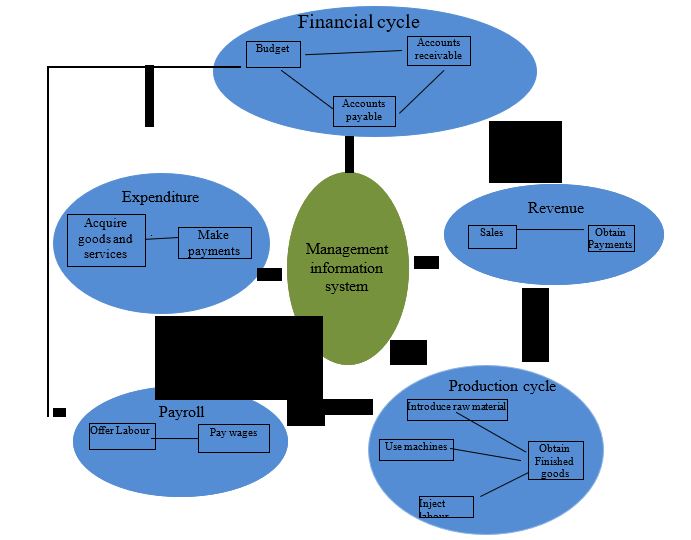

Transaction cycles in McDonald’s

McDonald’s has a number of transaction cycles. The transaction cycles include the financial cycle, the payroll cycle, the revenue cycle, the conversion/production cycle, the expenditure cycle, and the accounting cycle.

The financial cycle

The financial cycle represents the preliminary activities of the company business operations. It is concerned with the acquisition of resources for running the business, more so, during the start-up process. It involves raising capital necessary for supporting various business processes. Generating capital may involve acquiring loan from financial institutions, or as raising money through shareholders contributions.

The expenditure cycle

The expenditure cycle mainly involves utilizing resources based on the set budget to accomplish business tasks, and acquire other resources needed to run the business.

The revenue cycle

The revenue cycle is also important in transaction processing. It includes the dealings associated with sales of business products as well as the cost associated with the sales activities. The revenue cycle is preceded by the conversion cycle.

Production/conversion cycle

The production cycle involve transforming raw materials into finished products, which includes application of labour, and use of machines and equipments. It includes elements of both the payroll and expenditure processes.

The payroll cycle

The payroll cycle involves mainly staffing the company, or rather recruiting employees. Employees in the company have varying levels of authority which determine their salary and bonus scales. This variation in salary and bonus creates the need for accounting.

The accounting cycle

Each of the above mentioned transaction cycles contain an element of the accounting cycle. The accounting cycle involves activities such as checking payrolls and work tickets, invoicing, and placing purchase orders. The accounting cycle also involve transferring data from papers into the database, including verifying the data to ensure it is valid. The cycle also involves generating financial reports.

Transactions in the accounting and expenditure cycles

Both accounting and expenditure cycles are characterised by a set of activities (or transactions). The accounting cycle transaction involves identification of dealings and preparation of source document, analysis and categorization of transactions, enumeration of transactions into financial terms and ascertaining the accounts of concern. The cycle also involves recording transactions (creating journals) and creating T-accounts, or rather, the ledger accounts. Trial balances are also created in the accounting cycle. The cycle also involves rectifying differences and errors in the trial balances and adjusting journal entries. The cycle further involves production of financial statements, including balance sheets, income statements, and cash flow statements.

The transactions associated with the expenditure cycle include purchases, payment of goods and services (cash disbursement), and accounts payables transactions.

Source documents

McDonald’s uses a number of source documents to capture pertinent data for the accounting and expenditure transactions. The source documents include staff time cards, cash receipts, order forms, invoices, checks, credit memo, and credit card receipts (Morley & Parker, 2009, p.149).

Reports

A number of reports are generated in the accounting transaction cycles. These include mainly the financial statements, including income statements, cash flow statements, balance sheets, auditor reports, statements of shareholders’ equity, and statements of retained earnings (Brigham & Houston, 2009, p.62; Rich et al, 2009, p.23). These reports are used by investors to make investment decisions, by business owners and executives to make strategic management and investment decisions, for credit decisions by banks and suppliers, and taxation by the government. Employees also use these reports to seek employment in the company.

The reports generated in the expenditure transaction cycle include purchase reports, cash disbursement reports, accounts payable reports, and receiving reports (Delaney & Whittington, 2009, p.94). The purchase reports are used in making procurement decisions while receiving reports are used in payment authorization decisions. The accounts payable reports are useful in making decisions involving suppliers.

All these reports are adequate in terms of providing the relevant information to the company’s stakeholders, who are in need of making appropriate decisions.

Charts of accounts

The company’s chart of accounts is characterised by a listing of the company’s accounts. The chart of accounts’ structure is hierarchical with a tree-like view. This structure and tree-like view is useful because it allows decision makers to have an overall view of the accounts, it makes semantic search easier, it is more instinctive, and allows one to see and compute the accounts of concern (Cornyn & Mays, 1997, p.416). The hierarchical structure is so flexible that reorganizing the accounts is so easy. The flexibility of the structure also allows growth, or additional of accounts in the future according to needs.

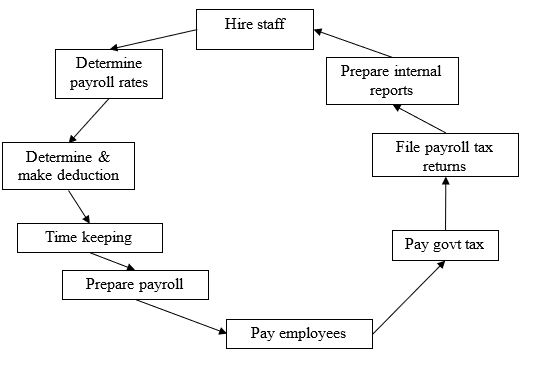

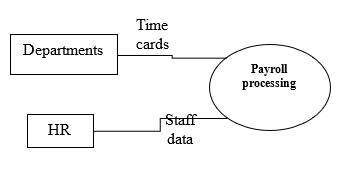

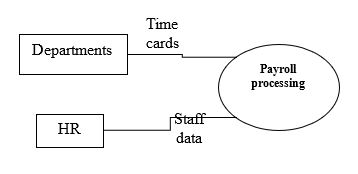

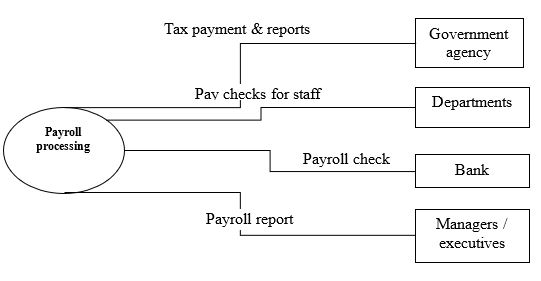

Examining one of McDonald’s business cycle: the payroll cycle

As highlighted earlier, the McDonald’s information system involves six business cycles: finance, revenue, payroll/personnel, expenditure, production/conversion, and accounting cycles. A deeper examination of the payroll/personnel cycle will help show information flow in the information system.

The payroll/personnel cycle is concerned with hiring and paying employees. The specific steps involved include hiring staff, approving payroll rates, making deductions, timekeeping, preparing payroll, paying staff, reimbursing payroll taxes, and filing tax returns associated with payroll.

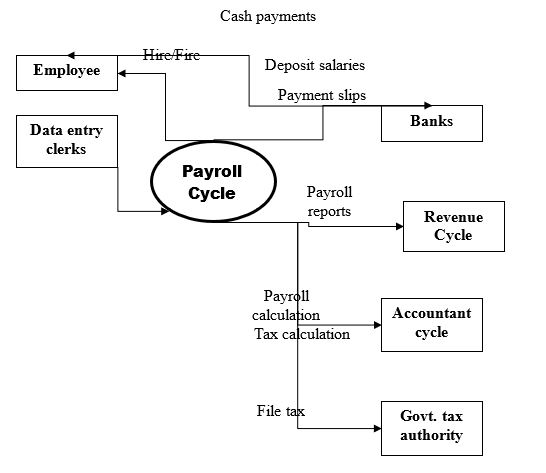

People involved in the processing data

There are a number of people and entities involved in the payroll/personnel cycle. These people and entities include HR staff and managers, accountants, data entry clerks, banks, and financial department’s staff, and government’s revenue authority.

Information flowing through the organization

The information flowing through the organization through the payroll cycle is broad. It includes the personnel rates, the number of employees, employees leaving the company in year, employees’ productivity, and so on.

A context diagram shows stakeholders outside the system (that is, the source and destination of (data) information, while a data flow diagram (DFD) shows more details of the data source and destinations flowing through various levels.

Data flow diagrams

Documents used in the system

There are a number of documents that are used in the company’s information system. These include the various source documents such as cash and credit card receipts, purchase orders, cancelled checks, staff time cards, invoices, and credit memo.

Other documents used in the company’s information system are the various reports. As mentioned above, the company’s reports include the financials statements such as the cash flow statements, balance sheets, income statements, statements of owners’ equity, and statements of retained earnings. Other reports include purchase order reports, cash disbursement reports, accounts payables reports, and receiving reports.

Files and databases

The company has three large databases for its information system, which consist of numerous tables and files. These databases include the customers and orders database, the asset management and inventory control database, and the human resource database. The customers and orders database contains information about the customers and purchase orders such as customers’ contacts, whether customers are corporate entities or individual, customers’ relationship with the company, customers’ purchase orders and purchases, customers’ geographical region and country, and other aspects relevant for marketing purposes. The asset management database includes data and information related to the company’s asset and equity. It includes information on the company’s innovations and products. Human resource database has information on the company’s staff, including information on the existing staff, retired employees, fired staff, and authority and responsibilities of each staff. The HR database includes also the salary scales of existing employees, their contacts and addresses, their academic qualifications and other professional information, and staffs’ personal information relevant for the company. The HR database also records the time card data, leave schedules and durations, and other data related to employees tasks. The human resource data in the database can be summarized as employee data, training data, job data, project data, and applicant data.

Other tools

The information system is also made of other tools such as the asset management tool, inventory control system, human resource management tool, and payroll software.

The database management system

McDonald’s uses an Oracle database management system (DBMS). This DBMS uses a relational logical data model and has a number of benefits that prompted the company management to use it for the company’s information system. The Oracle DBMS provides the benefits of a relational data model, which include easy linking of data in various records. In addition, the Oracle DBMS has a number of other attributes that make it suitable for supporting the information system. These attributes includes enhanced security (oracle supports secure connections between the client and the server), fast operating speed, and support for multiple platforms. Some Oracle functions such as flush back recovery and real cluster add value to this software. Atomicity, isolation, durability, and consistency are also some of the Oracle DBMS’ features that contributed to the software being selected to support the information system.

The database management system initially used by the company for its information system was also based on Oracle systems, but was inferior to the current system. Therefore, there were no major activities involving transfer of data to the upgraded database management system. Actually, the upgrade was more of updating the software to include more features such as improved security and enhanced support for the information system. However, with the growth of the company, there has been inclusion of more tables and records to the databases.

Advantages of the DBMS to the company

The advantages of the Oracle DBMS to McDonald’s have been enormous. The system has improved efficiency in storage and retrieval of data and information. It is easier and faster to search for records using this system than it would be with a manual system. It is also reliable in terms of security; the system provides secure connection between the client and the server. The Oracle database system of McDonald’s also includes myriads of features that support manipulation of the data contained in database.

Problems encountered in implementing the DBMS

The company faced a number of challenges in implementing the Oracle-based database management system. The immediate challenge was that the existing employees had no knowledge of the system. Therefore, it was necessary to conduct trainings as well as hire new employees. This process resulted in increased cost to the company. Actually, cost of implementation was an aspect of great concern to the company’s investors. Elsewhere, the implementation of the DBMS affected some operations of the organization during its implementation. The upgrade to the new version of the system also necessitated upgrading of the operating systems and some application software. Other majors problems encountered in the implementation were related to the hardware specifications. The existing systems did not meet the new software specifications and therefore upgrading of some computer hardware was necessary to meet the required specifications.

Accountants’ involvement in the database system

The company’s accountants have a high level of involvement in the database system. All the accounting data and information for the company is stored in the databases. Therefore, accountants must interact with the system in order to retrieve the data necessary for the tasks as well as store information that they generate. Some accountants interact with the system on a daily basis, while others use the system periodically. For instance, auditors interact with the system during auditing periods. However, as it is with the rest of the staffs, accountants are only allowed to access data that is relevant to the accounting activities.

Conclusion

This paper has examined the information system of McDonald’s and provided responses to concerns of the information systems. These responses are categorized under various cases. Internal and external users of the system have been identified as managers, top executives, staffs in various departments, as well as investors and financial institutions. Information and reports produced by the system, decisions supported by the systems outputs, the company’s strategy and strategic position, the transaction cycles, source documents, and the company’s chart of accounts have also been highlighted. This document has also pinpointed people involved in data processing, and information flowing in the organization as well as the database management system, its data model, its benefits to the company and challenges faced in implementing the database system.

Reference list

Brigham, E. F. & Houston, J.F. (2009). Fundamentals of financial management. Stamford, Connecticut: Cengage Learning.

Cornyn, A. G. & Mays, E. (1997). Interest rate risk models: theory and practice. Lessons Professional Publishing.

Delaney, P. R. & Whittington, O. R. (2009). Wiley CPA examination review, outlines and Study Guides. New York: John Wiley and Sons.

Ferrante, J. (2008). Sociology: a global perspective. Stamford, Connecticut: Cengage Learning.

Morley, D. & Parker, C. S. (2009). Understanding computers: today and tomorrow, comprehensive. Stamford, Connecticut: Cengage Learning.

Porter, M. E. (2008). On competition. Boston, Massachusetts: Harvard Business Press.

Pradhan, S. (2006). Retailing Management 2E. India: Tata McGraw-Hill.

Rich, J., Mowen, M., Hansen, D. & Jones, J. (2009). Cornerstones of financial accounting. Stamford, Connecticut: Cengage Learning.