Abstract

The accounting theory is going to be considered with the reference to the historical perspective of the issue development. Moreover, the structure of the accounting theory is going to be considered with the aim to understand the place of the accounting objectives in this structure, theoretical knowledge and practical assumptions in the discussed theme. Furthermore, nominative and positive accounting theories are going to be compared.

Introduction

Accounting is one of the main parts of business as all the incomes and costs are provided through the accountant. The existence of different theories in the accountancy allows different accountants work according to the theories they are more preferable to. Living in the world of information and innovative technologies, people still continue to work according to the accountant principles, which had been developed many years before, which is going to be considered in the history and development of accounting theory part of the essay, but with some innovations and the raised effectiveness strategies. The positive and nominative theories, which are going to be compared in the essay, are the different visions of one phenomenon and to consider this point is the main objective of the current paper.

The history and development of accounting theory

Analyzing the historical development of the accounting theories it should be mentioned that some scientists take up 1800s as the starting point for the accounting theories development. On the early stages of the accounting development, it was just used for the stewardship and external financial reporting, that was all. With the development of the accounting theory, the”Italian method” received a high widespread thought Europe in XVI and XVII century. The main idea of the method is used till now, that is the double-entry bookkeeping. The method of treating fixed assets was invented in XVIII century. During the XIX century the accounting continued its development as the economical science, and such methods as straight line, sinking fund and annuity method is evolved in the practice.

The cost accounting got wide spread in XIX century and it was the result of the industrial revolution. The accounting appeared to be more complicated and deeper science in the XX century, when the economical developments became to be the main consideration for all companies, and the relations between most corporations began to appear on the accounting bases, where the processes had to be followed attentively (Riahi-Belkaoui 6). The other significant moment in the history of the accounting development was provided in 1494, when Paciolo offered the usage of the journals, which contained the following items, “the date of the transaction, the name of the purchaser or the asset purchased, the name of the seller or the asset sold, the sum involved and a short narrative describing the transaction” (Glautier and Underdown 66). The mentioned innovations in the accounting system are not stopped for now as even in the modern world the accountants try to make the accounting system more effective.

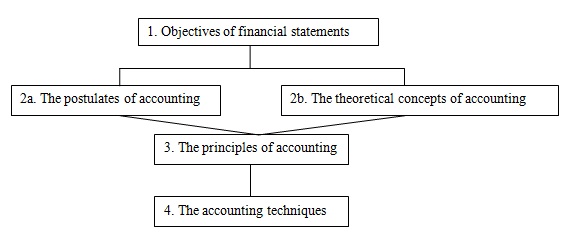

The structure of an accounting theory

The structure of the accounting system investigates the rules and techniques which are used there. To be more specific, the following scheme may be provided with the aim to introduce the accounting system better and with the higher level of detailing.

Describing the table, the postulates of accounting and the theoretical concepts come out of the objectives, which are the central points of the accounting, as they identify the main aim and direction of the accounting system in general. The postulates of the accounting and the theoretical framework of the accounting create the principles of the accounting, which, in its terms, provide the accounting techniques which are used on practice. In other words, the practical concepts of the accounting are impossible without the theoretical background. So, it may be concluded, looking on the table 1, that the objectives of the financial statement are crucial in the practical usage of the accounting theories and techniques, moreover, they direct the accounting systems, depending on the objectives.

Analyzing the notion of the accounting theory, the following information may be considered that accounting theory is “a coherent set of logical principles, which provides a better understanding of existing practices to users of accounting information, provides a conceptual framework for evaluating existing accounting practices and guides the development of new practices and procedures” (Porwal 22). Coming out of the definition of the accounting theories, the following classification may be offered, (1) inductive and deductive, (2) positive and normative and according to prediction level (Porwal 22). The comparison of normative and positive accounting theories is going to be provided further.

Positive accounting theory

Analyzing positive accounting theory it may be concluded that it explains and predicts the behavior in the accounting practice, coming out of what is now (Whittington 389). The main peculiarity of the positive accounting theory is that it is tied with the judgments and prescriptive implications, which in their turn may influence the choice of the hypothesis. The other core characteristic feature of the positive accounting theory is that it emphasizes “on predictions rather than on assumptions as a means of testing the validity of theories” (Whittington 392). Positive theory of accounting is resulted from the descriptive approach, when the accountants are aimed to predict their behavior in the relation to the treated problem. For example, cash, which is going to be entered in the debit side, may be predicted beforehand. Furthermore, Jack Rabin offers his own example of the positive accounting theory in action where it predicts the behavior of any firm in their attempt “to depict earnings as being lower than they are and will thus make accounting choices that decrease reported earnings to avert attention” (Rabin 17).

Normative accounting theory

The normative accounting theory identifies what is ought to be in the issue from the accounting perspective. The accounting practices, which ought to be adopted in the accounting issues, come from the normative theory. Accounting, as any other theory, has some standard situations, where this or that technique must be used. This is the main destination of the normative theory in accounting (Riahi-Belkaoui 109). Normative accounting theory also stresses on the methods according to which the decision is ought to be provided. The opinion is created that the normative accounting theory proponents attempt to make an accountant theory, according to which all decisions and the actions are going to be structured and predicted according to the scheme, which is going to be developed. In other words, in the case of the appearance of the difficulty, and relying on the normative theory, the accountants should act in the reference to the norms, which are developed and prescribed to the particular situation and no any further considerations should be provided in the case if it is not mentioned in the prescribed technique.

Differences between positive and normative to explanation phenomenon

Dealing with the positive and normative accounting theories it may be stated that these theories as if add to each other. The proponents of both normative and positive accounting theories criticize the opinion of each other, but in reality these two theories may never be considered absolutely separately. The positive accounting theory justifies what is, while the normative accounting theory tries to insure what ought to be used in the relation to this or that issue (Riahi-Belkaoui 109).

Stressing one more time on the differences of the positive and normative theories, positive theory is the theory which attempts to explain what is now, that is how the information is collected, while normative accounting theory explains what ought to be, that is how information is ought to be collected. Relating to the fact that the theories may never be separated, the argument should be provided that the normative theory (what ought to be) is usually cones from the positive theory (what is), and this interconnection may never be ruined (Porwal 10).

Conclusion

In sum, the historical development of the accounting was considered, the structure of the accounting theory was evaluated and the normative and positive theories were analyzed. The conclusion may be provided that positive and normative theories have different vision of the same phenomena, but at the same time they may never be separated absolutely, as normative theory comes out of the positive theory: normative theory explains how it ought to be done, coming out from the positive theory of what is now.

Works Cited

Glautier, M. W. E. and Brian Underdown. Accounting theory and practice. London: Pearson Education, 2001.

Porwal, L. S. Accounting Theory, 3E. New York: Tata McGraw-Hill, 2001.

Rabin, Jack. Encyclopedia of public administration and public policy. Newbury: Marcel Dekker, 2003.

Riahi-Belkaoui, Ahmed. Accounting theory. London: Cengage Learning EMEA, 2004.

Whittington, Geoffrey. Profitability, accounting theory and methodology: the selected essays of Geoffrey Whittington. London: Routledge, 2007.