Key aspects of Operations management

The Volvo Company has been a high quality car manufacturer for a long period. Their first car in 1927 did not perform well in the market however; the introduction of pv4 and ov4 models led the company to great heights. Since 1931 the company has consistently gained market as compared to other market players in the distribution of high quality motor vehicles. It impressed the rest of the world with its ability to improve the quality of their motor vehicles and they are able to gain high market share as well as increase the variety of vehicle models that they are selling (Mudie, P. & Pirrie, 2006).

The key areas in Volvo group that need operation management include management of quality, management of production, cost management social responsibility environment and logistics. In areas of quality, the company must ensure that the products produced and sold in the market have less defects and the supply must meet with the customers’ demands. This also involves mode of communication in the chain of supply used by the company in delivering the products in the market (Dixon, J.R., Nanni, A.J. & Vollmann, T.E., 1990).

In area of production and engineering, the company should ensure that the product produced using proper technology such as prototype in order to have the best output in the market. The vehicles produced should have spare parts as well as good features meeting the customer’s needs. Production should ensure that there is high quality with minimal cost of production and when delivered to market they are on time (Mascarenhas, O., Kesavan, R. & Bernacchi, M. 2006).

The company has ensured that the cost of production is maintained at an acceptable level as well as supplies of factors of production are paid on time in order to ensure there is a continuous supply. They have adopted open book approach in reporting the costs of production in the company to ensure accountability.

In terms of Social responsibility the company has ensured that all stakeholders of the company are taken care of in the activities. They have adapted ethical standards that ensure the environment is protected against emission from production plants of their motor vehicles. this is also facilitated with the use of green technology in production. The company has ensured that the human rights of employees are observed and they have put in place policies that govern the conduct of employees( Mudie, P. & Pirrie, A 2006).

Another key area of operation management is the logistics. They have ensured that dispatch is 100% fit for consumption and the delivery is on time. The delivery is also made in the right quantity and quality as well as fit for the purpose products. This has made Volvo group among the best producers in the Motor vehicle industry. The packaging of the products ensures that all products are serialized and a customer will only accept the product that has a serial number and sealed. All customers are advised to reject all product have their seal broken. There is also after sale services offered to customers which are another important area of management.

Technology and models of Production

The company has adopted various models of production but the best method that is used by the company in production is the green technology they have adopted as well as the broad type used (Mascarenhas, O., Kesavan, R. & Bernacchi, M. 2006).

Innovation: – Innovation is a process not just static. Man’s hunt for newer things and technology results in innovation and changes in life styles. As it is there in any case innovation also got two sides one for a good change and other for a bad out come. From the organization’s point of view innovation is very important. Many organizations now see innovation from a very important angle. A good leadership is mandatory to complement innovation. There will be people with creative ideas in any organization. But identifying and encouraging the talents is equally important. In some organization the management see innovative people as a threat to there own position and never take an extra step to appreciate or identify the efforts of these people. Even in some situations management discourage innovation due to the perceived threat to their position (Slack, N. Chambers, S. & Johnston, R. 2007)

The company has used various innovative ideas especially disruptive technology in the production of their motor vehicles. This has made them more profitable in the market. They are able to compete with other producers such as Toyota motor vehicles because of this technology. According to the companies website the company is a successful innovator (Dixon, J.R., Nanni, A.J. & Vollmann, T.E. 1990).

Disruptive innovation is the need of the hour. Most of the mangers are pressurized to make higher profits from the present technology. But it is very difficult in the present market. Technology is imitated very fast and become out dated very at the same speed. So it has become very difficult to move an inch with the existing products. So the key lies with the disruptive innovation. Managers have to make extra ordinary decision to compete in the present world. According to Clayton M. Christensen, Michael E. Raynor, and Scott D. Anthony Managers who wanted to perform should accept the need for disruptive innovation. “Managers today have a problem. They know their companies must grow. But growth is hard, especially given today’s economic environment where investment capital is difficult to come by and firms are reluctant to take risks. Managers know innovation is the ticket to successful growth. They also unveil the importance of disruptive innovation in industry and keys to achieve it. Disruptive innovation encourages growth. It can be utilized in many ways against competition. Either the firm can directly come in competition with existing firms by introducing new and cheaper product through disruptive innovation or the firm can reach newer market and newer consumers with products which are more acceptable and cheaper and also well fitting to the need of the customers. The mangers of industry should also know that the disruptive innovation targets newer market or lower end of the existing market. Disruptive innovation needs different planning than usual innovation. If it is planned as usual innovation the result may not be different than usual innovation. It requires special people and special planning (Mascarenhas, O., Kesavan, R. & Bernacchi, M. 2006).

Another problem lies wit the existing method, it is just segmenting the customers with the existing product and service features. The mangers have to live with the expectation of the customers and introduce newer products which would surpass the existing ones in respect of quality and price (Johnson, G. & Scholes, 2006).

Lean Production – JIT, Kaisen and continuous Improvement

Like most industry players the company has adopted just in time in stock control. In this method of stock control adapted by the company various issues are adapted. Product design and process design. Four elements of product design are important for JIT: standard parts, modular design and highly capable productions systems with quality built in and concurrent engineering. The use of standard parts means that workers have fewer parts to deal with, and training times and costs are reduced. Purchasing, handling and checking quality are routine and lend themselves to continual improvement. Another important benefit is the ability to use standard processing (Slack, Chambers & Johnston, 2007).

Modular design is an extension of standard parts. Modules are clusters of parts treated as a single unit. This greatly reduces the number of parts to deal with, simplifying assembly, purchasing, handling, training and so on. Standardization has the added benefit for reducing the number of different parts contained in the bill of materials for various products, thereby simplifying the bill of materials (Dixon, J.R., Nanni, A.J. & Vollmann, T.E. 1990).

JIT requires highly production systems. Quality is the sine qua non of JIT systems because poor quality can create major disruptions. Quality must be embedded in goods and processes. The systems are geared to a smooth flow of work; the occurrence of problems due to poor quality creates disruption in this flow(Johnson, G. & Scholes, 2006).

Because of small lot sizes and the absence of buffer stock, production must cease when problems occur and it cannot resume until the problems have been resolved. Obviously shutting down an entire process is costly and cuts into planned output levels so it becomes imperative to try t avoid shutdowns and to quickly resolve problems when they do appear(Johnson, G. & Scholes, 2006).

JIT systems use a comprehensive approach to quality. Quality is designed into the product and the production process. High quality levels can occur because JIT systems produce standardized products that lead to standardized job methods, employee workers who are very familiar with their jobs and use standardized equipment. Moreover the cost of product design low cost per unit. It is also important to choose appropriate quality levels in terms of the final customer and of manufacturing capability. Thus product design and process design must go hand in hand (Mascarenhas, O., Kesavan, R. & Bernacchi, M. 2006).

Process design:-Seven aspects of process designs are particularly important for JIT systems: small lot sizes, set time reduction, manufacturing cells, limited work in process, quality improvement, production flexibility and little inventory storage.

Small lot sizes – in the JIT philosophy the ideal lot size is one unit a quantity that may not always be realistic owing to practical considerations requiring minimum lot sizes. Nevertheless the goal is still to reduce the lot size as much as possible. Small lot sizes in both the production process and deliveries from suppliers yield a number of benefits that enable JIT systems to operate effectively. First with small lots moving through the system, in-process inventory is considerably less than it is with large lots. This reduces carrying costs, space requirements and clutter in work place. Second inspection and rework costs are less when problems with quantity occur, because there are fewer items in a lot to inspect and rework(Johnson, G. & Scholes, 2006).

Supply Chain Management

Supply managers are people at various levels of the organization who are responsible for managing supply and demand both within and across business organizations. They are involved with planning and coordinating activities that include sourcing and procurement of materials and services, transformation activities, and maintaining quality of products services.

Quality refers to the ability of a product or services to consistently meet or exceed customer requirements or expectations. Different customers will have different requirements, so a working definition of quality is customer- dependent. One way to think about quality is the degrees to which performance of a product or service meets or exceeds customer expectations. The difference between these two, that is performance–Expectations, is of great interest have been met. If these two measures are equal, the difference is zero and the expectations have been met. If the difference is negative, expectations have not been met., whereas if the difference is positive, performance has exceeded customer expectations(Slack, Chambers & Johnston, 2007).

Customers expectations can been broken down into a number of categories, or dimensions, the customers use to judge the quality of a product or service. Understanding this helps the organizations in their efforts to meet or exceed customer expectations. The dimension used for goods are somewhat different form those used for services.

The Role of HRM and People Management

More than ever, the human resource strategies, objective, systems and processes of the organization must be integrated and synchronized with the overall Volvo’s strategies, objective, systems and processes and the rest of the organization. Human resource as one of the key success factors in implementing the operations strategy must be able to support and not detract the company from it. Hence, the personnel selection, training and development, and performance appraisal processes should be seamlessly integrated into the whole organizational structure ad systems to ensure that all these systems are working towards the same goal: creating uncontested market space and making the competition irrelevant (Mascarenhas, O., Kesavan, R. & Bernacchi, M. 2006).

Mondy & Noe defined recruitment as the “process of attracting individuals on a timely basis, in sufficient numbers, and with appropriate qualifications, and encouraging them to apply for jobs with an [organization]” (2005, p. 199). The objective of the selection process for any type of [organization] is selecting the best “individual suited for a particular position and the organization” (Mondy & Noe, 2005, p. 162). Hence, for Volvo the goal of the organization’s selection process should be selecting the best individual suited for the vacant position and have the necessary capability to help the company in its quest in making the competition irrelevant.

On the other hand, the performance appraisal system is a “formal system of review and evaluation of individual or team task performance” (Mondy & Noe, 2005, p. 252) “to determine who should be promoted, demoted, transferred, or terminated (Anthony, Kacmar & Perrewe, 2002, p. 354). Several of the factors that affect the effectiveness of an appraisal system are job-related criteria, performance expectations, standardization, trained appraisers, continuous open communication, performance reviews, and due process (Mondy & Noe, 2005, pp. 270-272). Managing employee performance is one of the more difficult and complex activities within an organization. Unlike the other resources of a business, the human resource is not very easy to control: people think and act accordingly.

Anthony, Kacmar & Perrewe wrote that an effective performance appraisal system are “not only tools for evaluating the work of employees but also for developing and motivating employees” (2002, p. 351). These benefits are central to why the performance appraisal system was developed in organizations: employees need to be motivated and developed in order to perform their jobs effectively and efficiently. Furthermore, the appraisal system of a company can also be used to “determine who needs formal training and development opportunities” (Anthony, Kacmar & Perrewe, 2002, p. 354). In the end, all of these will result to a better equipped human resource. Hence, for Volvo Motors Corporation its performance appraisal system must be redesigned to fit the operation strategy of the company. As a vital component in motivating its employees, the human resource performance appraisal system of Volvo should not operate in a vacuum, rather it must support the goal of developing organizational competencies to make the competition irrelevant (Mascarenhas, O., Kesavan, R. & Bernacchi, M. 2006).

What had Volvo Corporation done for its worldwide human resource management is admirable – it developed HRM practices to sustain the Volvo Production System (Winfield 1994, p. 41). However, today it is no longer enough. It is time that Volvo models its human resource management practices to sustain the operation strategy. The four goals as promoted by the company’s existing human resource management practices are “employee commitment, workforce flexibility and adaptability, quality” (Winfield 1994, p. 50) in the operation strategy perspective are only several of the factors needed in creating an uncontestable market as opposed to the current practice.

Volvo has empowerment their employees and empowering is the process of giving employees an opportunity to exercise authority and responsibility regarding decision making in the organization and in their departments for improvement of customer satisfaction and product differentiation. The conditions relating to decision making are removed and employees are left to make decisions and make them powerful. Before employee empowerment is implemented in an organization, employees are powerless in bringing desired organizational changes which increase the profitability of an organization. It is the current idea relating to employee motivation and has had great influence in an organizational change in the recent past(Slack, Chambers & Johnston, 2007).

Some of the advantages of employee empowerment include increased participation if production process by employees who leads to great innovation and product differentiation. At the same time, it enhances training and development of employees relating to the specialty of their profession and job. Employee empowerment has reduced conflicts among employees and with the management and administration. Job satisfaction has also increased or changed and currently where employee empowerment has been implemented, job turn over has reduced drastically. This job satisfaction has led to reduced absenteeism from places of work since members will wish to continue under the same conditions. Through the following Volvo has kept high morale in their employees and empowerment possible(Slack, Chambers & Johnston, 2007).

The leadership adopted by the organization can be a source of employee empowerment and they have ensured that employees of the organization were given free hand to make decisions and ensure that the company’s’ products were improved. He encouraged teamwork where employees worked as teams and each team had a goal to accomplish. The goal was to be accomplished without employees being given conditions on how to make decisions relating to the products of the company. This led to aggressiveness and stability in the company (Robinson S. 2005).

Organization’s objectives are set in a manner that they allow employee empowerment. When the organization is setting performance objectives they should be challenging and influential to the employees. Performance objectives have many purposes that benefit both the organization and the employees. These objectives help to determine employee’s strengths and weakness. Also they can provide an opportunity for the employees to discuss performance and performance standards often with their supervisor, Further they can be used to recommend salaries to employee therefore this show that they are important hence they should be influenced and challenging such that they can be used probably to achieve the organization goals and further it will bring that satisfaction to the employee that they are incorporated in setting them(Johnson, G. & Scholes, 2006).

Integrating Operations Management

In most organizations, change is inevitable if profitability is going to be maintained and winning the trust from the bank. Change is not only in the people’s lives but also in our organizations. In your organizations a lot needs to be changed to avoid the problems that are being experienced currently. The change that should be implemented will take many dimensions in the short run and long run. Tough measures need to be taken to make the company afloat. Your company throughout has been successive but in recent times they have experienced a decline in market share for your brands. Unfortunately these changes are due to cutthroat competition in the industry of your operations. In business, gentlemen you have to know that in order to sustain the status quo or survive in this highly competitive environment it is not cheap but very expensive. To maintain this standing in the market, you have to spend more money in various activities such as advertising, inventory management, and improvement of quality, re-branding, brand extension, differentiation, and vertical integration with suppliers, expansion and going international. This will enable you maintain and sustain the market interest in your products and services, although this is vital in the long run, if spending is not checked therefore you should strive as much as possible to maintain the existing customers and continue making new ones too(Slack, Chambers & Johnston, 2007).

Quality Management and Quality Strategy

Successful management of quality requires that managers have insights on various aspects of quality. These include defining quality in operational terms, understanding the costs and benefits of quality, recognizing the consequences of poor quality, and recognizing the need for ethical behavior. It is true that all members of an organization have some responsibility for quality, but certain parts of the organization are key areas of responsibility(Johnson, G. & Scholes, 2006):

Top management has the ultimate responsibility for quality. While establishing strategies, for quality, top management must institute programs to improve quality; guide, direct, and motivate managers and workers; and set an example by being involved in quality initiatives. Examples include taking training in quality, issuing periodic reports on quality, and attending meetings on quality.

Design: quality products and services begin with design. This includes not only features of the product or services; it also includes attention to the processes that will be required to produce the products and/or the services that will be required to deliver the service to customers.

Production /operation – Production /operation have responsibility to ensure that processes yield products and services that conform to design specifications. Monitoring processes and finding and correcting root causes of problems are important aspects of this responsibility.

Quality assurance – Quality assurance is responsible for gathering and analyzing data on problems and working with operations to solve problems.

Packaging and shipping: this department must ensure that goods are not damaged in transit, which packages are clearly labeled, and that instructions are included, that all parts are included, and shipping occurs in a timely manner.

Marketing and sales: this department has the responsibility to determine customers needs and to communicate to the appropriate area of the organization. In addition, it has the responsibility to report any problem to the product or services.

Customer service: customer services are often the first department to learn of problems. It has the responsibility to communicate that information to the appropriate department, deals I reasonable manner with customers, work to resolve problems, and follow us to confirm that the situation has been effectively remedied.

Total Quality Management: – (TQM)-The term Total Quality Management (TQM) refers to a quest for quality in an organization. There are three key philosophies in this approach. One is a never- ending.

Push to improve, which is referred to as continuous improvement; the second is the involvement of everyone in the organization; and the third is a goal of customer satisfaction, which means looking only at the quality of final product services – to looking at the quality of every aspect of the process that produces the product or services. TQM systems are intended to prevent poor quality from occurring.

We can describe TQM qualities as follows:

- Find out what customers want. This might involve the use of surveys, focus groups, interviews, or some other techniques that integrates the customer’s voice in the decision- making process. Be sure to include the internal customer (the next person in the process) as well as the external customer (the final customer).

- Design a product or service that will meet (or exceed) what customers want. Make it easy to use and easy to produce.

- Design processes that facilitate doing the job right the first time. Determine where mistakes are likely to occur and trey to prevent them. When mistakes do occur, find out why so that they are less likely to occur again. Strive to make the process “mistake proof”.

- Keep track of results, and use them to guide improvement in the system. Never stop trying to improve.

Many companies have successfully implemented TQM programs. Successful TQM programs are built through the dedication and combined efforts of everyone in the organization. Top management must be committed and involved (Wooldridge, A. 2007).

Sigma

Prior to the Six Sigma, Volvo was using conventional approach. But customer dissatisfaction only intensified. Complaints came buzzing in primarily due to products failure. Apparently, they lost customers as well as profits. The huge cost of production and operation pressed down the company which was at the losing end. What made it worse was that the Japanese competitors were able to take their market share. This gave the company a wakeup call (Larson, 2003). From their Japanese competitors, Volvo realized that a huge change was necessary; change that would encompass all operation systems including manufacturing, service, administration and sales. A paradigm shift towards full customer satisfaction was worked out. The mathematics of the Six Sigma was formulated by Bill Smith (Larson, 2003). Since its launch in 1927, Volvo has developed its strategies using Six Sigma.

Six Sigma strategies have a history of high-volume manufacturing of near-perfect products. Aside from manufacturing however, Six Sigma can be applied in every industry and in every process. Only that it has to be adjusted or tailor-made for a particular industry for perfect alignment. It can improve various areas in an industry including manufacturing, services, engineering, sales and marketing, healthcare, government and corporate functions. Volvo which developed the Six Sigma is a manufacturer of semiconductors. In every manufacturing industry, it is very important that wastes must be reduced to the lowest level to ensure profit. Since Six Sigma implied goals of near perfect products, then it perfectly fits in the industry. In the area of services, it is effectively used in large companies such as GE which ventures into different businesses. GE applied Six Sigma in its financial services. In engineering, they are involved in creating new and exciting products and services. Hence the Six Sigma tool kit is useful in engineering. Designs and decisions in engineering can be further improved by the Six Sigma. Six Sigma strategies can help in improving health care delivery system. Since healthcare has to deliver services to everyone, there must be a way to counter the shortages. In the government institutions can improve efficiency and effectiveness by using the Six Sigma. Although unlike the private sector which constantly innovates, the public sector seems to lag in innovation thus this would be targeted if Six Sigma was applied in the government institutions. Lastly, in corporate functions, it is easier to fit the Six Sigma with their goals. Six Sigma strategies can easily work within all areas in the corporate world (Bertels, 2003).

One of the early adopters of the Six Sigma, General Electric (GE), stated that Six Sigma is a “disciplined methodology of defining, measuring, analyzing, improving and controlling the quality in every one of the company’s products, processes and transactions with the ultimate goal of virtually eliminating all defects” (Ramberg, 2000). The way to the minimal defects goals is through the five steps:

- define the process that needs improvement or control,

- measure the performance of the process,

- analyze the collected data,

- improve the process based on the result of the analysis

- control the process so that following improvement, near-zero rates will be achieved (Grant, 2006).

Three main areas of operation are basically targeted by Six Sigma wherein dramatic cost savings will be attained by company. Aside from that, it will help companies retain their customers, capture new markets and most importantly to build a reputation of being a company with top-performing products and services. Six Sigma strategies therefore is a business initiative. When a company was said to achieve the Six Sigma, its products and services are virtually of no defects. Nonetheless, in order to achieve the Six Sigma, total management commitment has to be present (Pande et al., 2001).

In implementing Six Sigma process, there are major elements to be considered. Basically, it needs strong leadership especially that those leaders are looked up to and have the ability to permeate all areas of management and operations. Tangible business results will be at hand if the senior leaders of the company will aggressively deploy to all employees including the lowest level the sense of urgency to achieve these aimed results. It is necessary then that CEOs should be strong leaders. Aside from that, it needs initial focus on operations, clear performance metrics, aggressive project selection, and selecting and training the right people. Together these elements will help facilitate the Six Sigma within the company (Hahn et al., 1999).

The combination of the right projects, right people and the right tools is essential for Six Sigma to completely work. For example, statistical tools are powerful but only when used by the right people on the right projects and in the right manner. Hence, it is necessary to carefully choose the most talented people for a given project and allow them to use the appropriate tools. The black Belts and the Master Black Belts are some of the most highly regarded people in a business thus they are significant candidate to take the roles. Carefully choosing the people to work in a particular project is a must because results are highly dependent on them (Hahn et al., 1999).

Six Sigma is not only about fostering quality program, it also changes culture within an organization. Culture change within a company requires strong leadership and focus on project implementation. The company’s top leaders should agree to drive deployment of Six Sigma approaches at all levels. They should also integrate Six Sigma approaches in business planning and deployment process within the organization. Competencies in statistical data analysis should be developed by individual leaders. They must also be able to cascade their competencies to other leaders. For the company’s top leaders to be successful in implementing Six Sigma in all levels in the organization, they must understand seven steps of deploying Six Sigma. (1) For Six Sigma initiatives to spread there should be support from committed team leaders. (2) Strategy planning and deployment must be integrated with strategic Six Sigma thinking and best practices. (3) Wherever the company operates, it needs to establish a close connection with the customers and the whole marketplace. (4) It must ensured that leaders do not view the company as mere isolated functions rather a family of closely related business processes which is supporting the business’ value. (5) Quantifiable measures must be developed. Other than that, leaders must demand from their employees their expectations and the aspired tangible results. (6) To compliment the employees’ performance, incentive and rewards system must be developed by the company. This would also entice the employees to perform better. (7) Lastly, top leaders must commit to all of the six strategies (Smith et al., 2002).

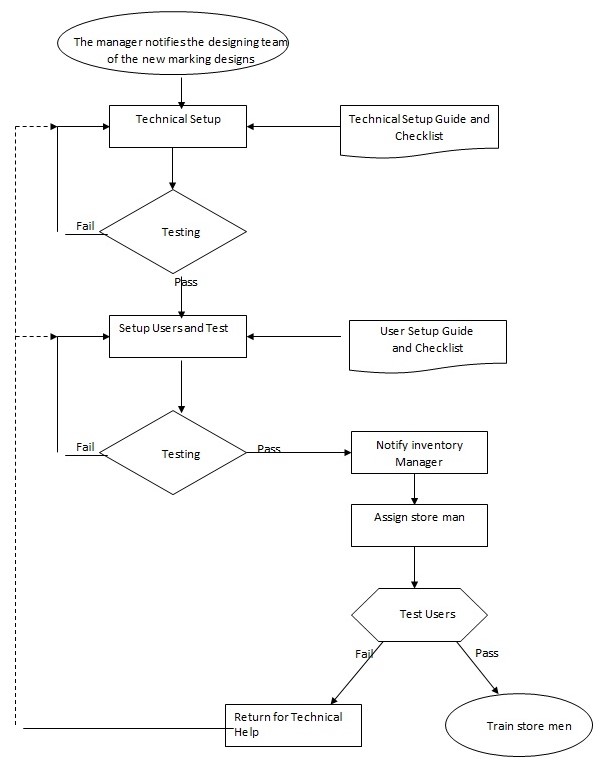

Operations Management and IS

Our internal process for setting up a new customer in our Internet software is complex, requiring over various steps for a typical customer set-up. The following “As Is” flow chart depicts the customer set-up process. A product lines such a luxury car, can be disaggregated into lot numbers that designates the style, and color. The sales forecasting model produces a cumulative estimate of what wranglers own customers will want. Sales volume is not uniform throughout the year. Given managements policy of providing a high level of customer service, a safety stock must be added to the forecast to hedge against demand forecast uncertainty. The safety actual demands stock model is based on statistical fit of month’s forecasts. The product line planning model indicates the cumulative production needed at each of the next 12 months. It reflects Volvo policy of keeping the workforce level throughout the year. Given the planned line level the fourth and build up inventory at the product line level, the fourth model disaggregates this inventory down to lot numbers. The fifth model takes the planned inventory of a lot at a specific week and apportions the stock to sizes. The sixth model calculates that net requirements from the preceding gross requirements for each customer (Wooldridge, A. 2007).

Conclusion and recommendation

The major factor that influences the continuous success of Volvo Company is the demand for vehicles that run on alternative energy aside for oil they have already responded well to this by adapting green technology and ensuring the management decisions are made in satisfaction of customers needs. They have maintained high quality levels of products. The few models made by the company have gained popularity as well as dominance on the market. This is due to great research and development adapted by the company. The abrupt change in demanded due to economic crisis caught the company in crisis but in many areas were caught because of technology adapted but ensured quality of the products they produced (Wooldridge, A. 2007).

The rest of the factors that can have a significant impact on the performance of Volvo are only the ones that new upstarts in other countries will create. Technology for fuel type to be used on engines is one major factor, aesthetics as well as pricing is going to be another major factor. The race for integration and constant improvement will always play a decisive role in the years to come. The kind of shift in consumer purchasing power for the middle class of both China and India will also mean a considerable change in the strategy and types of vehicles that Volvo might produce. The customers are all very inconvenient in terms of the rising gas prices as well as the fact that they are not helping the environment at all. The one that can best understand the needs of the consumers will win the biggest market share in the end. This single quality of Volvo of being responsive to the trends and demands of the consumer will mean that they will always remain a formidable competitor if ever they are dislodged from their current position of being the number one car maker in the world. In the end, it is the management that will determine whether or not they are providing the needs of the consumer. The technology may change and the various business factors may change but it is the ability of the management to adopt to changes that is the most important(Slack, Chambers & Johnston, 2007).

References

Anthony, W., Kacmar, K., & Perrewe, P. 2002, Human Resource Management: A Strategic Approach, 4th edn, South-Western, Ohio.

Atkinson, A.A., Waterhouse, J.H & Wells, R.B. (1997) stakeholders approach to strategic performance measurement. Sloan Management Review. 38(3), 25-37.

Balanced scorecard Strategy 2008, ‘The Strategy Canvas’, www.blueoceanstrategy.com, Web.

Dixon, J.R., Nanni, A.J. & Vollmann, T.E. (1990) The New Performance Challenge – Measuring Operations for World-class Competition. Homewood, IL: Dow-Jones Irwin.

Drucker, P. F. 2002, ‘The Discipline of Innovation’, Harvard Business Review, August, pp. 95-102.

Johnson, G. & Scholes, K. (2006) Exploring Corporate Strategy: Text and cases (6th ed.). Harlow: Pearson Education Limited.

Johnson, H.T. and Kaplan, R.S. (1987) Relevance Lost: The Rise and Fall of Management Accounting. Boston, MA: Harvard Business School Press

Kaplan, R.S. and Norton, D.P. (1992) The Balanced Scorecard – measures that drive performance. Harvard Business review. 70(1), 71-79.

Kaplan, R.S. and Norton, D.P. (2000) Having trouble with your strategy? Then Map it. Harvard Business Review. 78(5), 167-176.

Kaplan, R.S. and Norton, D.P. (2000) The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment. Boston, MA: Harvard Business School Press.

Lynch, R.L. & Cross, K.F. (1991) Measure Up – The Essential Guide to Measuring Business Performance. London: Mandarin.

Mascarenhas, O., Kesavan, R. & Bernacchi, M. 2006, ‘Lasting customer loyalty: a total customer’, vol. 23, no. 7, pp. 397-430.

Mondy, R. W., & Noe, R. M. 2005, Human Resource Management, 9th edn, Pearson Education, New Jersey.

Mudie, P. & Pirrie, A (2006) Services Marketing Management ( 3rd ed.). Oxford: Butterworth-Heinemann.

Neely, A. (1998) Measuring Business Performance. London: Economist Books.

Ng, P. T. 2004, ‘The learning organization and the innovative organization’, Human Systems Management, pp. 93-100.

Shenhar, A.J. & Dvir, D. (1996) Long term success dimensions in technology-based organizations. New York: McGraw Hill.

Slack, N. Chambers, S. & Johnston, R. (2007) Operations Management (5th ed.). London: Prentice Hall.

Winfield, I. 1994, ‘Toyota UK Ltd: Model HRM practices?’, Employee Relations, vol. 16, no. 1, pp. 41-53.

Wooldridge, A. 2007, ‘The Final Thoughts of Management’s Big Thinker’, The Wall Street Journal, vol. 31, no. 125, p. 12.